Le petit problème Pettis du laissez faire

Last week one of my oldest friends sent me a YouTuber’s critique of Michael Pettis, a man described therein as “one of the most influential economists” you’ve never heard of. I reference Mr. Pettis all the time, so if you’re a long-time reader or follow me on X where I regularly retweet his insights, you probably have heard of him. If you haven’t, don’t worry, I’ll explain.

I’ve followed Mr. Pettis’s writings for two decades and interviewed him almost a decade ago. For most of that time he was familiar only to China watchers as one of the leading analysts of its economy. But lately, as his ideas have been used to justify trade restrictions on China, he has come under attack as an economic radical who threatens laissez-faire, free-market economics. Nothing could be further from the truth. Instead, Mr. Pettis explains how China manipulates other countries’ laissez-faire policies to undermine free trade and the efficient allocation of resources around the globe.

Why this matters

Michael Pettis’s thesis plays an important role in my framework for thinking about China’s impact on the world and, thus, the responses brewing to it in the US, Europe and elsewhere. Hence, it’s worth describing his ideas, the criticisms of them, why those are wrong, and where I diverge from Mr. Pettis. Unfortunately, because his thesis is based on two economic identities, I am going to have to define some terms and take you through some simple arithmetic to explain them. This piece also is a little longer than my usual Seriously, Marvin?! articles. I apologize in advance.

Boring national income accounting

An identity is a mathematical equation that is true by definition. Most of macroeconomics relates at some level to two identities that define what national income, or gross domestic product (GDP), is. Why two identities? Because you can define GDP in terms of where income comes from or where it goes.

Think first of how income is generated: someone must produce and sell something. The “expenditure approach” to measuring national income defines it as the sum of all sources of spending in an economy, since that expenditure ultimately accrues as household income either through wages paid to workers or profits paid to proprietors and shareholders. Hence, we can measure GDP as follows:

(1) Y = C + I + G + (X – M)

(Y) GDP = (C) household consumption

+ (I) investment in factories or houses

+ (G) government purchases

+ (X – M) exports – imports (or, net exports)

Note that imports, which are the products of another country, are subtracted from domestic expenditure because they don’t generate domestic income. This equation should be very familiar to anyone who has taken even an introductory course in economics. But you can also think about how households use their income (somewhat confusingly called the “income approach”):

(2) Y = C + S_h + T

(Y) GDP = (C) household consumption

+ (S_h) household savings

+ (T) taxes paid to government

I.e. income is used to consume, save or pay taxes. Here’s where we do a little math. Since both identities define national income, GDP, we can set them equal to each other and, with a bit of algebra, derive a new identity that defines international trade:11

(3) (X – M) = S_h + S_g – I, where S_g = (T – G), or government savings, the excess of tax receipts over government spending (usually negative)

or, since household (S_h) plus government savings (S_g) equals national savings

(X – M) = S – I

If you stop to think about it, this equation is surprisingly intuitive: if a country doesn’t produce enough construction materials and machines to build the factories or houses it wants – i.e. it wants to invest more than it can produce or save – it must import those materials.

But how does a net importer pay for imports beyond its exports (which provide necessary foreign currency)? It must “borrow” the money from a net exporter. That borrowing could be short-term trade finance loans, or it could be more permanent, i.e. the net exporter could buy assets from the importer, like the importer’s government bonds or shares in its companies. This provides the savings the net importer lacks to fulfill its desired investment. This leads to one more identity that will be useful. Just as we approached GDP from both the “expenditure” and “income” sides, we can do the same with the international trade identity in equation (3) with an identity defining how net exports are paid for:

(4) (X – M) net exports = (–KA) private financial asset purchases

+ (dR) change in FX reserves

That is, a net exporter can finance importers’ purchases of its net exports by buying assets from the importers, either by private companies and citizens, or as official foreign exchange intervention.

We are now armed with the mathematical identities to explain Mr. Pettis’s thesis. But there are two important points to remember about these identities. First, they are not theories, they are true by definition. Second, they must hold across all countries. Unless we start trading with Mars, one country’s net exports are someone else’s net imports.

Mr. Pettis’s simple idea

Mr. Pettis makes two remarkably simple but easily missed points based on these identities. First, if a country can control both its domestic savings and investment, by definition it can wholly determine its net exports since the difference in the former equals the latter. Second, if a country can control its net exports, it forces other countries’savings and investment to adjust to accommodate it because trade must sum to zero globally.

