Brexit 10 years later

Last week marked the ten-year anniversary of the United Kingdom’s vote to leave the European Union. I had anticipated the result, in part based on the research I was doing for The Politics of Rage, which I had started about six months earlier. I also forecast that it would not be the economic trauma that most economists expected, nor would it threaten London as Europe’s financial capital. But I didn’t get everything right. While I nailed sterling’s pre- and post-vote plunges, I wrongly assumed that the financial fallout would be global based on my (correct) analysis that Brexit was the opening salvo in a rising tide of populist rebellions across the West. More consequentially, I forecast that within a decade the UK would prosper relative to its neighbors from its exit. That didn’t happen and it’s worth exploring why as the UK undergoes (yet another) leadership change.

Not a significant economic event

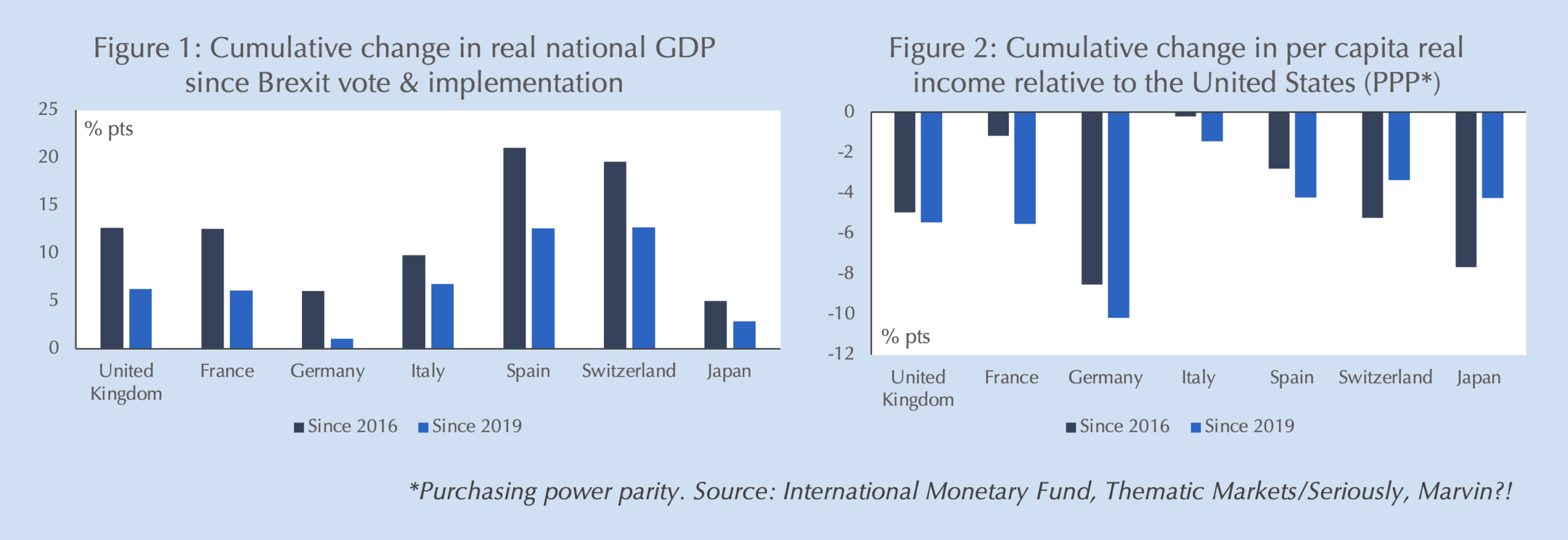

Contrary to the predictions of most economists, the UK economy weathered Brexit without problem. In 2017, the UK grew faster than any other major economy in Europe. Brexit wasn’t implemented until 2020, which was the same year as Covid, making it difficult to isolate its effects. But a comparison of cumulative economic growth in the UK and its peers since either the referendum or implementation suggests that, contrary to all the hype, Brexit was not a significant economic event for the United Kingdom (Figure 1). Versus major EU economies, the UK underperformed Spain, grew on par with France and Italy, and significantly outpaced Germany. Outside the EU, Switzerland grew much faster but Japan grew at half the UK’s pace. Population growth rates account for much of the difference with Japan, Spain and Switzerland, as shown by changes in per capita income (PCI) growth in Figure 2, further illustrating that Brexit did no clear harm to the UK relative to its peers. Well, most peers: Figure 2 is expressed in changes in PCI relative to the US and makes clear that everyone lost ground to America.

Gravity is constant

