Time flies when you’re having fun

Less than two years have passed since I wrote Global entropy: Enter the dragons, but many of the things I predicted already have occurred or at least rhymed with subsequent events. The most consequential development has been the re-election of Donald Trump. His shift to La Cosa Nostra realist foreign policy from America’s post-1992 turn to moralist policing likely has put the path of Global entropy more firmly on an evolutionary path, albeit at a cost of “fatter tails” in the distribution of risks. For all the noisy outrage in Western capitals – and contrary to the consensus echo chamber’s assessment – President Trump’s sharp course correction likely has caused more behind-the-scenes angst and debate in Beijing and Moscow.

Already prescient?

Before addressing the more consequential implications of President Trump’s policy U-turn and its consequences, with your forgiveness at what could come across as self-congratulation, I’m going to start with a list of other risks that I flagged. A remarkable number already have occurred, in many cases affecting the likely path of Global entropy. Among those that have eventuated already, at least in some form are:

- An evolutionary path of Global entropy will default to Global bifurcation: I wrote that “The geostrategic implications of Global entropy, acceleration of increasingly specialized technological advancement, and path dependence are pushing the global economy and military power towards Global bifurcation.” The contours of bifurcation already were becoming apparent by the time I wrote that but are clearer now in the increase in technology and export controls between the West and China, President Trump’s use of coercive tariffs to exclude China and apparent success in negotiated trade deals, and the battle over international payments systems.

- Increasing Global bifurcation would lead to economic coercion: Among the results of that bifurcation, I predictedthat as “Localization replaces outsourced global supply chains…The interdependence of suppliers and procurers in the globalized system likely will yield to greater coercive power of technology leaders [China and the US], via export controls, over increasingly supplicant trading partners.” Both China and the US (hat tip The Brawl Street Journal) have engaged in exactly these tactics.

- Increasing power of resource producers: Another implication that “one group of exporters likely will retain power over the technology originators in the new economic order: producers of essential natural resources, especially those needed for advanced technologies (critical minerals) and the functioning of economic activities (energy).” The Trump Administration’s resource nationalism at home and competition with China for resource control abroad illustrate the reassertion of resources as the other axis of power to technology (hat tip Doomberg).

- US adoption of stablecoins as an independent payments system: The passage of the GENIUS act directly fulfilled my prediction that the US would move to thwart China’s efforts to capture client states with its own centralized payments system by supporting the “emergence of independent blockchain-based payments systems.”

- Iran, Turkey and Israel redraw Middle East’s Sykes-Picot boundaries: The trigger and final outcome – that excluded Iran from the spoils – was different than the scenario I imagined, but the effective outcome was the same: Syria was carved up into Turkish and Israeli “buffer” zones with an “independent” Syrian state in the middle.

- India-Pakistan war: Again, not the exact scenario that I predicted, but the two countries did engage in a skirmish that, thankfully was less significant than I feared. The conflict also well illustrated two broader predictions that I made regarding India’s place in a bifurcated world and China’s military capabilities.

- India will be pushed to the West by China amid Global bifurcation: I postulated that in a bifurcated world, India will be pushed to the West by rivalry with and fear of China. Despite all the commentary to the contrary, as I justify below, I’m going to claim this as a win.

- China already is a peer military competitor to the US: The efficacy of China’s J-10C fighter aircraft and PL-15E beyond-visual-range, air-to-air missiles, used by Pakistan in the conflict with India, demonstrate that China’s indigenous military technology well competes with advanced Western weaponry.11 Note, these were China’s export weapons. The J-10C is a “4.5-generation” aircraft whose original airframe is now 30 years old. Last December, China showed off two prototype sixth-generation stealth aircraft ahead of Western sixth-gen development.22 As if to drive home that point, China’s 80th Anniversary Victory Parade displayed a modern military whose inventory is significantly newer and may outclass the West in some dimensions.33

- US civil war: I included in my definition “sustained low-grade terrorist activity,” hence will give myself partial marks for this. The assassination of Charlie Kirk, which has enflamed tension all around, is emblematic but only one of several instances of increasing political violence. There was the attempted arson of Pennsylvania Governor Josh Shapiro’s home in April, the assassination of Minnesota state lawmaker Melissa Hortman, and violent riots in several West Coast cities in June that included attacks on law enforcement officials.44 But more troubling was the pre-meditated anti-government attack in early July that was largely ignored by the media. Ten well-armed, body-armored Antifa insurgents lured two US Immigration and Customs Enforcement (ICE) agents into an ambush at an Amarillo, Texas detention center and fired upon them (hat tip Gray Zone Research).55 The incident was one of a surge in attacks on ICE agents this year.66

Misses? Or not yet?

