Note: This free article is based on my keynote speech to the 2023 Taiwan Big Future International Summit hosted by Business Today (Taiwan). It presents my analysis of the challenge Taiwan, one of globalization’s champions, faces in the new global political economy dominated by four major Themes familiar to Thematic Markets’ subscribers: Localization, Being is believing, Global entropy, and Uncertainty. You can watch the speech here.

A tiger in a typhoon

Taiwan was one of the four original “Asian Tigers”, the earliest adopters of the globalization enabled by the post-War paradigm of American peace, ascendant neoliberalism, and rapid technological progress. By facilitating the transfer of both capital and know how to less-developed economies, globalization led to the most rapid economic development and convergence in history. As first movers, the Asian Tigers benefitted most, climbing the skills and income ladder to join the world’s richest, most technologically advanced economies. Taiwan, to some extent, has even bettered its Tiger peers, Hong Kong, Singapore and South Korea, by specializing in the design and production of many of the world’s most sophisticated semiconductors, which are now indispensable inputs into the modern global economy.

But the peace, stability and neoliberal economics that allowed both globalization and Taiwan to flourish has rapidly disintegrated amid increasing challenges to US hegemony and relentless advances in technology. Taiwan must now adapt to a radically different economic environment, and must do so as an intensifying Great Powers tempest swirls around it. Metaphorically, to continue to prosper, the Tiger must change its stripes amid a typhoon.

Four Themes redefining the world

At Thematic Markets, my focus is on framework: a consistent, logical structure based on fundamental economic theory and evidence. Themes – the multi-year, sometimes multi-decade trends in economics, politics, technology, and behaviors – are essential building blocks within that framework. These Themes drive the global political economy, sometimes unnoticed and sometimes in the foreground. Often, however, these Themes are misidentified or misdiagnosed, leading to poor analyses and inaccurate forecasts.

I see four major global Themes redefining the global political economy: Localization, Being is believing, Global entropy, and Uncertainty. Despite their critical importance to reshaping the world and driving most major markets, the consensus has either missed them completely or misdiagnosed them, which explains why they have so badly forecast inflation, interest rates, economic growth, and trade in recent years. I will start by defining and explaining the effects of these four Themes, then analyze their effects on Taiwan, and finally close with suggestions for how Taiwan can adapt to this newly “punctuated equilibrium”.

Localization

The first, and perhaps most important of the Themes that I will discuss today, automated Localization, well illustrates the potential for misdiagnosis to cloud one’s analysis. Most of you likely already are familiar with this Theme under its more popular name, “de-globalization”, which usually is described in negative, welfare-reducing terms and is blamed on populism or regressive geopolitics. Yet, I will argue that Localization – the force driving what others call de-globalization – is primarily driven by technology, not politics or national rivalries, though these may now be accelerating it. Furthermore, Localization is welfare and income enhancing, not detracting. It also is wholly different from anything humans have experienced in 300,000 years. But, like globalization, it produces winners and losers, and like any competitive process, participants must continuously adapt to survive.

Excavations at Olorgesailie Basin, Kenya. Credit: Smithsonian

Recent evidence from the Olorgesailie Basin in Kenya (pictured) suggests that humans and their forebearers have been engaged in trade for at least 300,000 years. While its trend has been interrupted by war and civilizations’ rise and fall, human history has generally been defined by increasing levels of trade ever since. English economists Adam Smith and David Ricardo explained why two centuries ago: resources and skills are unevenly distributedand the principal of comparative advantage implies that, through cooperative trade, we can all be better off by specializing in work.

But what happens when robots or artificial intelligence, which can be located anywhere, begin to eclipse even the most skilled craftsmen in an increasing array of tasks? While trade in commodities – oil from the Middle East, cobalt from central Africa – remains necessary, globally dispersed manufacturing supply chains no longer make sense if the same specialized tasks can all be completed more efficiently by robots close to your customers.

Indeed, automated localized production has distinct advantages over dispersed global supply chains that go well beyond cost or more recent concerns over security. First, Localization better enables onsite, on-demand customization to meet buyers needs. It also allows for more rapid evolution of manufacturing processes to cut costs and meet ever-shorter design and investment cycles in a competitive business environment.