Leaving aside US outperformance for a moment, why wasn’t Brexit the disaster that most economists forecast? There was no UK recession or even any clear difference in growth with European peers over a decade. Much of the answer lies in a misunderstanding of the so-called “gravity” model of trade, perhaps willfully on the part of Remain-leaning economists.1[1] Most analyses focused solely on the marginal effects of changes in tariffs on economic growth, ignoring the other inputs to the workhorse model of international trade. At one level, this was sensible: tariffs were the primary (measurable economic) variable that was changing. But by doing so, these analyses ignored the dominant variables the gravity model. As its name implies, by far the most important determinant of trade flows in the gravity model — two to three times the magnitude effect of any other variable — is distance from trading partners. Brexit didn’t increase the geographic distance from Europe, so only a massive increase in tariffs could significantly disrupt the UK’s trade with Europe.

Falling off a pancake

Yet that was never in the cards. Before Brexit the UK faced zero tariffs on its exports to the EU and 2-3% weighted-average tariffs on its exports elsewhere.2[2] Even if the EU applied its “Common External Tariff” to the UK, it would have been only 5%, well below average annual exchange rate volatility.3[3] Furthermore, the UK is important to the EU, too. As a result, Brexit negotiations yielded weighted-average tariffs on UK exports to the EU of just 0.3% and 1-2% for exports to the rest of the world.4[4] As an old boss of mine liked to say, “You can’t fall far off a pancake.” Ironically, the weighted-average tariff bill on UK exports likely fell (marginally) due to Brexit. This of course ignores costly non-tariff barriers like customs, rules-of-origin documentation, and other regulations that changed due to Brexit, but it highlights a critical issue many economists got wrong.

Cutting loose the EU anchor?

Yet tariffs aren’t even the second-most important determinant of trade after gravity (distance): trading partners’ economic growth rates are. In that sense, the UK also has benefitted by reorienting its trade away from the anæmic growth of the EU towards faster growing economies elsewhere. Yet, as noted, gravity is still the most important determinant of trade, meaning that the EU’s poor economic performance remains an anchor holding back UK growth.

