What do we mean by debasement?

At Thematic Markets I’m in the middle of a three-part series on “debasement,” the first one on gold with pieces to follow on the dollar and Bitcoin. In thinking through the outlook for these three fundamental market prices, it struck me that there is a lot of misunderstanding about what constitutes fiat currency debasement and how to protect yourself against it. Let’s start by digging into what exactly debasement means.

A compelling but misleading chart

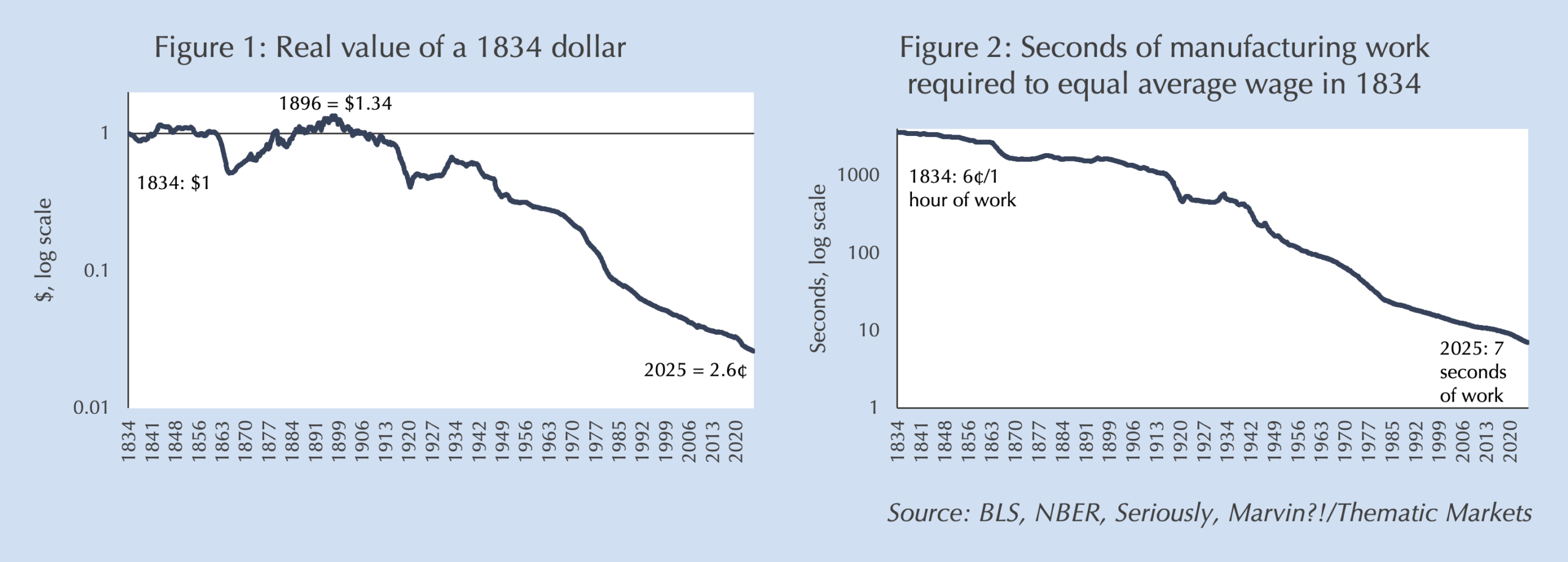

A common definition of fiat currency debasement is the loss of its purchasing power. That’s a reasonable definition, except it leaves out a critical element: time. If a dollar loses 10% of its value in a month – hyperinflation – it not only is unattractive to hold but even ceases to be an effective medium of exchange. If it loses 10% over a century, would anyone notice? If you’ve spent any time on social media, you will surely have seen a chart similar to Figure 1. On its face, the chart is quite damning: a dollar today buys 2.6¢ of what an 1834 dollar could buy. But that “debasement” took six to seven generations. Careful observers will note that the dollar’s purchasing power didn’t firmly fall below its 1834 value until 1906, but again, that’s at least four generations ago. Does that really count as debasement to anyone who doesn’t keep their life savings in cash under their matress?

But what happened to wages?