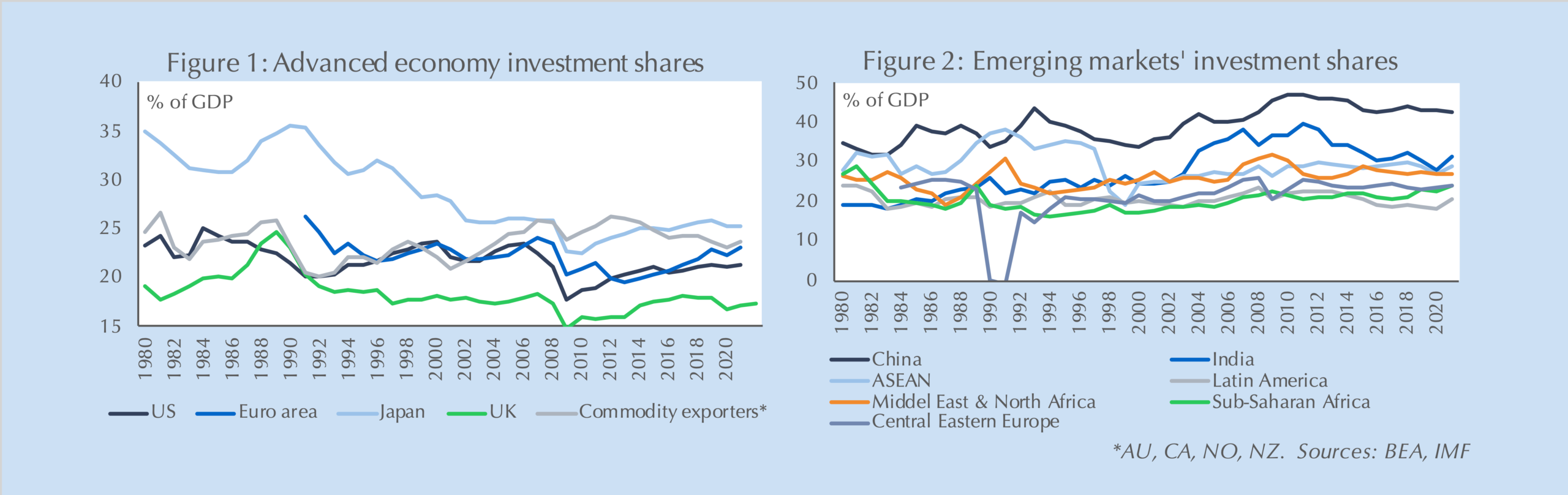

This is not my vision for the future newly enabled by ChatGPT, nor is it even a recent shift in global production since Covid. The change began over a decade ago and by 2012 hit a tipping point. In the prior 40 years for which we have reliable data, the investment share of GDP fell continuously in advanced economies (Figure 1), while it rose in emerging markets (Figure 2). This reflected the age of “hyperglobalization” where rich countries outsourced supply chains to cheaper, developing economies. But in 2012 – roughly the same year that ratio of global trade to income peaked – those trends reversed. 300,000 years of increasing trade came to an end.

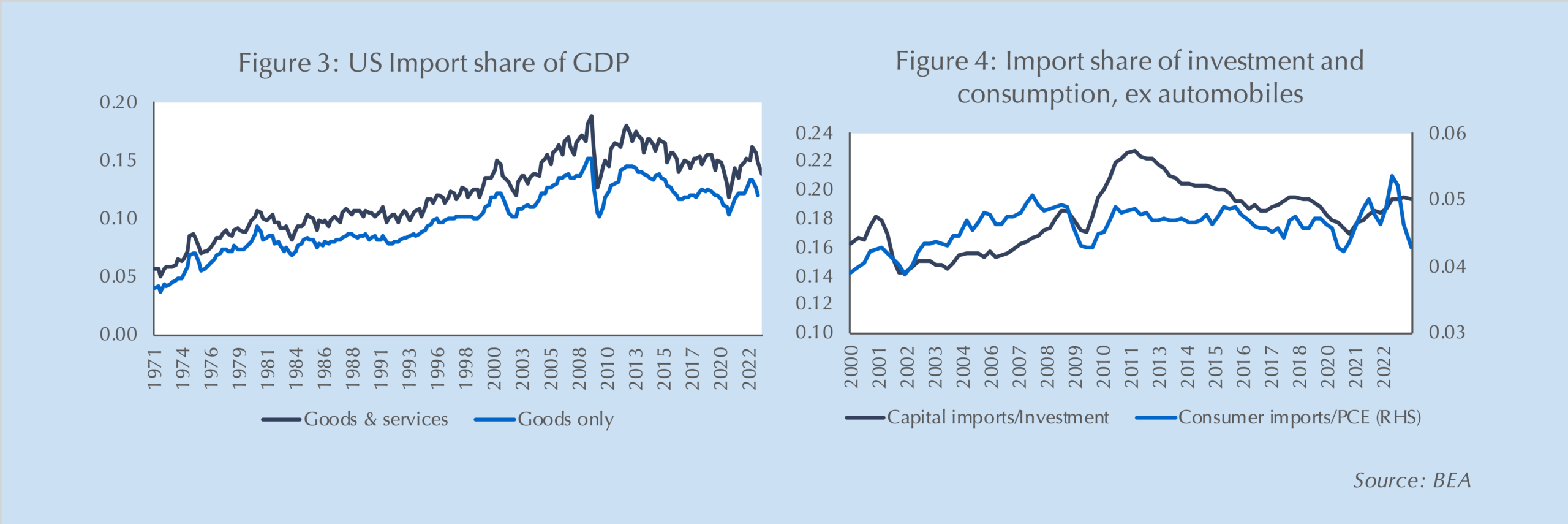

It wasn’t just a shift in capex. Import penetration in the US peaked as a share of both consumption and investment at roughly the same time (Figures 3 and 4). While consumer imports have rebounded somewhat since Covid as US demand outstripped supply, the breakpoint and reversal in trend is clear across trade and investment data. You can also see it in asset prices. Emerging markets’ exchange rates and stock prices all peaked relative to advanced economies at roughly the same time.

Further, at a microlevel you can see the Localization of production around you. Today, you can walk into some flagship Nike and Adidas stores and have shoes custom designed and made made for you, in house, while you wait. Or, look at Tesla’s state-of-the-art “Gigafactory” in Austin, Texas where every aspect of car production is integrated in a single, rapidly adaptable, automated factory.

Properly understood as a technological phenomenon, Localization is driven by efficiency, just as globalization was. And, just as globalization’s efficiency gains were a net positive for global income, so is Localization. But, like globalization, Localization’s gains are not evenly dispersed.

