Note: Just as I was scheduling this to publish, news of the two-weeks ceasefire and opening of the Strait of Hormuz was announced. Scenario 1 now could be recast as a temporary ceasefire, but otherwise there is little here that I would change.

Uncertainty means we don’t know

It seems an obvious point, but bears repeating: we are living in immense Uncertainty with the potential for catastrophic outcomes. The US-Israeli war with Iran may be the most consequential geopolitical event since World War II and has the potential to have a tremendous impact on both the global and on individual economies. No one knows how long the war will last, how much damage it will do to Persian Gulf infrastructure, oil and gas production and refining, and related production of other critical inputs to the global economy. Nor do we have any idea for how long or to what extent the Strait of Hormuz will be compromised. This week’s article is a little longer than usual, but it’s hard to gain “perspective” with brevity.

Navigating between false certainty and hyperbole

Unfortunately, Uncertainty of this magnitude typically begets two near-polar-opposite reactions, neither of which is particularly helpful. The first is to blindly apply models trained on “normal” data, i.e. a supply shock to crude oil of X leads to GDP losses of Y and inflation of Z. This ignores nonlinearities associated with the potential size of the current disruption and the huge changes that have taken place in individual economies like the transformation of the US from the world’s largest energy importer to its largest producer, or China from an impoverished backwater to the world’s largest manufacturer and energy importer. The second reaction is to lean into the unprecedented potential of the shock and make hyperbolic claims like “the world economy will not survive.”1[1]

“Satisficing” or “good enough”

One of the best methods for addressing Uncertainty — non-quantifiable risk — is to engage in scenario analysis: what are the possible outcomes you can envision and what are their potential consequences? With deep Uncertainty, like that we face today, you likely will not correctly guess all the possible outcomes, but mapping best guesstimates of the likely effects of a sufficient number of scenarios likely will encompass the range of potential ramifications. Economist Herbert Simon, in his Nobel Prize-winning theory of “bounded rationality” in decision making, called this process “satisficing” (a portmanteau of satisfy and suffice), but generations of humans before him called it “good enough.”2[2] Hence, bounding the range of potential outcomes with a robust set of scenarios, then comparing those boundaries with past disruptions that “rhyme” likely gives us a“good enough” estimate of the limits of possible.

Scenarios

By the time you read this, President Trump’s ultimatum to Iran will have passed and you may be able to cross some or all of these scenarios off the list, but here are the eight most plausible resolutions to the crisis that I see (ordered from least disruptive to most disruptive):

- Imminent negotiated settlement: Although Iran’s escalatory attacks in the last 24 hours argue against it, I would not discount that the sharp escalation in President Trump’s rhetoric represents a face-saving off-ramp for whoever now runs Iran to agree to a near-term negotiated settlement (“We submitted to save the people of Iran!”). This would be consistent with President Trump’s de-escalatory offerings following both his assassination of Quds Force commander Qasem Soleimani in January 2020 and the bombing of the Fordow nuclear facility last June, both of which were followed by perfunctory, face-saving and nonlethal missile salvos by Iran at (emptied) US military bases.3[3] In this case, the Strait of Hormuz reopens and repairs to destroyed infrastructure begins immediately.

- Trump Always Chickens Out: This is the least likely outcome in my view for the reasons I laid out in Alea iacta est, but I include it for completeness. In this fairytale, the US declares victory and walks away — and just as importantly — Israel and the Gulf Arab states that have been under continuous attack from Iran also accept the war’s end and Iran’s de facto future suzerainty over the Strait.4[4] As in case (1), the crisis would effectively end, the Strait would reopen, and rebuilding could begin. At least until the inevitable collapse of the unstable equilibrium it creates.

- The Islamic Republic collapses: It’s difficult to assess how strong the Islamic regime’s grip on power remains: continued retaliatory missile and drone strikes from independently distributed command structures and clever “Lego Movie” propaganda videos do not a functioning state make. Israeli strikes on the Republic’s command and control structure and internal security forces have been brutal. The regime could collapse tomorrow, next month, or next year, but depending on how long the US and Israel are willing to continue, no regime can indefinitely survive this scale of destruction and economic dislocation.

- War continues but Iran opens the Strait: Iran’s closure of the Strait of Hormuz was a hybrid-warfare strategy intended to pressure the US to relinquish its kinetic advantage. But one of the points I made in Alea iacta est is that President Trump effectively turned Iran’s strategy against it by credibly noting Iran’s supporters, not the US, need the Strait open. While those countries may ultimately blame President Trump, his “put” of the Straits problem to them effectively pressures Iran. I strongly suspect that Iran’s recent shift to allow ships from “Brother Iraq,” China, India, and other countries through the Strait reflects a realization that blocking it no longer serves Iran’s interests. Even if Iran continues to restrict (nonexistent) US tankers from the Gulf, an expansion of exemptions (or reflagging) effectively opens the Strait, likely fully within months.