American exceptionalism

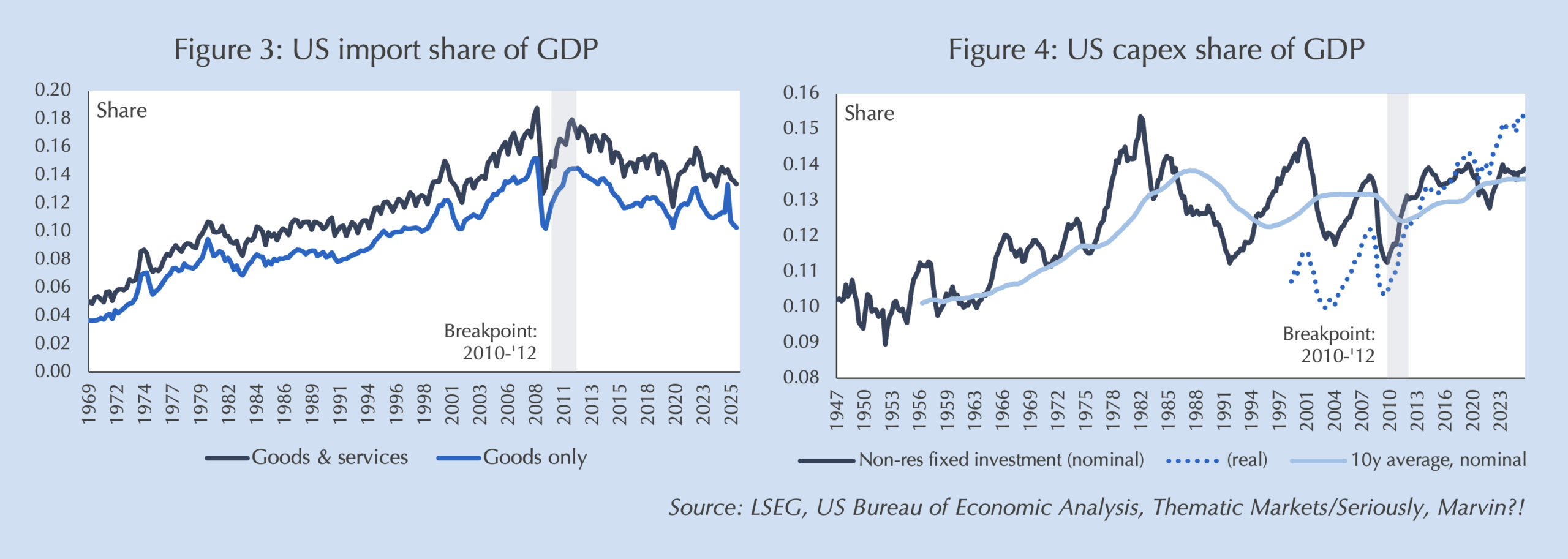

While the importance of gravity, microscopic tariff changes, and improvement in trading partners help to explain why the UK hasn’t suffered relative to the EU, Switzerland or Japan, it doesn’t explain why everyone fell behind the US. In the context of the Brexit debate, US absolute economic outperformance is even more striking given that the trade share of its economy, particularly its import share, has been falling since 2012 (Figure 3). US import compression — the US produces more of what it consumes on a gross basis (not net) — goes hand in hand with the US investment boom that coincided with it, an investment boom that is now the cumulatively largest of the post-War period. For all those claiming the US economy is wholly carried by AI and datacenter investment take note that this boom started a decade before the introduction of ChatGPT and that manufacturing comprised over 50% of the announced corporate investment in the US last year.

Going local

This is the US automated Localization boom that I’ve been writing about for a decade and using to forecast all the things most others have missed: persistently higher US GDP growth, real interest rates, corporate earnings, and US dollar. Sources of US growth, which have always been more dynamic and self-generated, have become even more so. The driver of Localization has been replacement of less efficient global supply chains with localized automated production, a phenomenon that started before, but has been reinforced by trade wars, Covid and the faltering global order. When a robot is cheaper than the cheapest skilled worker abroad, why locate your factories anywhere else?

America alone

Yet, my research into Localization has revealed a strange anomaly: the US appears to be the only place where it can be clearly identified. There are some signs that it may also be taking place in Switzerland (perhaps explaining its strong exchange rate) and Japan (whose exchange rate would suggest the opposite), but the evidence is not clear. When I’ve dug into what economists might call the “micro foundations” of Localization there are several US-specific factors that appear to facilitate it: strong entrepreneurship, top-flight research universities with well developed venture capital “eco systems” that help spread new technologies into businesses, and large, active private capital markets that are willing to finance expensive, perceived risky transitions from globalized supply chains to localized production.