While globalization disproportionately benefitted developing economies’ growth at the expense of advanced economies, the reverse now is taking place. Rich consumers not only offer higher returns to Localization, but the more educated workforces of advanced economies also better facilitateautomation. This helps explain the outperformance of rich economies’ — and especially American — asset prices since 2012.

But it also illustrates the immense challenge poorer countries now face as globalization shifts to Localization: how will poor economies keep pace with richer ones without the transfer of capital and technology that globalization enabled? If emerging markets, especially those lower on the development ladder, do not solve this problem, they are at risk of falling permanently behind, as they did when the West first industrialized.

More immediately, a proper understanding of Localization helps to explain why most analysts have gotten the global economy so wrong in recent years. Too many had bought into the false narratives of “secular stagnation”, politics as driving “de-globalization” and supply shocks as the source of recent inflation. As a result, they largely missed unexpectedly strong economic growth amid rising inflation and interest rates that all resulted from the interaction of Localization with Covid.

As noted, Localization began well before Brexit, Donald Trump’s presidency and Covid. But all of these, especially the last, accelerated Localization. When businesses that were already considering the potential efficiency gains of automated Localization were confronted by severe, even enterprise-threatening disruptions in their dispersed supply chains as Covid shut down international trade, the decision to localize was obvious and immediate. A massive capex boom to build new, automated, local production capacity ensued.

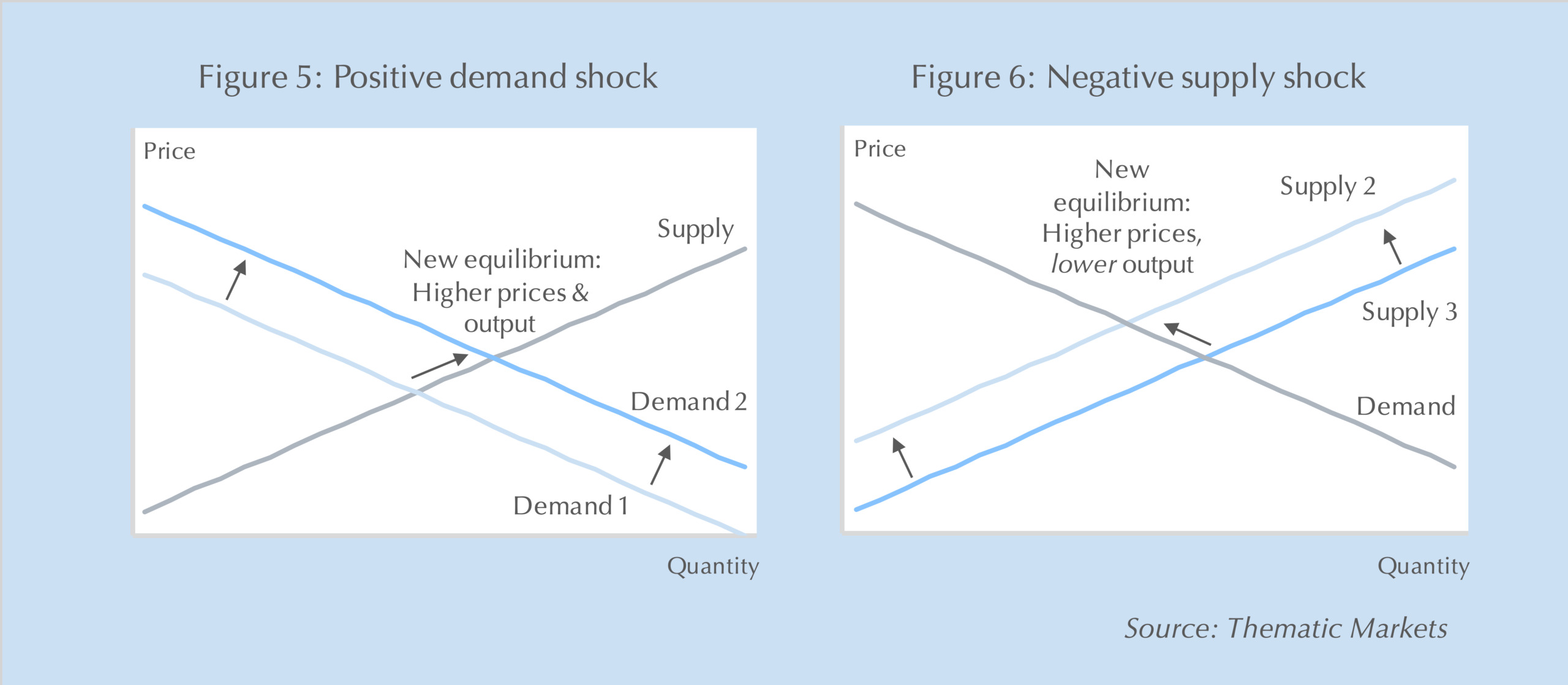

In the US and other rich economies, businesses are now rushing to replace 40-plus years of investment in outsourced supply chains with local production capacity, resulting in surging economic and employment growth, and rising cost pressures and real interest rates as demand outruns supply. Basic economic analysis points to a demand shock as the clear cause. Let’s review your Econ 101 class. If output, prices and interest rates rise – as they have – the only possible cause is a positive demand shock (Figure 5). In a supply shock, output and interest rates would fall when prices rose (Figure 6).