The answer to that question lies in part in what happened to wages over those many generations of falling purchasing power. Figure 2 shows how long a manufacturing worker has to work today to earn as much as his great-great-great-great grandfather did in an hour in 1834 (6¢): 7 seconds. Put another way, despite the 97.4% fall in the dollar’s purchasing power over the last two centuries, wages have risen more than 513 times, so that an hour of labor today buys 13.4 times as much as it did in 1834. This reflects two phenomena operating in different directions: (1) that productivity gains are ultimately reflected in real (inflation-adjusted) wages; and (2) that price inflation translates to wages, too.

Standard of living

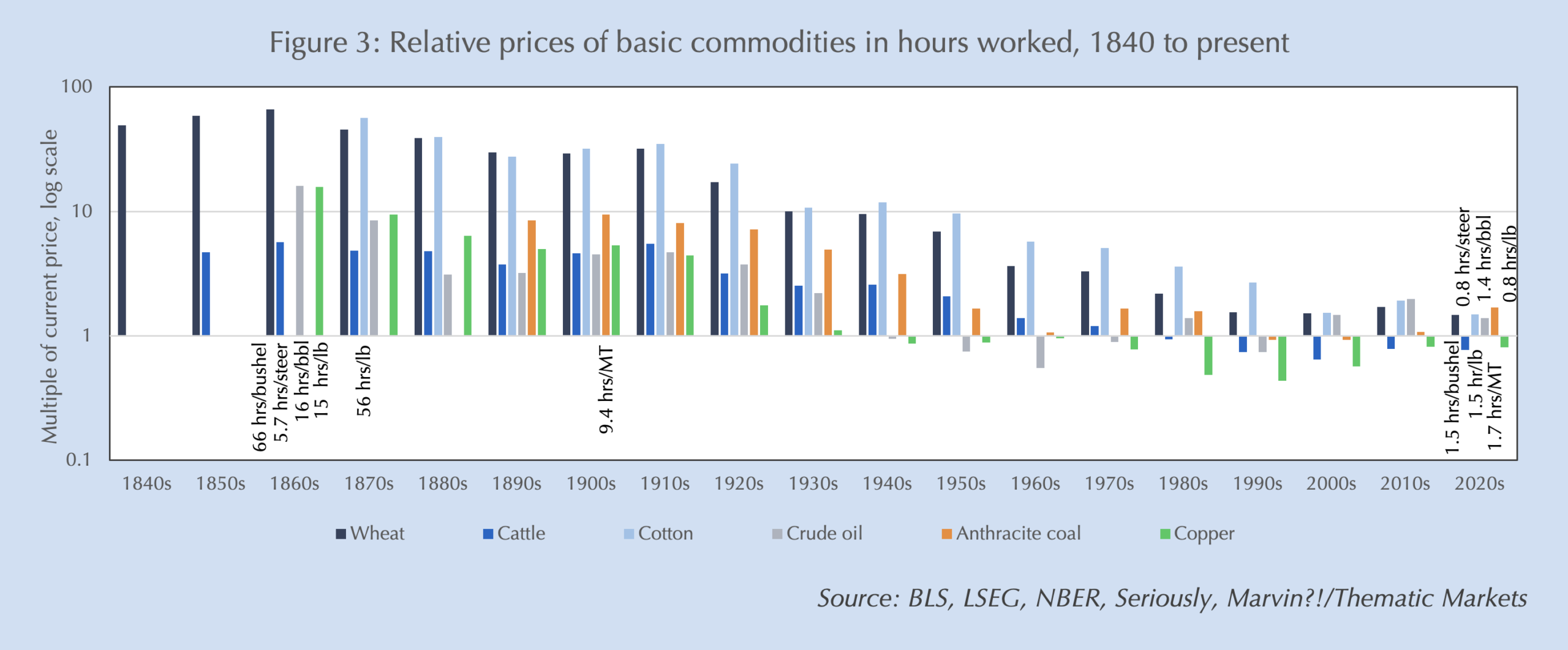

The first effect is the main driver of our standard of living. As technological progress and “learning by doing” raise productivity, we produce more output with less input and that ultimately is reflected in our wages and purchasing power. Figure 3 displays the prices of six basic commodities representing food, clothing, energy, and metals in hours of labor required to purchase fixed measurements from the 1840s to the present. For all those who worry about mismeasuring consumer price inflation, there’s none of that here: these are traded commodity prices divided by prevailing hourly manufacturing wages; no hedonic adjustment or any other gimmicks. Noting the log scale on the vertical axis, the fall in real prices – increases in our real standard of living – has been spectacular. In the 1860s a typical worker would need to work 66 hours for a bushel of wheat and 16 hours for a barrel of oil; today’s workers would need just 1.5 and 1.4 hours, respectively.