Localization lost

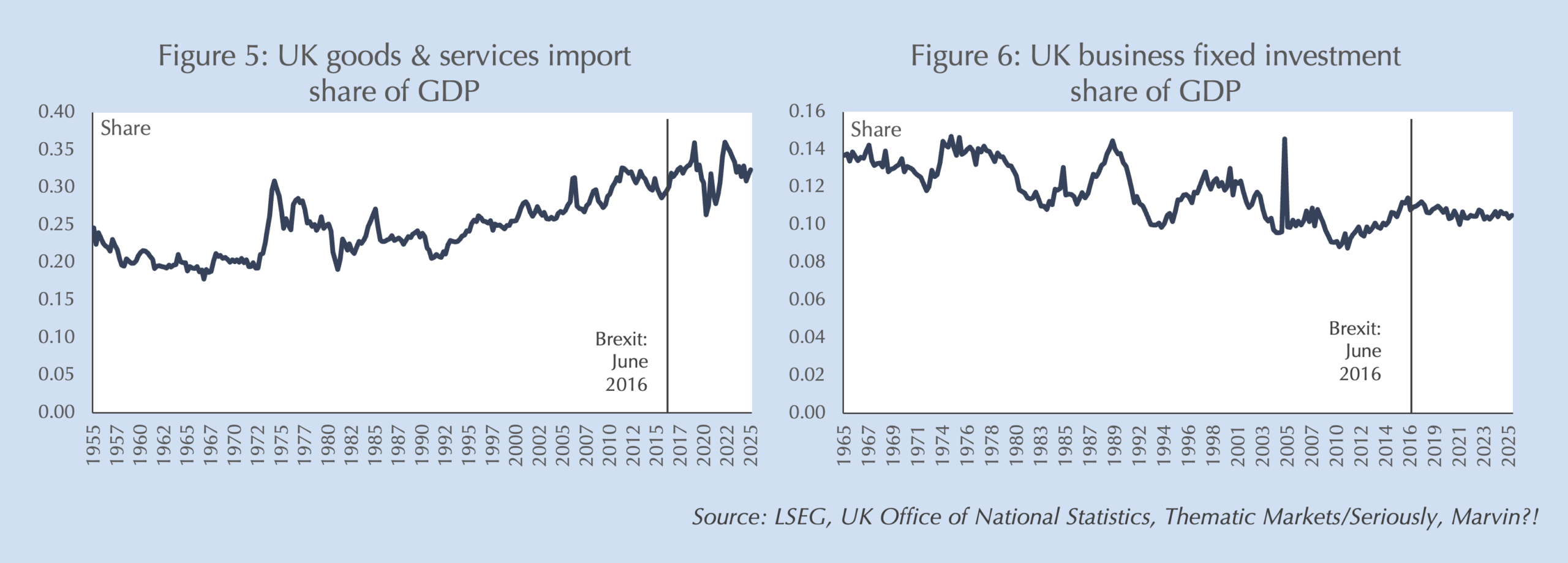

Those “US-specific” factors do exist in another country: the United Kingdom. Entrepreneurship is so native to the country that Napoleon famously called England “a nation of shopkeepers,” only the UK has a large number of top-research universities to rival the US, the Cambridge-London corridor is the most well developed venture capital ecosystem outside of America, and London is the premier non-US center for private capital. For these reasons, my research into Localization had led me to expect the UK to prosper once it cut the cord from a European Union that seems to delight in crushing entrepreneurship and innovation. Yet, the opposite happened. Over the last two decades the import and investment shares of the UK (Figures 5 and 6, respectively) do something very curious. In 2010, as in the US, they begin to reverse their three-decade trends of rising imports and falling investment. But, unlike the US, the reversal reverses itself following the Brexit vote.

Bizarre Brexit backtrack

How do we explain Britain’s bizarre Brexit backtrack: just as technology and means of production were poised to advantage an independent Britain, an economy that was naturally predisposed to Localization and appeared to be the only one following the US lead, suddenly reversed course. There are three possible explanations in my view: collapsed confidence, bad policies and insufficient scale.

