Impossible

Last week, on the social media platform formerly known as Twitter, aka X, I wrote that Bitcoin prices’ recent softness is consistent with “saturation” (or, full adoption). I based that claim on my “epidemiological” model of Bitcoin — i.e. modelling its spread like a pandemic — that not only captures how far through adoption we are, but what Bitcoin’s fundamental value is and what macro factors will drive its post-adoption price dynamics. Someone on X, apparently a true believer, responded, “So supply stops growing and price stagnates or falls? Impossible.” As crypto has become better known and held, its investor base has become more diverse, but its true faithful — “carriers” in my pandemic model — remain beholden to three myths about its underlying sources of value: the 21 million cap on Bitcoin supply, the “power-law dynamics” of its price, and that “nothing stops this train” to US debt oblivion. Let’s tackle each in turn.

A quick refresher on Econ 1

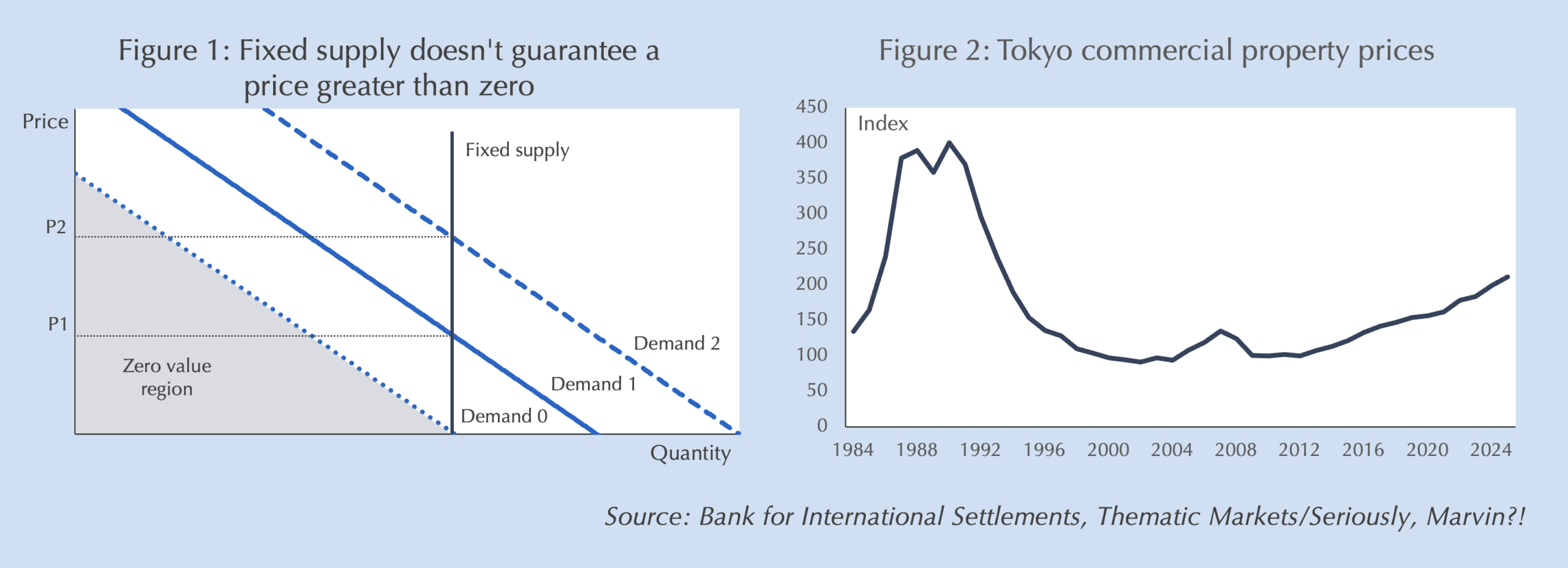

For many Bitcoin believers like my interlocutor on X, a sufficient indicator of value is that its supply growth is algorithmically limited to 21 million bitcoin, which it is on pace to hit around 2140. But as any Econ 1 student should be able to tell you, prices are determined by the intersection of supply and demand. Demand can and does fluctuate, even if the supply of something is fixed. Figure 1 shows the effect on price of varying demand with a fixed-supply cryptocurrency. As demand expands from “Demand 1” to “Demand 2” — for instance, rising crypto adoption, or an increase in the size of the economy — the price rises from P1 to P2. But if instead demand falls, the price can fall, even to zero, as illustrated by any demand curve below “Demand 0” in Figure 1.

Yes, it is possible

For some ideological believers in Bitcoin it appears inconceivable that demand could fall. If you truly believe in Bitcoin as the future of money, how could demand possibly fall? But the history of land prices, art prices, jewelry and even Beanie Babies — yes, they too had an intentionally fixed supply to support prices — show that demand can and does fall sometimes, and even completely evaporate. Famously, at the height of Tokyo’s property price bubble, the Imperial Palace in the city center was ostensibly worth as much as the entire state of California. But Tokyo property prices today are worth little more than half of their peak values in 1990. The supply of Tokyo real estate didn’t increase, but the value of the goods, services and wealth supporting it collapsed. The same thing happened in Detroit when the American auto industry went into decline. In the 1950s it was a glittering, wealthy city known as the “Paris of the Midwest.” But fortunes changed and by the 1990s many houses literally couldn’t be given away. Or, take art as another example. In the late 1800s the works of painters William Bouguereau and Jean-Léon Gérôme were all the rage, fetching extraordinary prices. Then Impressionism was born and no one even wanted a two-for-one deal on Bouguereau and Gérôme.