Then why do people hate inflation?

If our standard of living is determined by productivity, why then does it matter what our wages are denominated in? Or, why do people care about inflation? The reason is that our wage, business and other contracts are denominated in nominal currency values and generally are not indexed to inflation. As a result, wages can fall behind the prices of goods leading to a temporary erosion of our standard of living. If the rate of inflation is small, most people don’t notice it before their wages reset, but if the rate of inflation is high, it becomes far more noticeable. That explains why fewer than 10% of Americans considered inflation a problem before Covid but more than a third did after the Fed allowed it to skyrocket in its aftermath.11 This is why time matters: if “debasement” takes place over decades, wages have time to catch up before inflation materially impairs our standard of living, whereas rapid inflation erodes real wages.

The golden olden days…

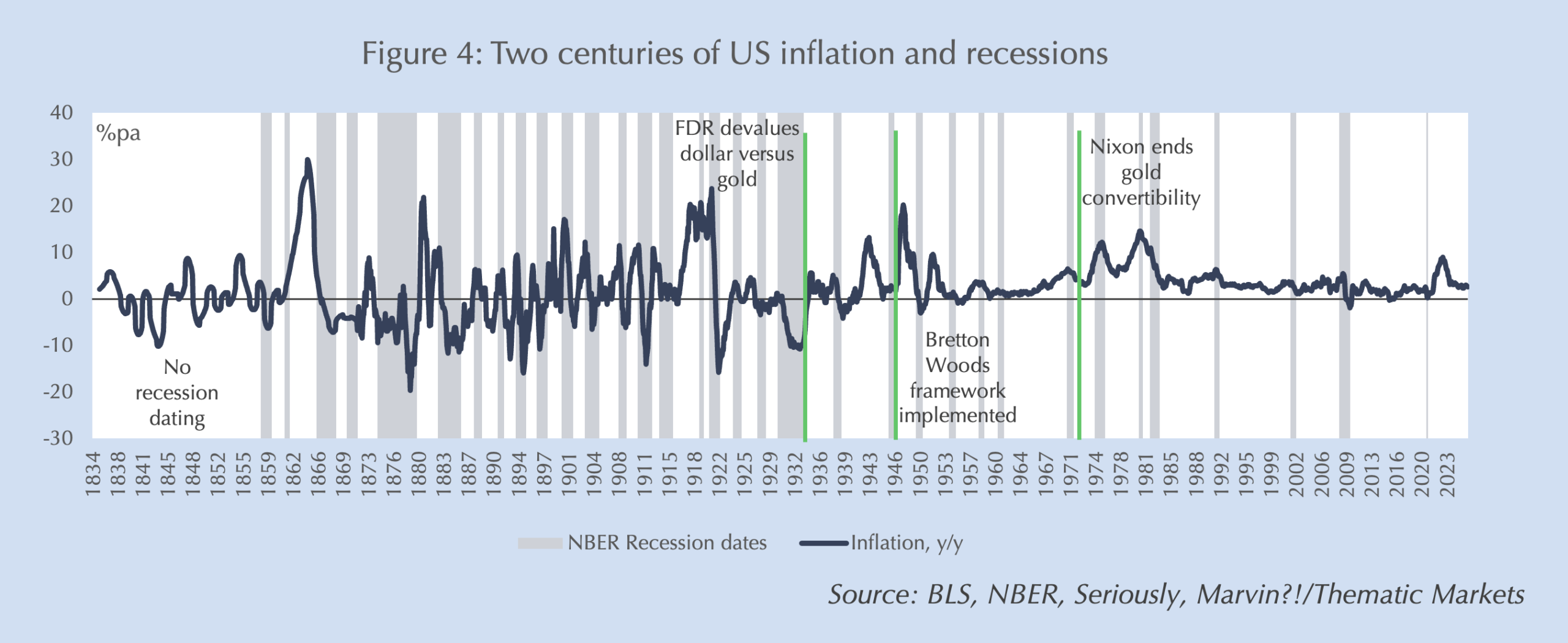

That observation has led many to pine either for the golden days of yore under the gold standard, or for “decentralized” money with a fixed supply, like Bitcoin. Yet, despite claims to the contrary, history shows that was worse, not better. Figure 4 displays US inflation rates over the last two centuries