“Who is ever going to use stablecoins?!”

My fiancée, Joy, was incredulous regarding my growing conviction that stablecoins will transform the global financial system: “Who is ever going to use this complicated, fake money that is impossible to understand?” Two minutes later (literally), “Hey, I just created a stablecoin account with a debit card I can use anywhere!” Me, under my breath, “Yep, I told you so.”

That interaction and the US Congress’s passage of the GENIUS Act, providing a regulatory framework for stablecoins, convinced us to write companion articles this week on stablecoins. While Joy, a chartered accountant who puts the Joy in The Joy of Accounting, is delving into the accounting treatment of stablecoins, my focus here is explaining why their uptake is likely to be more rapid and transformative than the consensus expects, and perhaps different from what some stablecoin proponents expect.

Stablecoins as global “payment rails”

If you don’t know what a stablecoin is, you should first read my earlier piece explaining how they relate to the concept of “narrow banking.” Even if you know what stablecoins are, you may want to start there. A key takeaway is that while stablecoins are often framed as “money,” it is better to think of them as payment systems like the Visa network. While these payment networks – sometimes called “payment rails” – can use any currency, the vast majority use one currency: the US dollar. The US government’s legal and regulatory adoption of stablecoins is likely to cement and even increase the dollar’s dominance, both in stablecoins and the global financial system. And it is likely to happen fast.

Why stablecoins will take off faster than expected

Stablecoin growth is likely to surprise even crypto enthusiasts for the same reason the internet and social media gained traction faster than earlier technologies: all the necessary infrastructure is already in place. When Mosaic, the first internet browser, was launched, fixed-line telecommunications were ubiquitous, a near majority of American households had personal computers, and scientists had been using the DARPA-funded proto-internet for over a decade. Similarly, each successive generation of social media has grown faster than the previous one because all the infrastructure – mobile telephony, smart phones and internet protocols – already existed. Only cultural adoption was necessary.