Relative demand…and supply

It is not a given that demand for Bitcoin will continue forevermore, or perhaps even until the last halving in 2140. Even if cryptocurrencies are not crushed by sovereigns protecting their seigniorage — revenue earned from issuing money — Bitcoin’s value may be eviscerated by new technologies or its molasses-running transaction speeds. The end of mining subsidies, vulnerability to quantum computing or some other unforeseen technology may obviate Bitcoin’s mission or security, undermining belief in its future value and leading to a collapse in demand. But even if we assume that Bitcoin or its “Layer 2” derivatives do become the universally accepted, dominant world currency, it would still be subject to relative demand shocks. The prices of gold, silver and their minted monies of the past all fluctuated with economic conditions as demand changed relative to (roughly fixed) supplies. If the global economy has a recession or the world population shrinks, Bitcoin demand and its price likely would fall as its relative supply increases versus goods and services, even though its absolute supply remains fixed.

Who’s gonna enforce the “power law?”

What about “power laws?” Read enough Bitcoin blogs and you will invariably come across this “model” of Bitcoin and other cryptocurrency prices.1[1] The idea is that because Bitcoin has a fixed supply, as it grows through network effects — I tell 10 friends, then they tell 10 friends, et cetera — the price grows exponentially, i.e. e¹⁰ᵗ, where e is a constant that grows at the “power” of 10 x time, t.2[2] The problem with this “law” is who enforces it? It only works if adoption continues to grow, which assumes an unlimited supply of humans and that every human is equally likely to adopt it. Neither of those assumptions are true.

A different power law: S2F

A related concept is the so-called stock-to-flow (S2F) “model” that models the price of Bitcoin as a function of the ratio of the outstanding stock of coins to newly created coins. Miners are paid a “subsidy” of newly created Bitcoins for crunching the numbers to calculate each new transaction (“block”), but the Bitcoin algorithm halves the subsidy roughly every four years. S2F thus implies that Bitcoin’s price should double about once every four years, or 2ᵗ⸍⁴, another power law. But S2F also faces “enforcement” issues. First, it implies that Bitcoin’s price goes to infinity (as the flow term approaches zero, the stock-to-flow ratio approaches infinity) when Bitcoin “halvings” cease as supply reaches its fixed 21 million cap, just as miners would lose (most of) their incentives to do transaction verification. Second, it runs into the same “demand” problem noted above: why would demand continue if the price went to infinity?