with economic recessions shaded with vertical stripes (since 1857 when the National Bureau of Economic Research’s official recession record starts). President Franklin Delano Roosevelt’s 50% devaluation of the dollar versus gold in 1933 roughly divides the chart in half between the Classical Gold Standard before and the Bretton Woods and floating exchange rate periods that came after. The difference is stark: under the gold standard, inflation was far more volatile and recessions were more numerous, longer and often much more severe.

Something’s gotta give

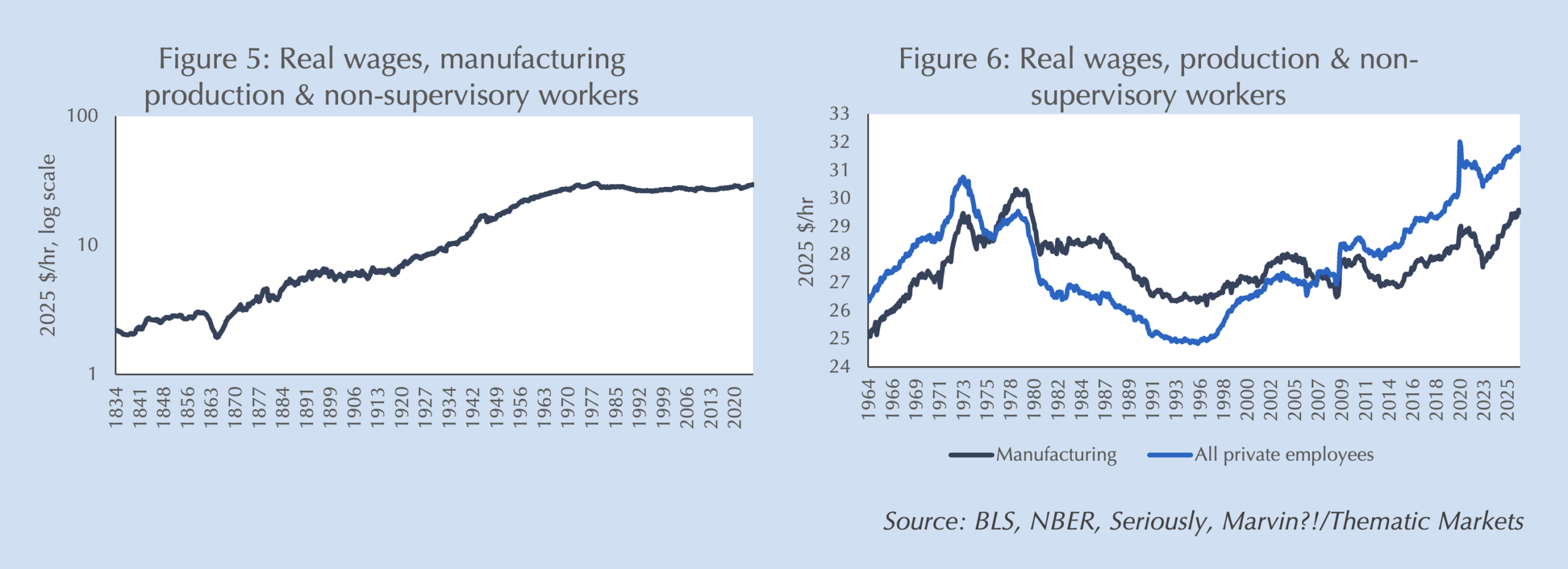

The reason is that an inflexible monetary regime – a fixed currency supply – forces all adjustment onto other economic variables. Thus, when the economy is hit by a supply shock, a productivity boom or a shift in demand, prices and output need to bear the burden of adjustment since the money supply cannot. As illustrated by the pre-Bretton Woods US economic experience, the resultant alternating bouts of inflation and deflation of as much as 30 to 40% per year played havoc with real wages (Figure 5). When inflation surged, purchasing power temporarily collapsed leading to a sharp drop in aggregate demand, and when deflation surged firms found it easier to cut labor en masse than sticky wages. The result was extreme economic volatility.