I also enumerated several risks that have not (yet) eventuated: a Chinese invasion or embargo of Taiwan, an Iran-Saudi war, European Monetary Union dissolution, Nigerian, Chinese, or Russian civil wars, debt crises, defaults, and hyperinflations. Importantly, I highlighted these, as with the above, as underappreciated risks, not forecasts. The surprise is that so many of the things I highlighted as risks have indeed occurred in one form or another. As I have written, I still worry greatly about a hostile attempt by China at Taiwan reunification, EMU dissolution especially with the mainstreaming of dollar stablecoins, and debt-related crises.

My most significant prediction still outstanding

Only time will confirm my most consequential prediction – that Global entropy is inevitable, but adaptation may slow it down – and that without that adaptation the West “risks a disorderly descent into a Complexity cascade with attendant increase in geopolitical, economic and market Uncertainty.” But my assessment of the developments since I wrote that are that America’s radical turn in foreign policy has hastened the path to Global bifurcation while reducing the risks of calamitous disorder. Yet, those risks remain substantial. As I described in Fire Marshal Trump, President Trump’s high-stakes gambling approach to policy often improves the central tendency (most likely outcome) while at the same time raising the risks of more extreme outcomes.

From a “bimodal” to a “fat tailed” future

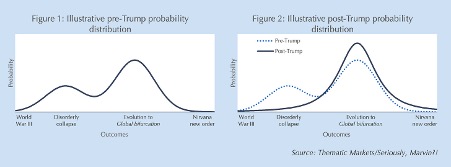

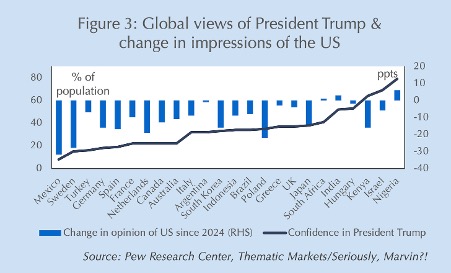

This point is a bit hard to conceptualize but I’ll try. In Enter the dragons, I postulated a “bimodal” future, i.e. one with two most likely outcomes as represented in the figurative probability distribution in Figure 1. The more likely outcome (the higher of the two probability “hills” in Figure 1) was evolution to a new world order of Global bifurcation. The other, less likely but still meaningfully probable outcome was a rapid collapse of the post-War liberal order (PWLO) into disorder (the smaller hill). Incineration in “World War III” or lucking into a new “Nirvana” world order also were possible, just much less likely. In my view, President Trump’s shift of US (and ultimately Western) policies has put us much more firmly on an evolutionary path to Global bifurcation – the highest probability peak in Figure 2 – decreasing the bimodality. But the risk of disorderly collapse remains high and the extreme outcomes of “World War III” and “Nirvana” may be even higher than before, i.e. the distribution has “fatter tails.” (Note: Figures 1 and 2 are illustrative, not based on any model.)

Altering course

While President Trump’s “Revolution” in American policy is even broader, there are five critical changes he has made to US (and ultimately Western) policy that shifts the distribution of outcomes as described in Figure 2:

- Shifting diplomacy from values evangelism to La Cosa Nostra realism to arrest the West’s cultural repulsion of non-Western countries;

- Countering China’s economic warfare to reindustrialize the US;

- Pushing US allies to step up to their own rearmament and reindustrialization needs;

- De-risking the international environment and returning the US to its pre-1992 policy of off-shore balancing; and

- Opening the door to Russia in an attempt to split it from China.