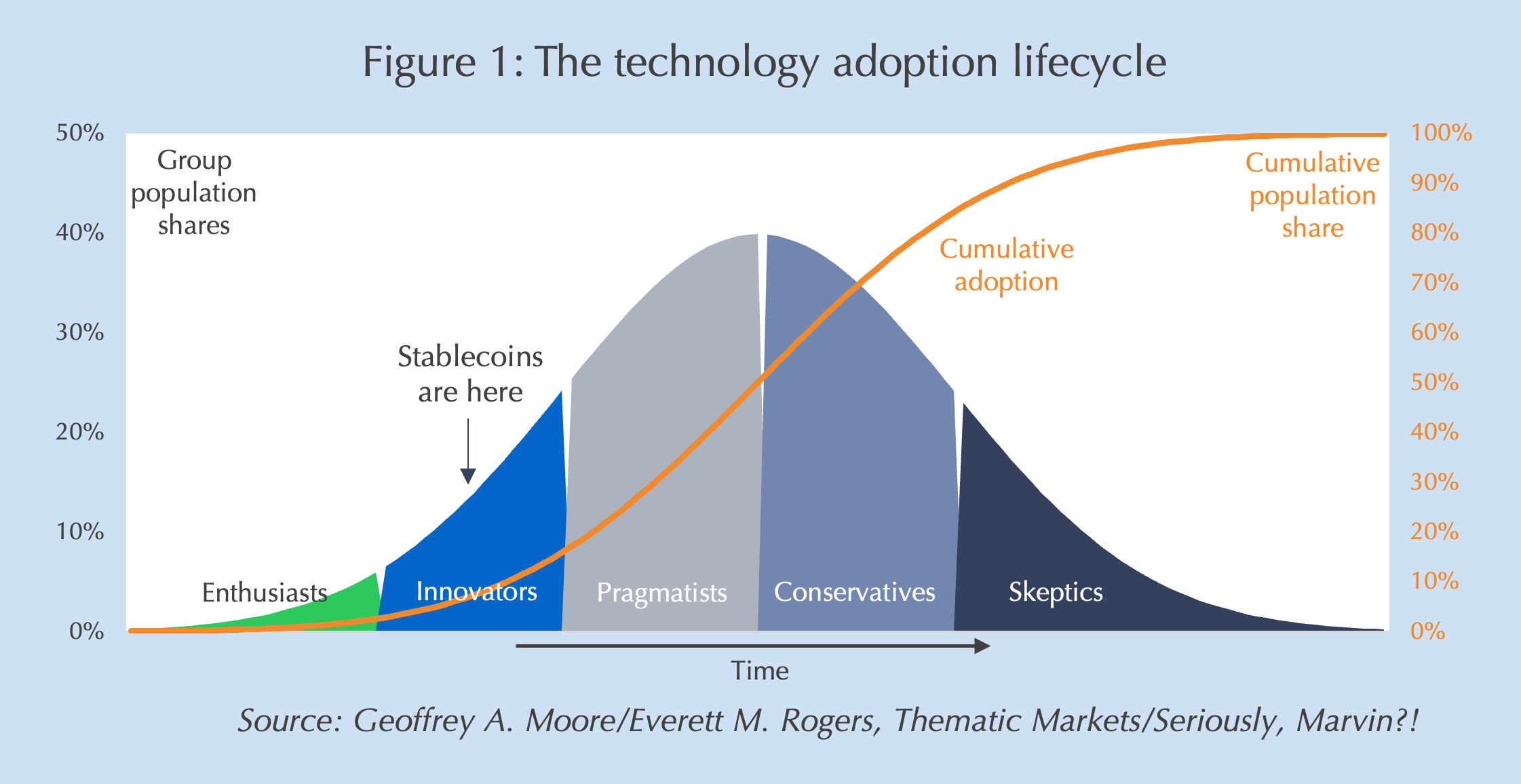

The technology adoption lifecycle

Geoffrey Moore, building on the ideas of Everett Rogers three decades earlier, described the rate of adoption of new technologies as a “lifecycle” spanning its uptake by five societal groups: fringe “enthusiasts” who originate the technology, followed by a minority of “innovators” who are early adopters, then the majority of people who are “pragmatists” that jump on the bandwagon and “conservatives” who only join when it is clear the technology is taking over, and finally “skeptics” who are resistant to any change (Figure 1).11

Enthusiasts completed the necessary architecture

Crypto enthusiasts created stablecoins to facilitate trading between crypto currencies: it was useful to have a stable price reference on blockchain to trade Bitcoin for another crypto currency like Ethereum. The digital dollar on blockchain, aka stablecoin, was born. Their efforts built the necessary “connective tissues” that made it so easy for Joy to set up a crypto account without any prior knowledge: the financial technology (FinTech) for on and off ramps from the traditional financial (TradFi) system to crypto platforms, and the “Layer 2” software that scales existing crypto currency platforms to handle the speed and volume of transactions necessary to be competitive payment systems.

Innovators have begun the acceleration

Enthusiasts’ construction of the final bits of stablecoin infrastructure opened the doors to the innovators, the early adapters who help normalize and create the scale necessary for accelerating adoption by others. It is the innovators who begin the exponential phase of growth shown by the orange line in Figure 1. The key driver, as with expansion of any other technology is cost relative to incumbents. This is why most of the stablecoin adoption outside of the crypto enthusiast community has come in the international payments space, especially from migrants remitting money to relatives in their home countries. In the traditional system, wiring $200 typically costs about 6% but can cost as much as 10% and may take days to effect with little transparency; the same transaction via stablecoins is instantaneous and transparent, and costs 0.5% to 3%.22

Pragmatists take up the baton for peak acceleration

Pragmatists, too, are driven by cost concerns by need evidence of a practical business case. That can come from a critical mass of users created by innovators, regulatory endorsement, or cost declines or productivity gains driven by both. But it also comes from peer validation: adoption quickens as more users embrace the technology. All those ingredients now are in place and create a virtuous circle of rising stablecoin use: official sanction and regulation by the US government raises trust in stablecoins as a means of payment, rising trust begets increased usage, which both increases use and further reduces costs, raising trust and usage further, and so on.

Business adoption in its infancy

Businesses are the critical group of pragmatists and the largest segment of the international payments market. To date, business usage of stablecoins is in its infancy and largely concentrated among small importers in financially underdeveloped countries.33 Among established Western businesses, use of stablecoins has been concentrated among international payments providers jockeying for market share in the global remittance market,44 though SpaceX reportedly has used stablecoins to handle Starlink payments from financially underdeveloped countries.55 But as Joy discusses in her companion piece, by legitimizing and clarifying regulatory and accounting treatment, government sanction provides the critical push for businesses to take advantage of the cost savings that stablecoins can enable.

Youth drive accelerating consumer growth

Business adoption also is encouraged by consumer adoption, which is accelerating particularly among the young as it has with FinTech.66 Younger consumers adopted digital payments and non-bank financial accounts like pre-paid cards faster than their older peers.77 But youth adoption was critical to the development of infrastructure like retail point-of-service (POS) payment capabilities that facilitated adoption of digital payments by older consumers.88 The next stage of stablecoin normalization – and declining transaction costs – likely will be the replacement of bank-based POS systems that complete the “last mile” for today’s stablecoin payments with direct stablecoin payment. Indeed, it already is happening: Stripe the company that Substack uses for subscriber payments charges half as much for stablecoin payments (1.5%) versus traditional card payments (2.9% plus $0.30).99