Confidence game

The swiftness of the reversal suggests that psychology played an important role. While Brexit was greeted with jubilation by its mostly working-class and non-London supporters, it was a profound and unexpected shock to its opponents who disproportionately comprised the governing, business and media elites. When the referendum’s results were announced I saw numerous people publicly weeping on the London trading floor I worked on at the time. Since elites make most business investment decisions, it is unsurprising that a major shock to their world view would suppress their animal spirits. Newspaper headlines, written by other elites, predicting dire consequences only reinforced the gloom, despite those dire predictions being repeatedly proven wrong over the last decade.

Biggest own goal in history?

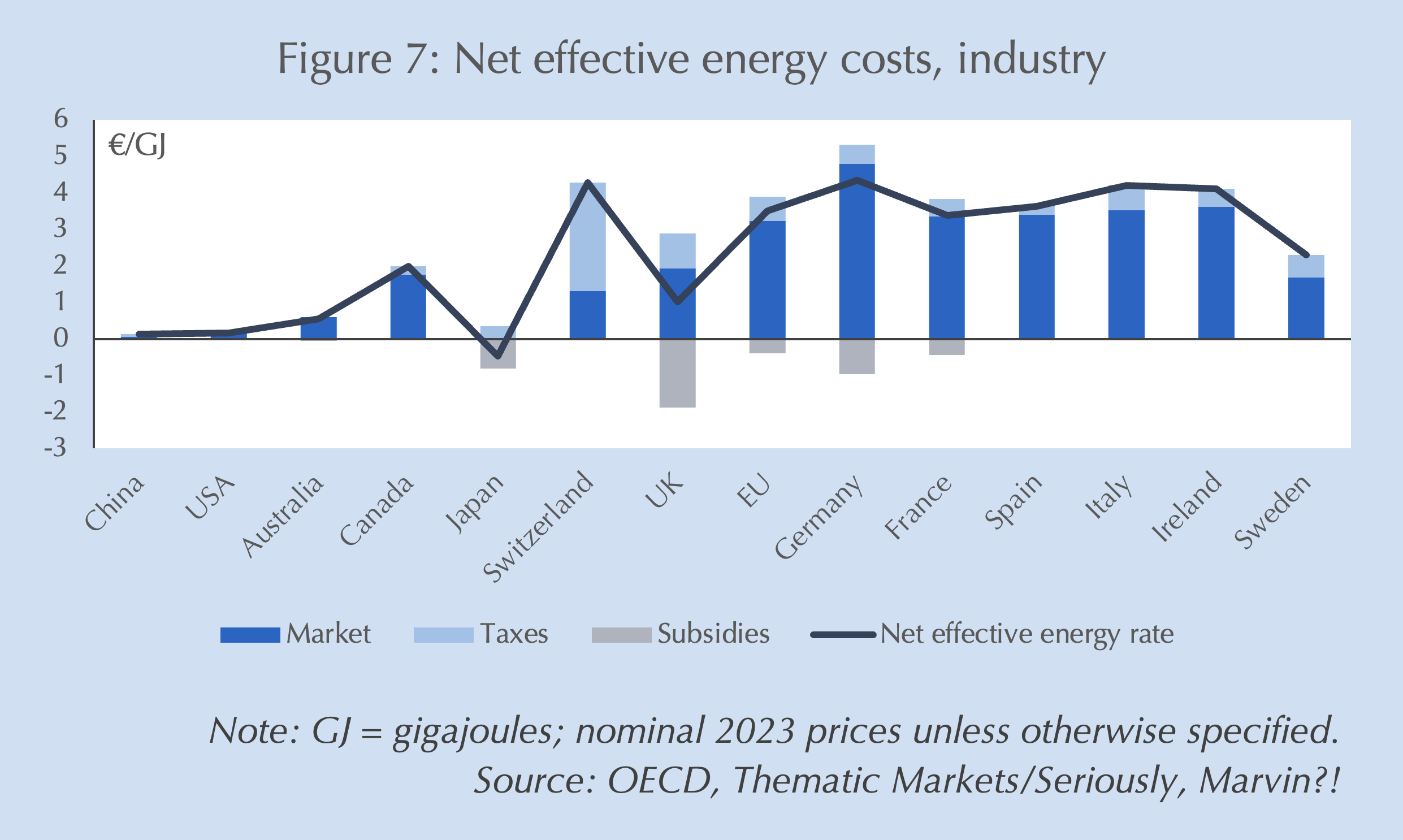

While they are unlikely to have been responsible for the initial reversal, bad policies almost certainly sustained the malaise. Pre-Brexit polling indicated that sovereignty over lawmaking was the primary driver of “Leave” votes, yet in what might be the biggest own goal in history, governing elites from all major parties agreed on wholesale adoption of EU rules and regulations. Thus, Brexit as implemented delivered the worst of all worlds: border frictions, red tape and (marginal) tariffs where none had existed, but without the freedom to innovate, deviate and re-imagine both trade with the rest of the world and within the UK. Energy policies compounded the error. The UK also adopted the EU’s energy suicide pact (perhaps even accelerated it under the current Parliament). In a world increasingly defined by national-security driven re-industrialization and an arms race for artificial intelligence supremacy, both of which require gigajoules of energy, pursuing policies that result in energy costs for industry that are 6-8x those of China and the US is a massive deterrent to investment (Figure 7).

Too small?

A final cause may be that the UK is just too small an economy to attract sufficient Localization demand. That would also help to explain why the US is such an outlier, being the only economy to show it unambiguously. Yet, this is at odds with tiny Switzerland showing signs of Localization but the large EU showing none. The UK’s pre-Brexit signs of Localization and abrupt reversal thereafter also argue against this hypothesis.

The Burnham question: As predicted?