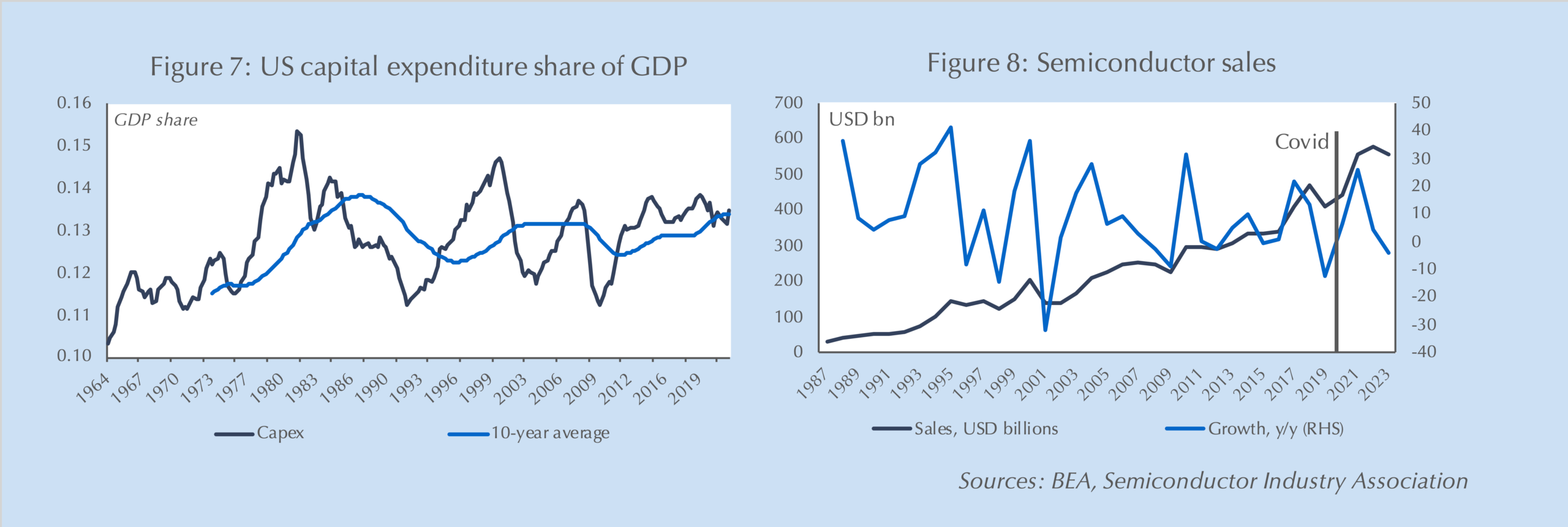

Now let’s look at the evidence. Even after an unheralded decade-long boom, US capex expenditure accelerated markedly after Covid. It even increased as a share of GDP despite the surge in government spending and “catch-up” consumption after lockdown (Figure 7). (How many times recently have you seen perplexed and astounded analysts circulating the chart of US business structures construction going hyperbolic?)

Remember the great semiconductor shortage? Despite being blamed for shortages of everything from computers to autos, semiconductor production never actually fell during or after Covid (Figure 8). Global chip sales rose by 7% in 2020 – despite the sharpest economic contraction in recorded history – and rose by a further 26% in 2021. Supply was not a problem, meeting surging demand for Localization-driven capex was.

And let’s not forget the most compelling evidence: both economic output and inflation have consistently bettered analysts’ expectations despite much higher real interest rates than any of them (or markets) had forecast.

As demand outstripped supply, it predictably led to surge in cost pressures that precipitated a sharp rise in inflation. But unlike prior cost shocks that quicky faded into the persistent disinflation that vexed most advanced economy central banks for the last two decades, this time inflation jumped much higher and has been far stickier.

To explain why, I need to introduce the next Theme crucial to understanding the current global political economy: Being is believing.

Being is believing

While most theoretical models of inflation include expectations, economists tend to leave them out of their empirical models for two reasons: First, few countries have consistent or reliable measures of inflation expectations. Second, like all beliefs, expectations are unpredictable. But just because it’shard to fit in your model doesn’t mean you can ignore it!

The same property of beliefs that makes them difficult to model also makes them impossible to ignore: beliefs can be self-fulfilling. That is, something can become real or true simply because it is believed.

Think about how inflation expectations affect the interaction of consumers and producers. Consider first a world – like that which existed in most advanced economies over much of the past two decades – where everyone expects inflation to be flat or even falling (Table 1, columns 2 and 3). If a producer with a profit margin gets hit by a cost shock he has two choices: raise prices to pass it on to consumers, or to absorb the cost within his margin. If consumers expect flat or falling prices, they will view a hike as price gauging and switch brands. While the producer may avoid a drop in his current margin, he likely loses future profits from the lost customers. Hence, the producer chooses to absorb the cost shock.

But notice how behaviour changes when consumers and producers expect higher prices (Table 1, columns 4 and 5). In this case, the producer has an incentive to take a chance and pass cost hikes on to his customers. The consumers, unsure if this is price gauging or expected inflation, may not switch brands. As a result, the producer preserves not only his current margin but its long-term profitability. Thus, expectations for rising inflation become self-fulfilling: Being is believing.