Losing India and the world order

The 25th Shanghai Cooperation Organization Council (SCO) two weeks ago caused much tut-tutting from the global commentariat that President Trump’s bullying had pushed India into the arms of Russia and China, creating a rival new order. But they seem to forget that Prime Minister Modi also attended the SCO in 2022 and that, while India boycotted the 3rd Belt and Road Initiative Forum in 2023 (as it had with the previous two), the latter meeting also was widely (and wrongly) described as establishing a new world order. Nothing substantive was agreed at the SCO, which was largely a photo-op that Beijing, Moscow and New Delhi all used for differing purposes.

Reality bites

But photo ops are not reality; they are a projection. No doubt, Prime Minister Modi sought to send a message to Donald Trump that India has alternatives to American tariffs. But it is a hollow threat, hence President Trump’s sardonic tweet that “Looks like we’ve lost India and Russia to deepest, darkest, China. May they have a long and prosperous future together!” The reality is quite different for both India and Russia. India was recently (again) invaded by China, a country that arms its mortal enemy, Pakistan, and is surrounding it in the Indian Ocean with naval bases. Realistically, it is not going to abandon the US over tariffs while it needs US arms and technology to resist Chinese domination, a point reinforced by the latter’s 80th Anniversary military parade.

Splitting up the Sino-Russian duo-pole

Russia, for its part, was humiliated by China offering nothing more than a memorandum of intent on the Power of Siberia 2 natural gas pipeline the two countries have been negotiating for two decades (see The Brawl Street Journal‘s excellent analysis).77 As President Putin smiled and joked with President Xi during China’s military parade, it’s hard to believe that he didn’t share India’s fear of the demonstration of China’s superiority in indigenous military-technology, production, and force of arms. The Trump Administration’s carrot-and-stick approach to end the Ukraine war aims to capitalize on both Russian and Indian fear and mistrust of China, as well as the two countries’ long, friendly history. While the ploy to split Russia from China remains a long shot, it isn’t implausible in the absence of Western repulsion, and would greatly reduce long-term risks to global stability.

Base interests over culture

President Trump’s La Cosa Nostra toughness risks injuring Indian pride, but its foundation in geopolitical realities is, for many countries a welcome change in US foreign policy. While the polling in Figure 3 took place before the US raised tariffs on India to 50%, India is one of three countries whose view of the US has improved – from an already high level – since President Trump was elected. As I noted in Values aren’t universal, but power is, President Trump is viewed much more favorably outside the West, in part because he eschews promotion of “universal” values and speaks to those cultures in the truly universal language of power.

No where else to go

For different reasons, other Western countries may be similarly offended by President Trump’s bullying, but they have no realistic option for alternative alignment. Culturally, they are far more aligned with the US, with or without President Trump; their economies are deeply intertwined with the US; and they lack the means to defend themselves in an increasingly dangerous world. This is why, despite all the public grumbling, Western nations have all agreed to increase defense spending and – with a few holdouts – largely agreed to President Trump’s re-writing of trade rules.

Shoring up defenses

In addition to getting NATO and Western Pacific allies to step up, the US is moving aggressively to reindustrialize itself, prioritizing its defense industrial base, and de-risking its security commitments through off-shore balancing to improve its defensive position. The Ukraine war remains unsettled, but the Trump Administration has prioritized resolution and has gotten Europe to agree to take the primary role in enforcing an eventual peace. Similarly, in the Middle East it used Israeli arms to largely neutralize Iran’s ability to disrupt the region, while delivering the final knock-out blow itself.

Clearer path, but still with big risks

Taken together, I see these developments as reducing the risks of a more rapid, chaotic disintegration of the PWLO. Instead, a sustained evolutionary path of Global entropy into a new order of Global bifurcation seems increasingly likely. But all these policies are big gambles that have extreme risks. The pace and wide extent of change being pushed by President Trump also risks a Complexity cascade into the unknown. Investing in this environment means choosing sides carefully in international asset allocation: the returns to China-allied countries are likely to underperform. But the extreme risks mean that a well hedged, tail-protected portfolio is necessary even if you do pick the winners.

Comments are available to paid subscribers only.