Enter Andy Burnham, Manchester’s former mayor and, with Sir Keir Starmer’s resignation, presumptive UK Prime Minister. Unlike Sir Keir whose rise was guided by former Prime Minister Tony “Third Way” Blair, Mr. Burnham is seen as a staunchly working class man of the Left. In those characteristics he well fits my predictions ahead of the 2024 election that Sir Keir would be ousted in favor of a Leftist premier who would take command of the massive majority Sir Keir delivered to Labour. In a country that already suffers from nose-bleeding taxes that still fail to cover its benefits bill, that path will almost certainly deepen the country’s malaise.

Or Nixonian?

But there is a different path that perhaps only Mr. Burnham could manage: like arch-anticommunist Richard Nixon going to China, Mr. Burnham could cut free from EU rules and rein in “Net Zero Tzar” Ed Miliband’s growth-killing energy policies. Mr. Burnham politically defines himself as a Northerner, coming from a region that voted strongly for Brexit and swung temporarily to the Conservatives on (false) promises to deliver on those voters’ intent. As Mayor of Manchester he aggressively pursued devolved education reforms promoting trade skills that not only likely better suit a world of AI and re-industrialization, but reverse Mr. Blair’s push for everyone to attend university and challenge traditional Labour demands for centralized control of education.5[5] His reforms align well with Leave voters’ preferences to “take back control” of UK laws. Mr. Burnham hasn’t tipped his hand yet on energy policy but it is reported that he is being strongly lobbied by trade unions to exclude Mr. Miliband from a list of possible Chancellors of the Exchequer.6[6] If Mr. Burnham uses Labour’s majority to free UK regulations from the EU, reduces domestic energy costs and takes some steps toward fiscal sustainability, the combination likely would help break the UK free from its economic (and political) lethargy.

I’ll believe it when I see it

Will Mr. Burnham be the Leftist whose coming I prophesized? Or a Nixonian surprise? I suspect the former and hence retain my bearishness on the UK economy and sterling. But the incentives strongly align for Mr. Burnham to take the Nixonian path. Bond markets are unlikely to accommodate even short-term pump-priming fiscal policies leaving any incoming Labour prime minister with a choice: More of the same that killed Sir Keir’s premiership? Or a radical turn to support private-sector growth?

Comments are available to paid subscribers only.