These insights form a powerful idea: if – and this is the big question, if – a country can manipulate its domestic savings and investment through industrial policies, then assuming other countries do nothing to counter it, i.e. pursue laissez-faire policies, the manipulating country can force adjustment of the rest of the world’s savings and investment. If the country in question is relatively small, it probably doesn’t have a large macro effect (though it might in specific industries where industrial policies are concentrated). But if it is a large country, like China, it can create major distortions in the global economy.

Manipulating savings and investment

As noted, Mr. Pettis’s insight hinges on a big, controversial “if.” How can a country, particularly a large one, control both savings and investment across millions of households and companies? Mr. Pettis identifies several ways in which Chinese policy intentionally suppresses consumption to boost national savings and directs both the level and allocation of fixed-asset investment within the country.

- Wage repression: The household income share of GDP in China is remarkably low relative to other countries, in part due to wage suppression. Workers in China require local residency permits (the hukou system) that creates two tiers of wages: higher wages for local workers with valid work permits and lower wages for migrant workers from poorer provinces lacking local permits. By managing the flow of hukou – issuing permits and cracking down on migrant employment – Chinese provincial governments can suppress both tiers of wages by increasing the effective labor supply.

- Financial repression: China’s financial system is closed by capital controls and highly regulated, reducing the investment opportunities of households and encouraging higher savings rates. Bank interest rates on deposits are regulated and held at artificially low levels to enable banks to direct lending to favored industries at below-market rates. Few other domestic savings opportunities exist: real estate (hence the now collapsing property bubble), domestic stocks, and unregulated “wealth management” products that are another form of directed bank lending. Foreign investment is constrained by capital controls.

- Land seizure and reallocation: Local governments force rural owners to sell land to the government at low, state-determined prices, repressing rural households’ wealth. The acquired land is then used by local governments either to generate government revenue via land sales (at marked-up prices) to property developers, or to stimulate investment in targeted industries through land grants or below-market price sales to state-owned enterprises (SOEs).

- Exchange rate undervaluation: Throughout its most rapid phase of development, China intervened heavily in currency markets to prevent the renminbi from appreciating. Brad Setser at the Council on Foreign Relations documents continued stealth interventions via state-owned banks that have accelerated recently.22 Comprehensive capital controls allow China to decouple its domestic monetary policy from its exchange rate interventions, preventing the liquidity they create from driving inflation. Without inflation raising both the domestic and international price of Chinese goods, FX intervention depresses the real value of the renminbi. This raises the cost of imports for consumers, suppressing consumption, and encouraging domestic investment in import substitutes.

- Retained earnings of firms: The state-owned enterprises that dominate China’s economy, particularly in fixed asset investment and in strategically important industries, reinvest earnings at unusually high rates relative to other “private” Chinese companies, which reinvest earnings at unusually high rates relative to non-Chinese companies. This increases both national savings and investment and simultaneously denies households dividend income.

Criticality of capital controls

The critical ingredient is China’s comprehensive capital controls. Without the ability to trap households’ savings within China, the power to regulate interest and dividends paid to households, to direct savings from banks, or to dictate land distribution would be useless. But by creating a closed system, capital controls mean that Chinese policymakers largely can determine domestic savings and investment. It’s also important to remember that all firms in China, not just SOEs, are instruments of state policy: by law, every large company in China, public or private, must have an active Communist Party cadre that aligns its activities with state policies and priorities.33 Further, China augments its state-directed lending and investment with a massive subsidy program that the Center for Strategic and International Studies estimates at almost 2 percentage points of GDP per year.44

The manipulation that matters

While China’s currency manipulation is a major focus of the US Treasury – and supposedly the IMF if it did its job – Mr. Pettis’s framework makes clear it plays a small role in the overall strategy. Yes, relative prices matter for trade (and suppression of Chinese households’ consumption) but the ability to manage national savings and investment in the international trade identity, equation (3), forces both domestic and foreign prices to adjust. That’s the real manipulation. Indeed, if one combines the international trade and finance identities above it becomes clear that the biggest effect of FX intervention is to “macromanage” savings and investment, which, even with China’s capital controls, are difficult to micromanage from the bottom up:

(5) (–KA) private financial flows + (dR) FX intervention =

(S) national savings – (I) investment

By adjusting dR on the left side – or as Mr. Setser points out, increasingly –KAthrough state-owned banks’ foreign asset purchases – Chinese policymakers can fine tune net savings flows on the right side, and thus net exports.