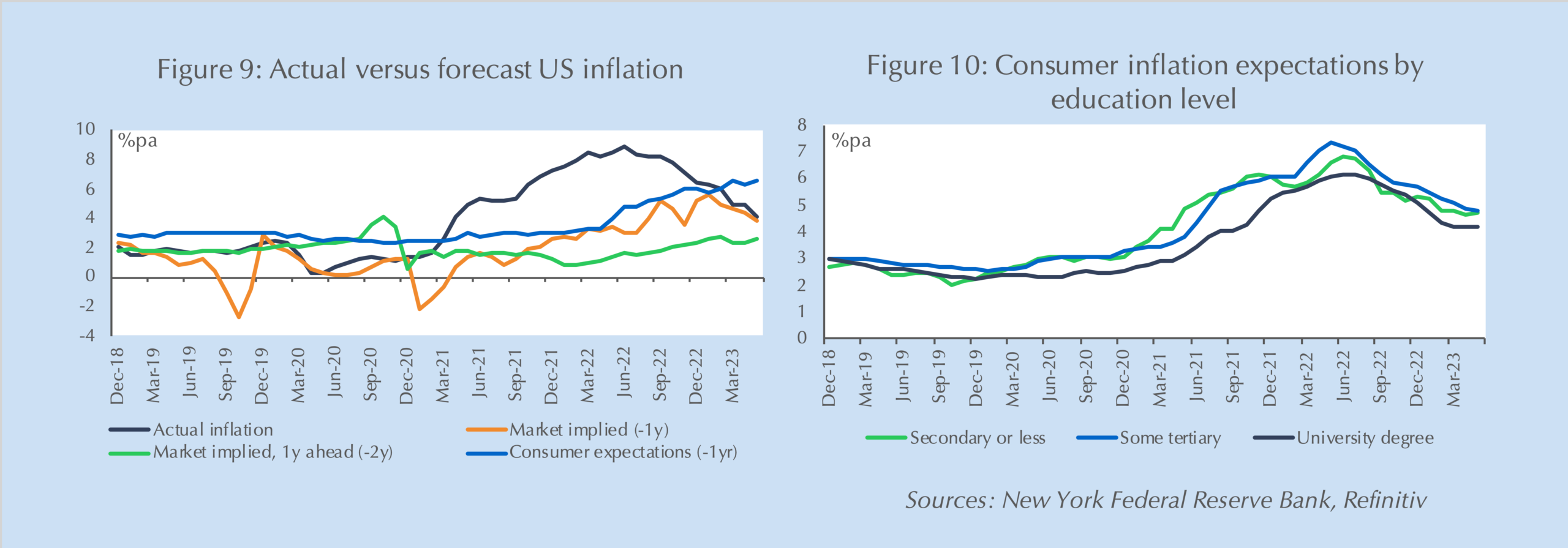

There are two stunning pieces of evidence that beliefs are creating inflation. First consider the predictive power of consumer expectations versus professional forecasters since Covid. Unlike most countries, the US has several survey measures of consumer inflation expectations that we can compare with inflation forecasts by professional economists, the Federal Reserve, and those implied from markets by inflation-indexed bonds (Figure 9). Since Covid hit, the mean-square forecast error of consumer expectations was smaller than that of markets, professional economists and the Fed. More astounding, if we break down US consumer expectations by education (Figure 10), those with a secondary education (or less) did better than those with some university, who did better than those with university degrees!

How can this surprising inversion of expertise be possible? That less-educated consumers are better forecasters than the educated, who are themselves better than experts and policymakers? The answer is simple: the less educated are not forecasting inflation, they are creating it by believing in it! Being is believing in action.

Corporate profits also provide evidence for this unexpected result. Despite double digit increases in input costs, PepsiCo reported not only higher profits in 2022 but even increased gross margins! Pepsi was not alone; many other companies reported similar margin expansion even as input costs rose. While politicians and the press decry this phenomenon as “Greedflation” – as though these companies somehow spontaneously discovered pricing power last year – it was only possible because consumers expected higher inflation and accepted price hikes without switching brands, for instance to Coca-Cola.

Why did inflation expectations shift? Since the Global Financial Crisis, persistent disinflation pushed central banks into a decade-long experiment in unconventional monetary policy. As Covid hit, many central banks, including the Federal Reserve, took a new step by committing to target average inflation rather than current inflation, meaning that they would try make up any shortfall in inflation by allowing an overshoot later.

These commitments came just as Covid led to the massive demand surge – and cost push – that I described before. The combination, augmented by unprecedented peacetime fiscal largess, appears to have dislodged expectations for falling inflation and embedded expectations for persistently higher inflation.

