No, it isn’t April Fools Day…

You could be forgiven for thinking it was April (Fools Day) or that some prankster had replaced your FT or WSJwith The Onion or Babylon Bee last week. The Sunday before last, in broad daylight while the museum was open, four masked burglars drove a truck with an extendable ladder alongside the Louvre in Paris, slowly extended the ladder to a second-floor balcony to enter the museum via a window that they breached with power tools, smashed display cases to seize irreplaceable French crown jewels worth an estimated €88 million, scampered back down the ladder, and then absconded on motor scooters.11

It’s just another accidental prisoner release

Not to be outdone, British authorities twice in the days that followed proved themselves even more incompetent. Three days after the Louvre humiliation, the first “one-in-one-out” asylum seeker returned to France under a deal negotiated between Prime Minister Sir Keir Starmer and President Emmanuel Macron, snuck back into the UK less than a month after deportation.22 A few days later, British prison authorities accidentally released the UK’s most notorious sexual predator and asylum seeker, whose assault of a teenager had led to sustained civil unrest this past summer.33 Adding to the Keystone coppery, after Hadush Kebatu had spent 90 minutes in front of the prison soliciting passersby for directions, a helpful Bobby pointed him to the train station.44 And this was no one-off mistake: as a result of the cockup, Britons learned that Mr. Kebatu’s release was one of 262 accidental prisoner releases in the last year!55

Farcical façade has real ramifications

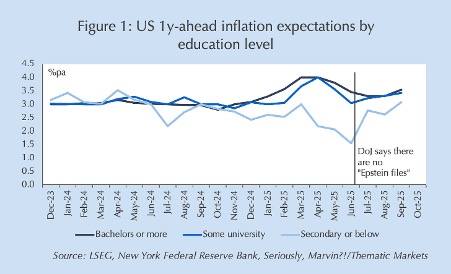

These stories may seem farcical fodder for tabloid covers and TikTok memes, but I expect them to have significant political and market consequences. If that seems far-fetched, recall that earlier this year I forecast that the Trump Administration’s non-release of the “Epstein files” risked reigniting inflationby undermining his voters’ faith in his ability to bring down inflation.66 Yet, as is often the case with my predictions – you have subscribed, haven’t you? – exactly that happened as shown by the jump in lower-education consumers’ inflation expectations shown in Figure 1 (note that their expectations had moved in the opposite direction to educated consumers who were more likely to vote for former Vice President Harris). Sometimes, things that seem inconsequential to the cognoscenti become totems for the masses.

Cutting to the core of the Politics of Rage

The Epstein backpedal was significant because it was a breach of covenant with Trump voters. The Anglo-Gallic farces are instead serious because they cut to the core issues that have fueled rise of the Politics of Rage, the four-decade-old voter rebellion against their betters.77 The critical driver of “populism,” as it is more commonly called, is ordinary voters’ sense of disenfranchisement due to the divergence in interests between them and the elites they elect to represent them. The two greatest elite-commoner divides across Western countries are immigration and sovereignty. Elites value cheap labor, frictionless business and globetrotting; ordinary citizens resent the resultant wage suppression, housing and healthcare pressures, and cheapening of their “first-world” citizenship.

Lingering reminders

Last week’s embarrassments are likely to linger in the public consciousness as reminders of those deeper tensions. The demonstrated failure of Sir Keir’s “one-in-one-out” policy and the accidental release of Hadush Kebatu the same week are damning indictments of UK asylum policy – adopted from EU law after Brexit – that has inflamed many Britons. The reason for Mr. Kebatu’s asylum claim remains unknown, but after being sentenced to a year in prison in the UK for sexually assaulting a 14-yearold girl and another woman within a week of entering the UK, Mr. Kebatu apparently felt safe enough to request that he instead be return to Ethiopia (a request that was granted; Mr. Kebatu was due to be deported when he was mistakenly released).88

Of true “exorbitant privilege”