Critique#1: Identities aren’t causal

The first major criticism of Mr. Pettis’s framework is that mathematical identities aren’t causal. This is true in a textbook or in trade between countries pursuing laissez-faire policies. Under those conditions, if a government restricted interest paid by banks or forced banks to lend to unproductive enterprises, savers would send their money abroad and banks would go bankrupt. But in China, capital controls trap domestic savings inside the country, leaving households with no other choice, and bad loans are segregated from banks’ balance sheets into government-funded “bad” asset managers that absorb the losses as fiscal expenditure.

Quite ironically, some of the same economists leveling this criticism at Mr. Pettis insist, because government savings is part of national savings, that equation (3) implies the US current account deficit is “caused” by the US fiscal deficit. Yet in an open economy, where domestic savings and investment are free to adjust in response to government dissaving, the fiscal deficit can and often does move differently to the trade balance because identities are notcausal in an open economy. China, however, is a closed economy, so policy does have the power to manipulate identities for causal effect.

Critique #2: China’s production is more efficient

The more common criticism of Mr. Pettis’s thesis is that China dominates manufacturing not due to industrial policies but because its manufacturers are “more efficient.” By “efficient,” those making the claim generally mean that Chinese carmakers like BYD sell sophisticated, market-leading cars at prices well below those of inferior German, Japanese or US cars. But that’s not evidence of efficiency if the cars are being sold at a loss. Even before it became front-page news that BYD and every other Chinese auto maker is struggling to pay their suppliers, it’s been clear for decades from earnings reports and the performance of Chinese stocks that Chinese companies fail to generate profits.55

China’s poor efficiency is even apparent in the aggregate data. As I discussed in Ain’t misapplyin’, China’s total factor productivity growth – i.e. its value added above its cost of labor and capital – has been negative for over a decade. Put another way, all the capital lavished on BYD by Chinese banks would have had a higher return in Germany, Japan, the US, or nearly anywhere else. It’s easy to make “cheap” sophisticated products if you have access to free, unlimited capital, but that’s not the same as efficient. That’s the point of Mr. Pettis’s thesis: by suppressing consumption to boost savings and then direct it to targeted industries, China has engineered its economy to create underpriced capital that allows its manufacturers to produce below the marginal costs of international competitors.

You got a lot of explaining to do, Mr. Critic!