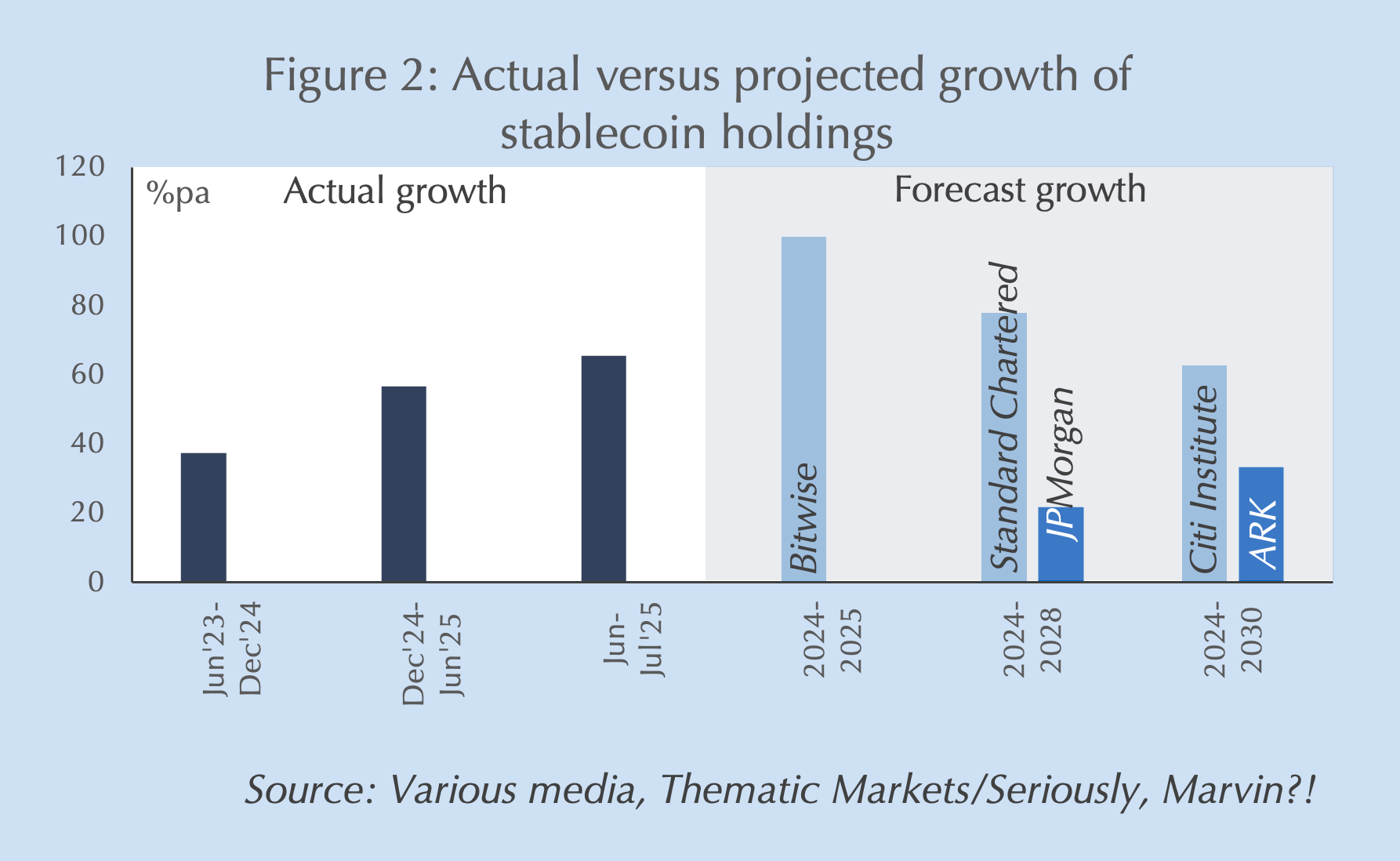

Consensus estimates for growth probably are too low

While the orange line in Figure 1 is a figurative representation of cumulative adoption rates, it accurately represents the observed pattern of technological adoption: a logistical function that initially grows slowly before exploding exponentially and finally slowing again as full adoption nears.1010 The shift to exponential growth begins with adoption by innovators and accelerates in the handoff to pragmatists. While one could argue how far we are through the “innovators” phase, it’s difficult to argue that stablecoin adoption won’t accelerate markedly given already-in-place infrastructure and the regulatory boost from the GENIUS Act. Yet, most market forecasts of stablecoin holdings over the next three to five years show a deceleration in growth (Figure 2).