“Models” versus models

I put quotation marks around “model” for both power laws and S2F because they aren’t really models, they’re just deterministic trends fit to Bitcoin’s observed price history. If you think that’s useful, please look up Tyler Vigen’s “Spurious Correlations” to see how you can fit almost any two trending series (“non-stationary” in statistical parlance), whether they are the distance from Neptune to the Sun and US burglary rates, or the popularity of the first name “Brooklyn” and UFO sightings in Kentucky. In contrast, a true model postulates a theory — why something happens — and tests it with statistical methods that account for potential non-stationarity.

Logistic, not exponential growth

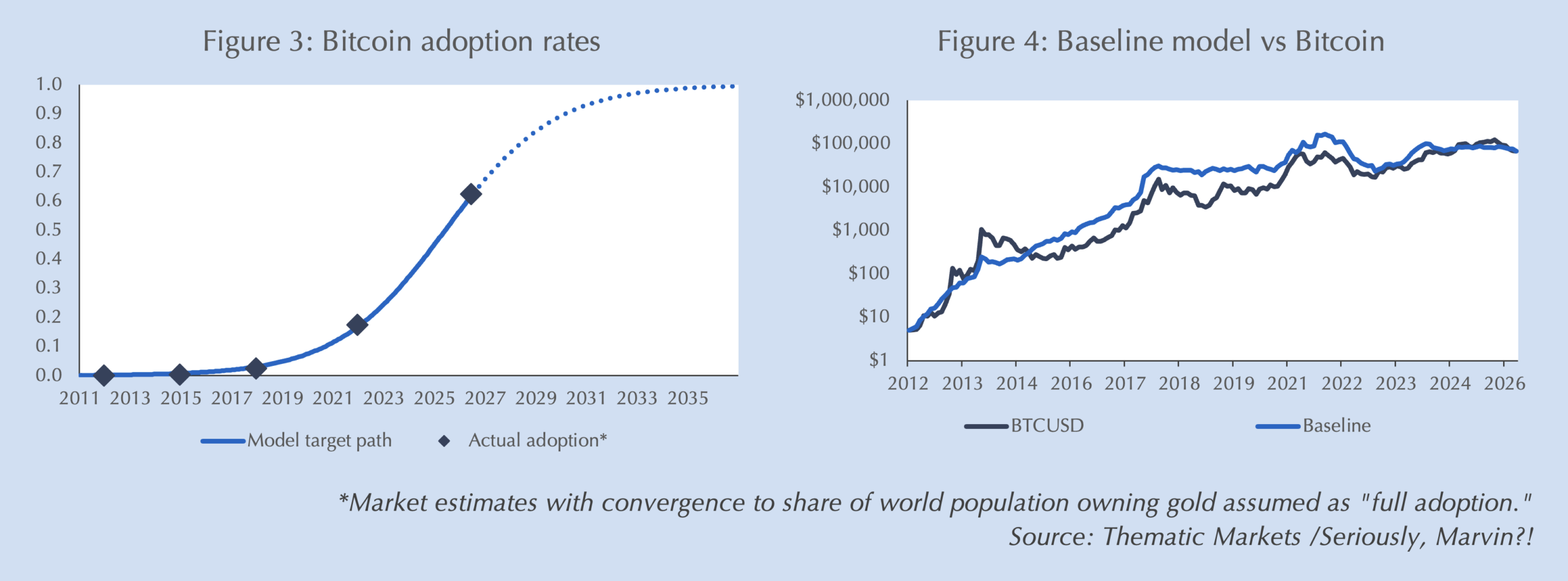

This is exactly why I modeled Bitcoin as a pandemic, because that’s how any new technology, particularly a networked technology, grows and spreads. Initial adopters are outliers and their random contacts grow slowly. But as the “infected” population increases the network effects create exponential growth (the “power law” phase). Eventually, explosive growth makes the new technology “endemic” — most people have it — and growth slows as the “uninfected” become rarer within the population. This creates a logistic growth path — a flattened “S-curve” — shown in Figure 3 rather than a continuous exponential path. I used industry estimates of the number of Bitcoin holders — direct and indirect — for a number of years and fit them to a logistic function that assumes full adoption is equal to the share of the global population that owns gold as an investment. The fit, as shown by Figure 3, suggests that we’re nearly two-thirds of the way to full adoption.

Adoption isn’t everything

Fitting a logistic function to estimates of Bitcoin holders is no more a model than a power law or S2F ratio, but it provides the theoretical foundation for a model that helps explain the exponential trend in Bitcoin prices’ growth over the last decade while rapid adoption was taking place. A fuller model should better explain the “wiggles” along that trend with fundamental variables associated with economic and political conditions, which my full epidemiological model does, as shown in Figure 4. The advantage of embedding “pandemic” adoption within a structural model of Bitcoin’s macroeconomic drivers is that it not only captures exponential demand effects during adoption (and gives you an estimate of how far through adoption we are), it isolates the additive effects of macro variables that help explain both past “wiggles” and future price dynamics once we reach full adoption and the end of halvings.

“Nothing stops this train”

