Grading the Fed

Last week’s Fed meeting can only be described as a train wreck. As expected, the Federal Open Market Committee (FOMC) compounded its earlier policy errors with another rate cut, but this time it was so confused and contradictory in its justification that I wasn’t the only one to notice.11 Ironically, the day before the meeting I participated in a Johns Hopkins University online panel grading the Fed – thank you Prakash Loungani of Global Housing Watch for the invite – at which my fellow panelists awarded the Fed A, A- and B. I, of course, gave them an F, even before witnessing Wednesday’s train wreck.

Ranking Fed Chairmen

Before I delve into the specifics of last week’s meeting, I think some perspective on the Jerome Powell Fed is in order. I have been shocked by the number of people in markets, academia and the press that rate Chairman Powell favorably. That was true even before President Trump made a martyr of him. Yet, Jerome Powell is far more likely to be remembered as one of the worst chairpersons in the Fed’s history.

Third worst inflation record in history

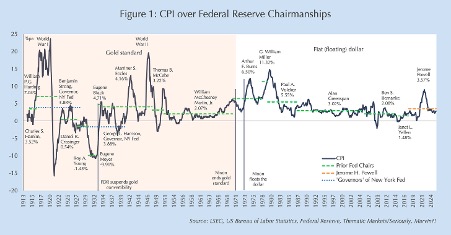

Figure 1 presents an objective measure of Fed chairmen’s success: price stability. With an average inflation rate of 3.57% over his tenure as Chairman, Mr. Powell has the seventh highest record for inflation (of 16 chairpersons) in the Fed’s 111-year history.22 Yet, that flatters him too much. Willam P.G. Harding, Eugene R. Black and Marriner S. Eccles, had to deal with World War I, FDR’s 50% devaluation of the dollar versus gold, and World War II, respectively, all while operating under the more restrictive gold standard where inflation is largely determined by the international price of gold. Of those with worse inflation records in the period since the dollar was floated in 1971, Paul A. Volcker inherited 14% inflation from G. William Miller and is rightly lionized as the greatest of Fed Chairman for bringing inflation down to 3% by the end of his tenure. Thus, a fair reading of Chairman Powell’s term would rank him as the third worst after Mr. Miller and his predecessor Arthur F. Burns, who is widely accepted as the Fed’s worst chairman.

Covid is not an excuse

Many of Chairman Powell’s defenders point to the challenges of managing Covid, but I am unconvinced. First, as I note below the resultant inflation was both forecastable and preventable as it resulted from consistent policy errors. Second, his floating-dollar predecessors also faced large supply shocks like the oil price shocks of 1981 (Volcker), 1990 (Greenspan), and 2006-’08 (Bernanke), and the banking controls of 1980 (Volcker), or demand shocks like the Reagan tax cuts of 1981 (Volcker), the dot-com capex boom (Greenspan), or the Obama stimulus of 2009 (Bernanke). More directly comparable was the 1921-’22 Spanish Influenza that Mr. Harding faced, which resulted in less inflation even though it followed on the heels of a World War and took place under the more restrictive gold standard.

An ignominious legacy

Further, unlike Mr. Powell who inherited 30 years of stable inflation expectations, neither Mr. Volcker nor even Mr. Greenspan benefited from that advantage in mastering the cost shocks they faced. Instead, Mr. Powell has the ignominious distinction of being the only Fed Chairman to dislodged stable inflation expectations in the four decade history of the University of Michigan Survey of Consumers. As with Arthur Burns, who pre-dated the Michigan survey, de-anchoring inflation expectations is likely be Mr. Powell’s enduring legacy with important implications for his successors as I return to below.

Questionable management

Nor has Mr. Powell acquitted himself ably as a manager. As Chairman, Mr. Powell launched the only two Monetary Policy Framework Reviews in the Fed’s history (in 2018-’20 and 2023-’25), both of which I would charitably describe as disappointments. The first changed the Fed’s policy target to “Flexible Average Inflation Targeting” (FAIT) and the second – without admission of error – unwound FAIT after the widely criticized policy contributed to the worst inflation miss in 40 years. Further, as Treasury Secretary Scott Bessent rightly pointed out, neither Review addressed the far more fundamental issues of the potential conflict between the Fed’ regulatory obligations and its core responsibility for monetary policy, or its questionably effective unconventional balance sheet policies that have become a political lightening rod and arguably led to the failures of several large regional banks in 2023.33 (I’ll return to the efficacy of balance sheet policies in next week’s Seriously, Marvin?!)