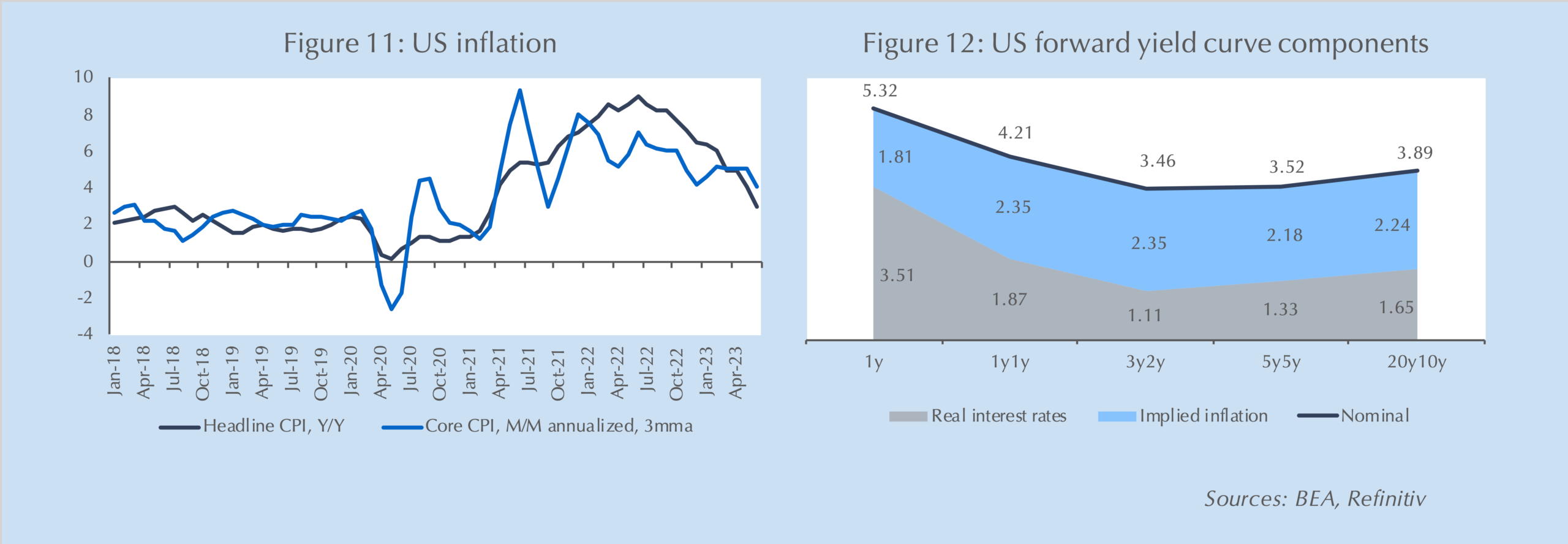

Both central banks and markets may face a rude awakening next year – again! – judging by the survey measures of consumer inflation expectations that I just referenced. Although they have retreated from their peak values, they have begun to stabilize well above pre-Covid levels. This, and the stubborn persistence of core inflation suggests that higher inflation expectations have become embedded and will be difficult to dislodge (Figure 11).

Inflation swap and interest rate markets price in a rapid return to target inflation and a sharp fall in policy rates next year (Figure 12). If Being is believing effects really are the now primary driver of inflation, as I believe, a sharp repricing of interest rates and thus other assets is likely before yearend. That likely implies another surge in the US dollar as the Federal Reserve, despite its late start, has shown itself second to none in its commitment to return inflation to target.

Higher interest rates and stronger US dollar will further strain the world’s debtors, especially those that are having difficulty adjusting to the new economic paradigm of Localization. Macro-credit events remain one of the most likely sources of volatility in our immediate future as debtors adjust to this new reality. I covered these risks in detail in Debt reality versus perceptions, but here I would like to connect them to Being is believing effects and one low-probability, high-impact regional risk important to Taiwan.

Credit events, just like bank runs, are belief-driven: if creditors believe a debtor is solvent, even if it is not, they will continue to lend to it. But if belief in the debtor’s solvency evaporates, so too does its access to credit and liquidity, even if it is solvent! Beliefs drive reality: Being is believing again.

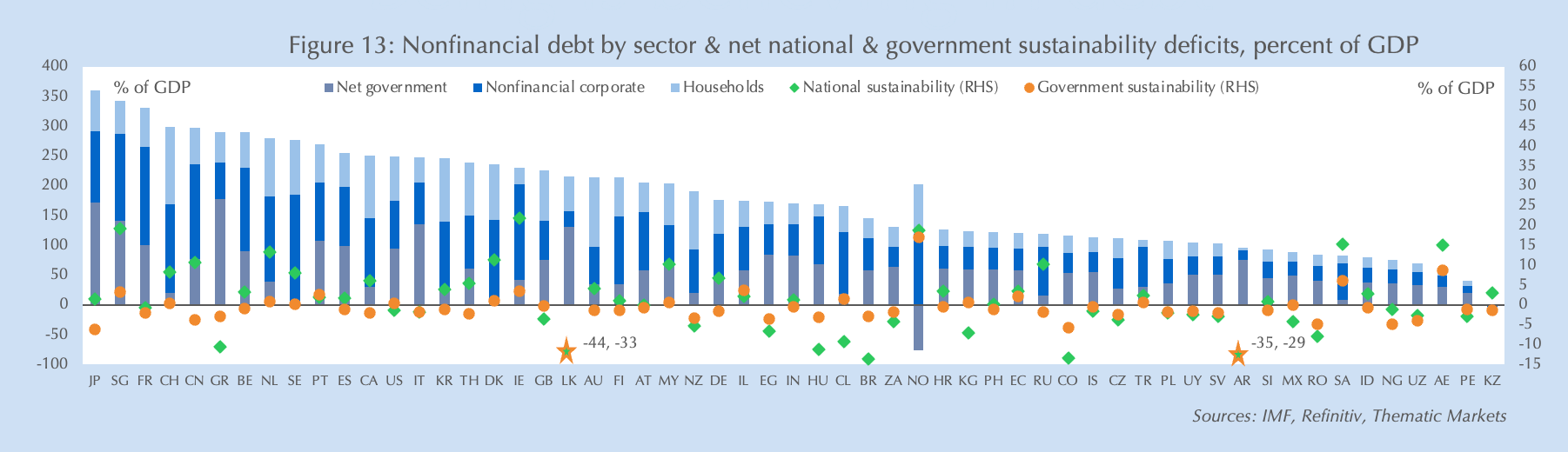

Relative to income, the world’s largest gross debtor is Japan (Figure 13). Fortunately, Japan funds its own debt and is, indeed, a net creditor to the rest of the world. But given the immensity of Japan’s debt and its anaemic potential growth rate, its solvency depends on extraordinarily low real interest rates. Japan’s aberrantly low interest rates – in a world where interest rates have leapt higher nearly everywhere else – are possible only because Japanese citizens believe in the solvency of their own government.