Among the variables included in my model to explain Bitcoin’s price dynamics are changes in the Fed’s balance sheet and US fiscal deficits. The latter are a specific focus of the high priestess of Bitcoin and master of memes, Lyn Alden, who has popularized the mantra “nothing stops this train” in reference to the unsustainability of US fiscal expenditures. According to the Alden view, unsustainable fiscal paths in most major economies, including the world reserve currency issuers, the US, are not correctable and will eventually be monetized — governments will print money to fund deficits — causing hyperinflations that will push citizens everywhere to Bitcoin or other cryptocurrencies. While I strongly share Ms. Alden’s concerns about global debt sustainability and the US in specific, perhaps because I’ve lived through other such panics about US finances, I don’t think they’re uncorrectable and, as I’ve written, the US has compelling geopolitical interests in avoiding both debt monetization and default.

The ultimate irony

Ironically, I think Bitcoin holders have far more to fear from US default or monetization than stand to benefit from it. Indeed, in my view, Bitcoin only has long-run value because the US now endorses cryptocurrencies as independent payment rails and that a US default or debt monetization would lead to Bitcoin seizures and transaction bans (as China has). The US adoption of crypto payment rails to block China’s efforts to capture third countries within its proprietary payment systems requires the US to not only accept but protect crypto as a tool of dollar hegemony. But if the US ever required debt monetization or default, it would immediately ban crypto payments — and likely seize “illegal” cryptocurrency holdings — just as Franklin Delano Roosevelt’s government banned private gold holdings when it devalued the dollar by 50% in 1933.

They have guns

Crypto believers like to believe that their “digital gold” stored on private wallets and slipping across borders like electronic quicksilver will be immune from such actions. It won’t. The sovereign always wins and in the long run no government is going to yield its monopoly over seigniorage willingly. Hence, why governments through time have been able to use monetization as a means of debt finance in times of trouble. Even amid the worst hyperinflations in history, most people have been trapped using government-issued currency, not because they were foolish or lacked alternatives, but because their governments had guns (or spears) and enforced the use of their currency in most transactions. Taxes will be required in government-issued scrip, banking licenses will enforce use of government currency, ditto medical licenses, permits to rent or sell property, or even run a grocery store. What good will your Bitcoin be if you can’t buy food, pay rent or get healthcare with it, and risk arrest just for owning it? You don’t have to imagine it: it’s life today in China. Cryptocurrencies are increasingly traceable and all the on- and off-ramps to the financial system can be controlled. You won’t escape.

Comments are available to paid subscribers only.