Under Mr. Powell’s leadership, press investigations into the questionable personal trading practices of two Federal Reserve Bank Presidents, Robert Kaplan and Eric Rosengren, and Vice Chairman Richard Clarida led to their resignations in 2021 and 2022. Yet, even though subsequent investigation by the Fed’s Inspector General found that President Raphael Bostic of the Atlanta Fed had violated Fed trading rules as late as March 2023, he faced no consequences.44 Chairman Powell also presided over the controversial $3.1 billion renovation of the Fed’s three buildings in Washington that cost more than Manhattan’s tallest residential building, Central Park Tower.55

I foresaw it; why couldn’t 400+ economists?

But the core failure of the Powell Fed – and that is the FOMC itself, not just its chairman – is its record on inflation. As I noted above, the worst inflation in over 40 years was both forecastable and preventable. Despite not having 400+ economists working for me – still more if Reserve Bank economists are included – I forecast that FAIT would raise inflation expectations and inflation in November 2020. By early 2021 I was advising clients that inflation definitely was not “transitory” and that the Fed would be hiking rates “like 1994” to over 4% in 2022. Yet, the Fed was so confident in its erroneous inflation and growth forecasts that it continued “Quantitative Easing” (buying bonds) until November 2021.66 Nor am I one of the stopped watches that predicted higher inflation throughout the prior decade; quite the opposite: I was one of the first to identify and predict sustained “Missingflation” during that decade.77

Failure to learn from mistakes

Perhaps I just got lucky or have nonpareil forecasting abilities that are an unfair benchmark for what is arguably the world’s premier economic research institution (my two decade unmatched record of successfully forecasting the global economy’s major trends does suggest the latter is possible!). But that still doesn’t excuse the Fed’s sustained failure to learn from their mistakes throughout this cycle. To their credit, the Powell Fed did (belatedly) hike “like 1994” in 2022 and much to the surprise of markets – but not Thematic Markets’ subscribers – held rates at a relatively high level throughout 2023. Yet at each dip in inflation, without firm evidence that inflation expectations had stabilized and despite a still roaring economy, the Fed either guided markets to think rates would be quickly lowered (December 2023 and December 2024), or erroneously did cut rates (September, November and December 2024).

Do you really understand inflation?

The Fed’s confidence to repeatedly ease rhetoric or actual policy after just a month or two of acceptable inflation speaks to a dangerous hubris and ignorance of what they do not know. A reasonable person might conclude after consistently overpredicting inflation in the previous decade, then underpredicting it for years after Covid, including the third worst inflation of the modern period, that he or she didn’t fully understand the inflation generating process. One might then be a bit more cautious in basing policy decisions on those forecasts. But not the Powell Fed: never an admission of error and full confidence in their continuously wrong inflation forecasts.

“Restrictive” rates

Each time the Committee eases its policy or rhetoric it leans on rates being “restrictive” as an excuse. But as in The Princess Bride, “I do not think [that word] means what you think it means.” When the Fed urgently cut rates by 50 basis points a year ago, the economy had been growing for two years at an average annualized rate of 3.4%, almost double the Committee’s estimate of “potential growth.” At that point real interest rates had averaged almost 3%, or three times the Committee’s estimate for “neutral real interest rates” (aka r*), for three years.88 Notoriously, monetary policy’s lags are “long and variable” but generally not greater than 18 months. While fiscal policy contributed about 0.7 percentage points per year to GDP over that period, it still doesn’t reconcile how GDP managed to grow well above trend (with above-target inflation) if real market rates were so far above “neutral.”