The cause of the Great Depression

Worse still, these adjustments can become self-perpetuating, resulting in much longer, more severe economic dislocations. That is exactly what turned a normal recession into the Great Depression. To defend US gold supplies the Fed raised interest rates, which pushed the US into deflation. Deflation raised real interest rates further since real interest rates are nominal rates less inflation, or in this case plus deflation. This pushed the US economy into a debt-deflationary spiral as rising real interest rates increased deflation (and defaults), which in turn raise real interest rates further. That’s why FDR’s devaluation of the dollar ended the Depression, because it broke the spiral by allowing the money supply to absorb the shock instead of output. Indeed, one can date the end of the Great Depression in every country studied to the day it left the gold standard.22 Taking the wrong lesson from that experience is why central bankers remain so fearful of deflation to this day. But the problem was not deflation per se – as Japan’s deflationary expansion of the 2000s showed – but rather an inflexible money supply.

Stagnant real wages

Still, many will point to flat real wages since President Richard Nixon floated the dollar as evidence that fiat debasement erodes real standards of living (Figure 5). But the end of gold convertibility is likely coincident with, not the cause of flat real wages. The first thing to note is that real manufacturing wages also stagnated for nearly three decades from 1892 to 1918, between the productivity booms driven by the Age of Steam and the Age of Electrification. (Notably, it also was the only period in US history whose immigration – an expansion of labor supply – neared the rate of the most recent period.) Second, if we zoom in on the post-Bretton Woods period in Figure 6, real wages rose amid the most intense inflation of the 1970s and have risen again since the middle of last decade, accelerating during post-Covid inflation. Stagnant and falling real wages largely coincided with the Volcker disinflation and subsequent period of low inflation from 1990 to 2014 that few Americans complained about. Finally, while manufacturing wages have yet to climb back to their 1978 peak in real terms, wages of all private employees – including managers and service employees – are at a record high in data going back to 1964.

Adverse labor supply shocks

Based on these observations it seems likely that real wage stagnation had more to do with globalized competition and a rising premium for intellectual capital relative to manufacturing skill, than it did the abandonment of gold convertibility. US workers faced increasing labor-supply competition from both globalization and immigration, and later saw their productivity eroded by Chinese economic warfare that systematically undermined the value of US manufacturing capital. Simultaneously, US workers were hit with the Information-Age technology shock that increased the returns to intellectual capacity relative to skilled labor. Software and financial engineers captured all the wage gains while the owners of intellectual property harvested a higher profit share of GDP.

The Roaring ‘20s?

These trends may be changing, just as they did in the 1920s’ Age of Electrification. As I’ve noted, the advent of artificial intelligence, especially large-language models, raises the relative value of manufacturing skills versus many white-collar jobs that have benefitted from the trends of the last five decades. But those gains also will accrue increasingly to the owners of the capital that are behind that transformation. More generally, the rise in worker productivity that follows will flow through to their real wages – even with a “debasement lag” – and ultimately to the products they purchase.