The robbery of French national treasures is not directly related to French immigration policy, but the fact that at least one of the suspects is a dual Algerian-French national is likely to turn the scandal into an immigration issue.99 More pointedly, the Louvre heist serves as reminder of elites’ lack of accountability: Even after offering her resignation, the museum director faces no consequences for the spectacular security failure at the world’s most-visited museum despite admitting that security upgrades whose need was well known were delayed, that there were no security cameras in the area, and that while alarms supposedly worked, no one responded within the seven minutes taken by the burglars despite the museum being open to the public.1010

And a history of incompetence

Perhaps more pertinent, last week’s debacles were a stark reminder to voters of the staggering record of incompetence in recent decades by Western leaders from both the center left and center right. The list of their failures long and damning: costly inconclusive or losing wars in Afghanistan, Iraq, Libya, Serbia, Syria, and Ukraine, waves of immigration following each, the Global Financial and European Monetary and Banking Crises, lockdowns that yielded no improvement in mortality rates relative to jurisdictions that didn’t implement them but resulted in far worse social and economic costs, and a Brexit execution that generated no tangible economic gains but adopted EU laws and increased immigration, despite those two issues being the first and second most cited reasons for Leavers’ votes. This litany of failure has shattered trust in government across the West.

Making mockery great again

Perhaps most damaging for center parties in Europe, not just Sir Keir and President Macron, is that it opens them to general mockery rather than usual partisan variety. Even Labour and Renaissance diehards will feel foolish defending their leaders from due ridicule in pubs and brasseries across the UK and France. But it is unlikely to stop at the Rhein and Pyrenees: their center-left/right partners across Europe will be opened to the same popular jeering due to their own embarrassing failures this year, including:

- German Chancellor Friedrich Merz’s historic failure to be elected on the Bundestag’s first vote,1111 nearly collapsing his two-month-old coalition with his endorsement of a Constitutional Court nominee whose views are at odds with his own party and is accused of plagiarism,1212 and most substantively breaking his campaign pledge on German’s “debt brake” to boost defense spending but arguably hobbling its efficacy by agreeing that much of the exempted spending must aim to achieve “climate neutrality by 2045.”1313

- Spanish Prime Minister Pedro Sanchez was embroiled in a corruption scandal that involved his most senior deputies1414 and oversaw the worst blackout in European history after the Iberian grid failed for three days due to overreliance on solar electricity generation without sufficient infrastructure to offset its fluctuations, a fact that he continues to deny.1515

- The European Commission admitted that it had misused grants from a €5.4 billion environmental fund to lobby EU member governments,1616 and more substantively suffered the perceived humiliation (the actual deal was not as bad) of bending to President Donald Trump’s trade demands after a half year of tough but hollow threats.1717

Et tu, Brut?

Populist leaders, too – notably President Trump – have had their fair share of embarrassing displays of incompetence in the last year, from including uninhabited, non-independent islands (Heard and McDonald Islands) on his “Liberation Day” tariff list, to announcing H1-B visa changes late on a Friday night. But there is a big difference between embarrassing rollouts and failing policies. Like his policies or not, except for the Epstein files that remain a thorn in his side, President Trump is largely delivering on his election promises with better-than-expected results:

- Implementing widespread tariffs without significant negative economic consequence;

- Severely reducing illegal immigration into the US;1818

- Attracting $2 trillion in year-to-date investment commitments to the USdespite the sharp rise in policy uncertainty;

- Passing legislation to eliminate taxes on tips, overtime and Social Security benefits;

- Reducing the primary budget deficit through 2028; and

- Deploying the National Guard to sharply reduce violent and property crimes in Washington, DC (even being thanked by Washington Mayor Muriel Bowser, who opposed the deployment).1919

One can site similar achievements for Prime Minister Giorgia Meloni of Italy, including a 3.4% fiscal consolidation that is one of the largest in OECD history (and yet still resulted in GDP growth better than Germany). Or, Javier Milei’s economic growth and budget balancing success in Argentina that has resulted in a major surprise electoral victory over the weekend. The point is, that populists across the world are delivering on their promises and attracting voters with competent governance at a time when the traditional center-left/right parties are making themselves the butt of jokes (and objects of voter ire).