Wednesday’s train wreck

This pattern of consistent failure and hubristic unwillingness to learn from past errors was on full display at last Wednesday’s meeting and even more so at Chairman Powell’s post-meeting press conference. Despite the median Committee member raising their projected paths for both inflation and GDP growth, and lowering their expectations for unemployment, the Committee elected to cut policy rates by 25 basis points with the only dissent being new Governor Stephen Miran’s outrageous vote for a larger easing. The usually subservient press corps zeroed in on this contradiction in the Q&A. They also noted the conflict between Chairman Powell’s contention that downside risks to the Fed’s full-employment mandate had grown relative to the risks to its inflation mandate even as he asserted that slowing employment growth “has more to do with immigration than it has to do with tariffs,” i.e. weak payroll prints are more due to constrained labor supply than slowing labor demand.

“Risk management” amid “restrictive” policy

Chairman Powell attempted to make sense of these contradictions by characterizing the Committee’s decision as a “risk-management cut.” Because the Fed’s models (still) tell them that policy rates are restrictive, labor demand might fall faster. Because bond markets’ long-term pricing and the Fed’s models show inflation returning to 2%, inflation risks can’t be that bad.

Don’t believe your lying eyes, our models know

Never mind that real GDP grew at a 3.3% rate in the second quarter, is projected to grow at the same pace in the current quarter,99 that growth has been led by interest-sensitive capex spending and that announced corporate investment suggests that pace will accelerate, or that nominal retail sales grew at an 8% annualized rate in the most recent three months, this Fed’s models tell it – as they have throughout this cycle – that policy rates are restrictive. Never mind that consumers’ long-term inflation expectations have broken markedly higher for the first time in more than 30 years and that both bond markets and the Fed’s models wholly missed the 2021-’22 rise in inflation. As with “restrictive,” the Fed’s understanding of “risk management” seems to mean something other than the generally accepted definition; i.e., adjusting policy just in case the Fed’s models get it right this time.

It takes a Committee

While I am clearly not a fan of Chairman Powell, it would be a mistake to absolve the rest of the FOMC. And this is perhaps the most fundamental point of this article since Chairman Powell’s sell-by date is fast approaching. The “cool kids” of the FOMC – the chairman, the two vice chairs, and the president of the New York Fed – set the terms of debate and drive the Committee’s direction. But they generally seek a consensus, especially amid a political assault like President Trump’s. Consensus is easier when Committee members’ views are closer to one another. And therein lies the real reason that the Fed cut last week: the range between the highest and lowest estimates for GDP growth, unemployment, inflation, and the appropriate Fed funds rate narrowed at most horizons…toward the dovish center. That made getting to a cut easier, even when it contradicted the change in the median view and required convoluted logic to justify.

Tough shoes to fill

For more than two years I’ve warned (again, and again, and again, and again, and again, and again) that the cool kids – Powell, Williams, Waller, Bowman – have the wrong model of the economy and inflation. Their persistent inability or unwillingness to learn from their mistakes has led to a sequence of policy errors that jeopardizes long-run inflation stability. As noted above, Chairman Powell’s only real legacy will be that of Arthur Burns: that he de-anchored consumers’ inflation expectations. That already makes the job of whomeverfollows him much harder. But inheriting a Committee full of Powells, Williams, Wallers, and Bowmans will be the next chairman’s real challenge.

Bonds’ soft underbelly and long tail

While the implausible “Miran dot” and what it may imply for President Trump’s intent for the Fed is a serious concern, bond markets’ more tangible worry should be the convergence of the Committee to its dovish, misguided core and the mess they’re leaving for the next chairman. The best case scenario is that they recognize their errors too late and are compelled to hike aggressively next year and beyond (1-year, 1-year forward interest rates did finally jump at the end of last week). A more troubling case is that the next Fed chairman is a G. William Miller who further accommodates the rise in inflation expectations his predecessor bequeathed to him. And of course, the worst case is that the “Miran signal” is a valid indicator of the future of the FOMC: one focused on government finance at the expense of monetary and price stability.

While term premia have risen sharply this year, ironically the Fed hasn’t been the driver. Maybe it should be.

Next week I’ll discuss if and how Quantitative Easing and “Quantitative Tightening” work.

Comments are available to paid subscribers only.