Put another way, Japan is solvent because its citizens believe it is solvent. Therein lies the problem. Rising global interest rates and a strong US dollar are going to test that belief and even a small erosion Japanese savers’ faith could precipitate a cascade of domestic capital flight that would bring about mayhem in the world’s third-largest debt market with serious implications for global and regional financial markets. I will return to this risk as it relates to Taiwan later.

Global entropy

The next Theme I’d like to discuss is Global entropy. Entropy is a concept from physics that everything, given enough time, tends toward disorder. The post-World War II “rules-based order” established by American hegemony is no exception. New challengers always arise to tear down the previousorder and the world descends into chaos. Global entropy is now well underway, driven by deep cultural differences, technology and entropy’s most powerful weapon, time.

In the 1990s two rival views of the world’s political future emerged: Francis Fukuyama’s “End of History” and Samuel Huntington’s “Clash of Civilizations”. Fukuyama argued that liberal, capitalist democracy had proven itself unbeatable and was on an irreversible march to total victory. Huntington instead saw democratic liberalism as a Western European cultural creation whose roots were not well suited to grow in other cultures. Huntington predicted instead that long-standing cultural differences would create conflict as globalization brought them into closer contact and non-Western cultures evolved political economies to better compete with liberal capital democracy’s economic and military dominance.

The last three decades since have been characterized by sustained conflict between the West and parts of Islam, a resurgent Russia challenging the West in the Middle East and Ukraine, and China increasingly asserting its role as the “Middle Kingdom” of Asia and global strategic rival to the US. Democracy instead has retreated. It seems clear that Huntington was right and Fukuyama suffered from American cultural arrogance. Cultural differences are deep and reflect differing values, including those related to political discourse and governance.

But cultural rivalry alone is not sufficient to undermine US hegemony. America’s rivals needed to evolve, both politically and technologically, and have. Politically, the development of state capitalism – individual economic freedom, incentivised to achieve state objectives determined by an oligopolistic elite – allowed China, one of the world’s poorest countries when Fukuyama wrote his thesis, to build unprecedented industrial might and technological know-how to rival the world’s hegemon within 30 years. Russia used state capitalism to reinvent itself as a producer and broker of commodities and sophisticated armaments.

Technologically, American rivals co-opted Western technology as a steppingstone and strategic weapon. For instance, through industrial policy China now dominates manufacturing of Western technology products. Or for a more sinister example, in the war in Syria, ISIS, a non-state actor, created sophisticated artillery targeting systems that previously only nation-states had access to using nothing more than iPads and Google Earth. More importantly, the rivals are now becoming technology leaders y coupling state capitalism with fundamental research as China is in some areas of artificial intelligence or robotics, or in military technologies like ballistic and hyper sonic missiles, or cyber weapons, where both Russia and China excel.

Perhaps most importantly, as detailed by my colleague David Kilcullen in The Dragons and the Snakes, America’s rivals patiently observed US weaknesses in war and peace, learning how to undermine and defeat it. China joined the WTO without opening either its capital account or key sectors in finance and technology, the equivalent of entering the Tour de France with an electric bike. At the UN, China and Russia have effectively wielded their vetoes and capitalized on Western stumbles – like Iraq – to build alliances, and block US initiatives. China even copied the US Marshall plan with its One Belt, One Road initiative in economic diplomacy. Militarily, China’s modernization of its military and heavy investment in Anti-Access/Area Denial weapons, infrastructure and even man-made islands has effectively made the Western Pacific a potential no-go area for the US Navy.

With the US now no longer an unrivalled hegemony, Global entropy has taken hold. I do not need to belabor the immediate implications for Taiwan, which sits on the literal frontline of the worsening tension between China and the US. But it also sits on the figurative frontline of global economic bifurcation resulting from Global entropy. Western nations’ rejection of Huawei’s 5G network was one of the first visible signs of it, but now we see the same in China and Russia’s efforts to develop parallel payment systems, in US efforts to restrict both countries’ access to undersea cables, and perhaps more important to Taiwan, increasing nationalism around advanced semiconductor manufacturing.

Of these examples, none would naturally occur even within the paradigm of automated Localization that I described before. The economies of scale or network benefits are too great. But national security concerns increasingly trump economic efficiency.

Uncertainty

I will now turn to the final and most abstract Theme of my talk, which intertwines and connects the other three: Uncertainty. Properly understood, Uncertainty is a mathematical concept rather than a Theme, but its importance to the global political economy, or at least our perceptionsof it, changes through time. Localization, Being is believing, Global entropy, social change, and the rapid technological change that contributes to each, all have sharply increased Uncertainty, and it is that rise to which I am refer as a Theme.