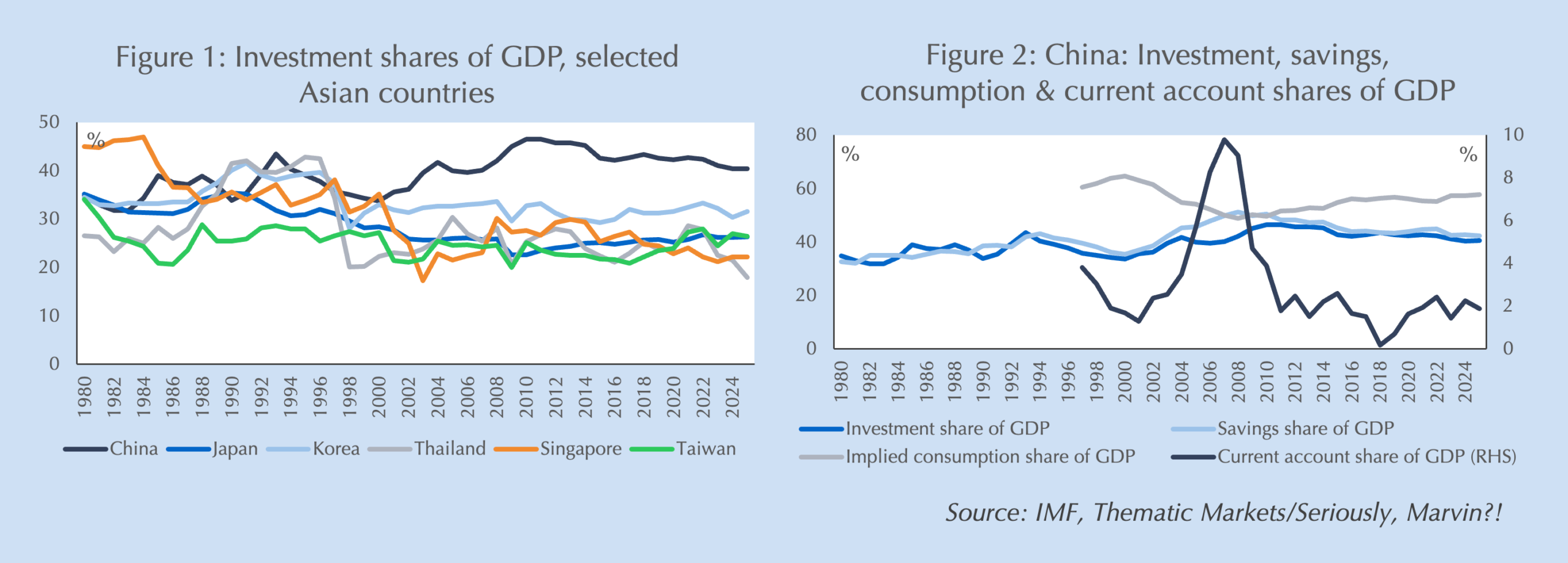

If Mr. Pettis’s theory is wrong, his critics have a lot of big mysteries to explain. For starters, how has China, for over 30 years, sustained an investment share of GDP that no other country could maintain for more than a decade, and even then, usually ended in an economic crisis (e.g. Japan, Thailand, Korea; see Figure 1)? Why, over the same period and contrary to all economic theory, did China export a significant share of its savings each year to richer countries, peaking at 10% of national income during China’s fastest phase of development (Figure 2)? How did it maintain interest rates that were below almost any other emerging economy and even most advanced economies while it was investing at such high rates and still exporting a significant portion of national savings? And why did its stock market underperform over that period if it was such a productive place to invest?

The questions themselves make clear that China’s economy is not now and never has been a market economy. They also are nearly impossible to answer without making use of Mr. Pettis’s insights. China can maintain unprofitable rates of investment that would bankrupt any other nation because it represses its citizens’ consumption to create the savings needed to fund cheap, targeted bank loans to manufacturers and to pay for fiscal authorities to wipe away the losses that accrue from inevitable overinvestment. China’s size and ability to do this has a major impact on resource allocation in the rest of the world, effects that are now generating unprecedented shifts in economic policy elsewhere in response. This is why I regularly cite Mr. Pettis in my analyses of how China’s policy affects the rest of the world (see for instance, Incompatible drag).

Where I differ: motives

Mr. Pettis and I both agree that China’s overinvestment is intentional, not accidental, and on the mechanism used to achieve it. But we differ on the motivation for it. Perhaps because Mr. Pettis lives in China, where he is a professor of Finance at Peking University, he ascribes more benign motives for China’s distortion of global resource allocation. In his view, the original motive was – following Germany’s, Japan’s and Korea’s lead – accelerating development. But once the system became entrenched, it was hard for the special interests that benefitted from them, namely SOEs and the Chinese Communist Party members who run them, to give the system up.

While I accept that entrenched interests play a role, I think the evidence points to national security policy being both the original and continuing reason for China’s economic policies. Both the industries targeted – all critical industries for military development – and the broader effects of intentional overcapacity fit too nicely within the framework of Unrestricted Warfare, a book written in 1997 by two (then) People’s Liberation Army senior colonels on how to counter America’s superior technological and military might.66 Intentional overcapacity serves multiple purposes: it undermines strategic competitors’ industrial capacity, it creates monopoly powers that can be used offensively (e.g. refined rare earth), and it offers rapid technological progress by running many concurrent (costly and mostly failed) experiments. The last may not be economically efficient, but it is time efficient for a country that was in a hurry to catch up with the West.

Whether Michael Pettis is right about the motives of Chinese policymakers or I am doesn’t change the macroeconomic effects. They are real and are shaping the global economy. Denying the Pettis model leads both to bad policy responses and misinformed judgements on markets. But understanding the motivation, or how that motive is perceived in, for instance, Washington, makes a big difference in other country’s policy responses.

Comments are available to paid subscribers only.