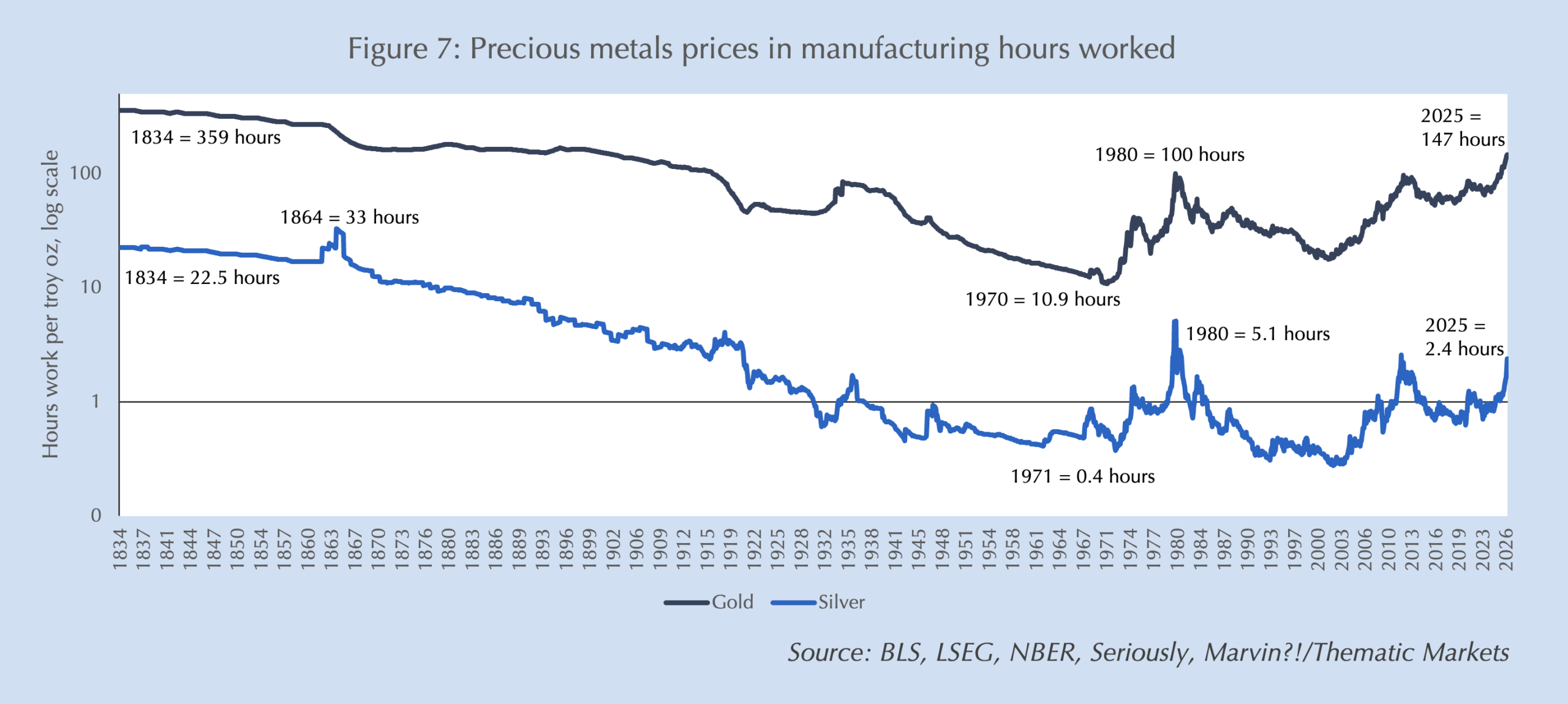

Choose the faster horse

What does that mean in an era of historic debt loads, geopolitical turmoil and erratic policymaking? The honest answer is that, even as relatively optimistic as I have been on the US outlook, I cannot exclude that the US doesn’t trap itself in a hyperinflation, or at least an extended period of high inflation that significantly undermines lagging wages’ purchasing power. What I can say is that long-run value doesn’t come from a non-producing asset stored in a safe. Figure 7 shows two centuries of gold and silver prices in terms of hours worked. Both bottomed out with the end of convertibility in 1971 and have risen (unevenly) since. But, remembering that their rise has accompanied the stagnation of real wages, both also show that productivity is the best long-run investment you can make. An ounce of gold is earned in 40% of the hours work it took two centuries ago and silver costs just 10% as many hours. Fiat debasement can’t stop that. While wages may suffer a lag amid rapid inflation, forward-looking equity prices will not.

Note: Starting this week, I will be cutting back the frequence of Seriously, Marvin?! to biweekly, from weekly. If you can’t get enough, remember that in the alternating weeks you can listen to me and Mark Farrington discuss global markets on the Thematic Edge Podcast. And, if you’d like to step up to my institutional-grade research, try subscribing at Thematic Markets.

Comments are available to paid subscribers only.