Performance-based legitimacy

The greatest political scientist of the last century (ever?), Samuel Huntington, described almost 60 years ago a formula for governing legitimacy that has proved immensely successful with autocrats in Asia and the Middle East: “performance(-based) legitimacy.”2020 By meeting citizens’ needs for security, stability and sustained income growth, autocrats in these countries have been able to not only maintain power, but popularity with their citizenry. Mr. Huntington theorized that democratically elected governments did not need to meet as high a threshold for competence because their legitimacy derived from election by their citizenry. However, he did not tackle the question of a minimum bound before citizens throw out their elected representatives. Europe’s center-left/right governments appear to be testing that boundary.

Populist wave?

Italy, Belgium, Czech, Hungary, and Slovakia all now are led by right-wing populist governments, while the governments of Denmark, Finland, Sweden, and Switzerland, all either include populist parties or rely on their confidence and support (additionally, the caretaker government of the Netherlands was installed by the populist Freedom Party who is again leading in the polls for this week’s election). Populist parties continue to make gains across Europe, both in polling and in recent elections in Austria, Norway and Portugal.2123

The big three economies most under threat

While the big economies of France, Germany, and the United Kingdom do not face scheduled elections until 2029, all three governments are unstable, suffering from crises of legitimacy, and are behind in the polls. Friedrich Merz’s coalition government seems to lurch from one crisis to another despite being less than six months old and has fallen narrowly behind Alternative für Deutschland in polling. President Macron’s 2024 gamble to call early legislative elections and coordinate tactical voting against the populist National Rally (RN) party backfired, resulting in an ungovernable parliament and a succession of failed governments. Even some allies of President Macron are now suggesting he leave office early and call elections to resolve the crisis, with RN holding a significant lead over other parties.2222

Watch for the backbenchers’ knives

But it is Sir Keir in Westminster that is in the most immediate danger. For much of this year polling shows the new populist Reform Party winning an absolute majority in an early election – potentially the largest single-party majority in British history – with the traditional ruling parties, Labour and the Conservatives, falling to a distant third and fifth!2323 But that is not Sir Keir’s imminent danger. As I warned before the 2024 election, the combination of Labour’s large majority, popular dissatisfaction with them – their electoral victory resulted from a vote against the Conservatives rather than for Labour – and Sir Keir’s ties to the Blairite wing of the party run the risk of an internal coup before the 2029 election. The writing appears on the wall for Sir Keir after this week’s historic by-election loss of a seat that Labour had held for a century in Wales and the election of one of his foes as Deputy Leader of the party.2424 A popular, young and much further left mayor of Manchester, Andy Burnham, is apparently already being urged to challenge Sir Keir for the premiership.2525

Are markets prepared?

Europe is already struggling with anæmic economic growth, persistently high inflation, high energy costs, serious debt sustainability questions, and rising needs for defense expenditures with a war on its doorstep, yet markets seem remarkably complacent. I’m commonly asked if UK gilts look attractive at these levels (no) and EURUSD risk reversals – the premium for call options over put options – are positive from 1 month through 5 years (insane). The UK is at serious risk of a sharp turn to the left that likely will have significantly negative implications for its currency and its relations with President Trump (who recently came to visit bearing £100 billion in gifts that he might call back). France, with the least sustainable debt in Europe, is ungovernable and potentially on the verge of early elections. Even Germany, formerly Europe’s Atlas but more recently its sick man, appears at risk of political instability. The only potential good news is that the record of European populist governments – if they get a chance to govern – is for greater fiscal responsibility than their traditional centrist peers. Clearly, I meant the question in the subtitle rhetorically.

Epilogue: Jackson, Sulla or Cæsar?

I suppose that I can’t cast Donald Trump as delivering Huntington’s “performance-based legitimacy” without returning to the question I posed last November in my preview of his second term (free at Thematic Markets): will he prove to be the return of Andrew Jackson, Sulla or Cæsar? With nine months of evidence, I still lean towards Jackson. Indeed, I would suggest that all his behavior and policies strongly align with the seventh US president. Rather than performance-based legitimacy, he seems to be delivering what European center-left/right parties cannot: performance-based electability. But Sulla or Cæsar remain possibilities; only time will tell.

Comments are available to paid subscribers only.