Only Bitwise’s single year forecast for 2025 and Standard Chartered’s three-year forecasts show any acceleration in growth of stablecoin holdings. Even ARK, the notoriously pro-crypto investment manager, forecasts five-year annualized growth of 33%, only half its most recent, post-GENIUS Act pace of 65%. Given that global contactless card payments – nearly thirty years after introduction and 15 years after widespread rollout – are still growing at rates over 50%,1111 these forecasts seem conservative relative to previous technological adoption cycles. Further, the numbers being forecast are stablecoin holdings, not usage. Non-trading usage of stablecoins – i.e. for remittances and commerce – grew an astounding 288% in the last year and is likely to grow faster still as the velocity of stablecoins transactions (recycled use) rises with adoption.1212

Why does it matter?

At this point some readers are beginning to wonder “why does this matter?” while others are likely getting excited for what are probably the wrong reasons. Let’s start with the latter.

Stablecoins do not bring down US Treasury yields

US Treasury Secretary Scott Bessent and many others have gotten excited about the potential for stablecoin adoption to lower US interest rates by creating a “new” source of demand for US debt. But this is robbing Peter to pay Paul. While every dollar of stablecoin issuance must be backed one for one with US T-bills or like instruments, no new demand for US debt is created since stablecoin creation robs banks of deposits. To offset the lost deposit, the bank can either sell T-bills and delever, or issue new commercial paper or bonds to fund its loan portfolio. Either way, net credit in the economy is unchanged. There are some implications for credit spreads and swap rates that I covered in my research at Thematic Markets, but interest rates are unaffected.

But they could reduce US seigniorage…

There are two potential exceptions to this related to non-US users of dollars. The first is if foreign holders of physical US dollars exchange them for more convenient dollar stablecoins. That doesn’t increase demand for T-bills but it does reduce US seigniorage revenue. The drop in demand for Federal Reserve currency liabilities causes it to sell an equal amount of its own T-bill holdings, offsetting stablecoin issuers’ purchases, but it also reduces the interest the Fed earns and remits to the US Treasury.

Or possibly strengthen the dollar

The other exception is if US regulation of dollar stablecoins increases foreign demand for dollars, creating truly new demand for US T-bills. Yet the impact on interest rates is ambiguous in this case. Because foreign assets or debt are being sold to buy dollar stablecoins, the global supply and demand for savings isn’t changing, just its currency composition (dollars up, other currencies down). But that may show up as a stronger dollar rather than a fall in US T-bill rates.

Increasing dollar dominance

This last case isn’t hypothetical. Even before the passage of the GENIUS Act, the US was already a net exporter of dollars stablecoins.1313 I expect that to increase. More than 98% of stablecoin issuance is denominated in dollars despite most stablecoin demand being outside of the United States.1414 For many frontier and some emerging economies where monetary systems are unstable and large portions of the population are unbanked – but have mobile phones – the ability to easily obtain and transact in US dollars is a key driver of growing demand for dollar-denominated stablecoins. Importers struggling to obtain traditional sources of foreign exchange are using the rising supply of remitted stablecoin dollars to pay foreign suppliers, while consumers and businesses get respite from inflation conducting business in dollars even in countries where use of foreign currencies in commerce is illegal.1515

Stablecoins as Shiva, the destroyer…and creator

The easy availability and usability of dollar stablecoins throughout the world turns them into a monetary Shiva, the Hindu god of destruction and rebirth. In increasingly shrill tones central banks outside of the US are beginning to worry about the rise of dollar stablecoins…with good cause.1616 In countries struggling with monetary credibility and effective controls, an effectively unlimited supply of hard currency on a safe, regulated payment system that anyone can access on their phone anywhere threatens the very existence of their sovereign currencies and seigniorage. But even central banks with more credible inflation-fighting track records and well developed financial systems face a significant threat from regulated dollar stablecoins: bank runs. Imagine an alternative future to the 2011-’12 European banking crisis where Italians and Spaniards could immediately convert their euro bank deposits at Monte del Paschi and Bankia to dollar stablecoins instead of transferring them to Deutsche Bank (who immediately lent the funds back to the southern European banks via the European Central Bank). Would the euro still exist today?

But dollar stablecoins simultaneously offer a huge potential opportunity in many of the world’s poorest and most financially underdeveloped economies. Just as mobile communications technology allowed many of these countries to leapfrog past the expensive infrastructure of fixed-line telephony,1717 dollar stablecoins could allow them to escape chronically corrupt financial regulation and banking systems. The ability to transact in dollars through smart contracts embedded in the underlying blockchain of the stablecoin’s payment rails opens the door to commerce and credit that would require decades of financial development even if political reforms were feasible.

Don’t let me tell you “I told you so.” Get ready. Stablecoins are going to transform the global financial system and it will happen faster than you think.

Comments are available to paid subscribers only.