By Uncertainty, I mean non-quantifiable risk. John Maynard Keynes, in my view, best delineated risks and in doing so defined Uncertainty. Keynes described three types of risk: objective, subjective and uncertain. Objective risks are those with probabilities we know and can precisely define; for instance, the likelihood of drawing three aces from a deck of 52 cards. Subjective risks are those that can be quantified, but only with judgement or guess work because, in the language of Mathematics, we cannot precisely define the probability measure. For example, we know that the probability of a typhoon hitting Taipei next month is higher than in, say, January, but unlike an objective risk, we can’t precisely state its probability.

Uncertainty is the most dangerous type of risk because it cannot be quantified. The late US Defense Secretary, Donald Rumsfeld, called these “unknown unknowns”. Uncertain risks are those that we know only through conjecture or that occur so infrequently that we cannot even guess at their probabilities. Indeed, we may not even know the risk exists. For instance, how many of you could even conceive in January 2020 that lockdown of 7 billion people was possible? And yet it happened. (See Wagner’s lessonsregarding our ability to perceive changes in uncertainty and profit from them.)

After five decades of unprecedented stability and (at least seeming) predictability, we now live in a world awash with Uncertainty: a multitude of risks that are impossible to quantify. Will Localization lead to permanent divergence of the world’s rich and poor economies? Will Japanese residents lose faith in their own currency? Will China try to take Taiwan by force? Will ChatGPT put everyone out of work? Will its cousin Skynet terminate us? None of these questions are knowable, nor are their probabilities quantifiable. Yet each has potentially enormous effects on us personally, politically and financially.

Think for a moment about the financial implications. Asset managers are increasingly using quantitative methods to allocate capital and invest. Yet the risks to which these investments are exposed are increasingly non-quantifiable. Can their portfolio choices be even close to optimal as a result? Highly unlikely.

Implications for Taiwan

Let me now close by turning to how these four Themes affect Taiwan and offer some proposals for how this vibrant democracy may attempt to address them.

Taiwan is fortunate that, as one of the original Tigers, it was able to climb globalization’s skills and capital ladder before Localization removed it. Today it is a rich, dynamic economy that is a world leader in design and production of the most sophisticated microchips with a skilled workforce that easily facilitates participation in Localization. But Taiwan faces two serious demand problems, one internal and one external.

Taiwan’s internal demand problem is its continued reliance on the East Asian Tiger model of growth originated by Japan: suppressing domestic consumption in pursuit of capital accumulation and, as a small, open economy, leveraging foreign demand for growth. This model no longer works in a world of Localization where automated capital produces for local, or domestic consumption. Liberalization of domestic financial and labor markets is needed to promote greater consumption growth.

Taiwan’s external problem, alluded to earlier, is that its leadership position in sophisticated semiconductors is both a blessing and a curse. The economies of scale necessary for semiconductor production remove competitive risks from Localization and create a wide defensive moat. Unfortunately, semiconductors’ centrality to national security creates a strong incentive for other countries to bridge that moat, and they will amid worsening Global entropy. This political reality means that Taiwan’s semiconductor producers will have to pursue a “second-best” strategy and gain comfort with licensing, or “globalizing” their intellectual property through production in the US, Europe and perhaps other economies.

Complicating Taiwan’s transition to the new paradigm of Localization is the necessity to carefully manage Global entropy’s bifurcation. The US, Europe, Japan, and Australia – increasingly an important regional player – are unlikely to look favorably on Taiwanese technology licensing or “outsourced production” if it includes political rivals like China and Russia. Yet, China may see bifurcated licensing that favors the West as provocative and invite unwanted confrontation, especially as it pursues its “Made In China 2025” policy. Despite this complication, I see no choice: Taiwan, if it wants to maintain its political and economic autonomy will have to choose the West for licensing and attempt to placate China with unconstrained Taiwanese-produced supply. This may also provide a disincentive for China to pursue forced reunification that threatens its semiconductor supply.

Finally, Taiwan will have to deal with the challenges presented to all economies by rising real interest rates stemming from redundant Localizationcapexacross economies, especially in the US. But it faces unique challenges due to its neighbors and its unusually concentrated international investment portfolio.

As noted earlier, Japan’s debt is precariously exposed to Japanese residents’ faith in their own governments liabilities at a time when the Bank of Japan is being forced to extricate itself from its experimental policy of Yield Curve Control, or YCC, amid the largest rise in global real interest rates in decades. This represents a low-probability, high impact risk to global financial markets and the global economy.

Taiwan’s life insurers are notorious – and I am not using that word loosely – for selling interest rate volatility to investors globally. That means that if Japanese interest rates move sharply, Taiwanese life insurers are exposed to potentially existential losses from their short volatility positions. Aside from Japan, there is possibly no other economy that is more exposed to Japanese fixed income volatility than Taiwan. While a full-blown debt crisis in Japan remains a low probability, even a hiccup in Japan’s YCC exit, which may come before yearend, could precipitate devastating losses for Taiwan’s volatility sellers.

Unfortunately, the size of Taiwanese volatility selling and the relative illiquidity of volatility markets leave little room for mitigation before a YCC exit likely begins. Hence, my only advice is to stop selling volatility, build liquidity buffers, and hope for the best.

As I would like to end on a high note, I will point out that Taiwan has faced serious challenges in its past and triumphed. Most notably it has risen to the heights of global wealth and technological prowess from an impoverished, isolated province of Imperial China that had been colonized by Japan and liberated by America just 78 years ago. I have every faith that Taiwan will manage its current challenges and look forward to the next, magnificent chapter in its history.

Comments are available to paid subscribers only.