- US seizes the Iranian coast and oil production, opening the Strait: The US has one Marine Expeditionary Unit (MEU) in the region, another arriving next week, and has mobilized the Army’s Immediate Response Force (IRF), some elements of which already are deployed. President Trump has explicitly held out the possibility that the US will take Iran’s oil. If the primary US war objectives are as I postulated in Alea iacta est, not to stabilize Iran, but to eliminate Iran’s nuclear threat permanently, end the Islamic Republic’s 47-year war on the US, eliminate a Chinese proxy state in West Asia, and control the flow critical resources to China, then seizing Iran’s oil and gas distribution hubs on the islands of Kharg, Lavan and Sirri, the UAE-claimed, Iranian-held islands of Abu Musa, Greater and Lesser Tunb in the Strait itself, and the Iranian loading terminal at Jask, just outside the Strait on the Arabian Sea, while promoting civil war inland until a US-friendly regime emerges shouldn’t be discounted. Combined with an effective shipping insurance regime, which the US is reportedly working on, this likely would (mostly) reopen the Strait while slowly strangling what is left of the Islamic Republic.

- US leaves the world to sort it out: As noted above, I think the consensus version of “TACO” is unlikely, But as I wrote in Alea iacta est, I think President Trump’s threat to walk away and let others sort out reopening the Strait is his most likely stop-loss if the Iranian regime doesn’t submit on his timetable. In this scenario, the US likely fosters a civil war by supporting Azeri, Balochi and Kurdish separatist movements and anti-government Persian insurgents, destroys most Iranian infrastructure, and leaves Israel and the Gulf Arab countries to ensure that the Islamic Republic never becomes a threat again.5[5] Assuming I’m wrong about scenario (4) and Iran retains the ability to target ships, the fate of the Strait remains uncertain, but “toll” revenues will become even more essential to the regime (or local warlords) making it more porous than today.

- Iranian production destroyed: Extensions of scenarios (3), (5) and (6) include the possibility that the US or Israel destroy Iranian crude oil and gas production and distribution facilities, having already heavily bombed the country’s petrochemical complexes and leveled its steel production. This likely would remove Iranian production from global supply for at least two years and potentially a decade.

- Most Gulf production destroyed: The most catastrophic (economic) scenario is that both sides remove current redlines that have so far protected (most) oil and gas production and distribution infrastructure, and that Iran retains the capacity to effectively attack other Gulf states’ hydrocarbon infrastructure. The fate of the Strait becomes largely irrelevant if the sources of production for 20% of global oil and gas, 25% of helium, 35% of nitrogen fertilizer precursors, and 45% of global sulphur trapped behind it are destroyed. Nothing will leak out then.

A century and a half of perspective

While history rhymes rather than repeats, perspective on past shocks to the global economy is both essential to make “good-enough” guesses about the effects of large disruptions and to appreciate how resilient the world economy is. One of the more disappointing aspects of analyses I’ve read on the potential effects of this war is the short histories on which they’re based. Truly large shocks to the global economy — like a closure of the Strait of Hormuz — are extremely rare, and only a very long sample is likely to reveal a “rhyming couplet.” In the Appendix I’ve compiled a list of major supply shocks to the global economy spanning the last 155 years.

Complex systems

A long history like that reveals two important characteristics of the global economy: it is simultaneously nonlinear and surprisingly resilient. These are characteristics of complex systems, of which the global economy is a great example. Complex systems respond to shocks in unexpected ways due to the intricacy of their structure. But they also are always operating in “failure mode;” i.e. something is always going wrong. That makes them quite resilient as failures are normal and strengthen self-healing mechanisms. One illustration of this is the long list of major disruptions to the global economy that has occurred over the last century and a half. Note there have been seven just in the last decade and a half. Food supply and supply-chain failures in the early 2010s, followed by the massive Covid shock, the Ever Given blockage of the Suez Canal, and the Russian invasion of Ukraine all have increased the resiliency of current supply chains, a fact that may be present in the surprising resilience of equity prices and lower-than-expected crude oil prices.

Two historical parallels to consider

While there are many relevant comparisons to some of my eight scenarios above, two are especially pertinent to the more extreme scenarios of prolonged Strait closure or massive infrastructure damage that impairs a significant share of Gulf production: the Iranian Revolution and Iran-Iraq War that followed it; and the Russian Revolution against the backdrop of World War I.

47 years ago

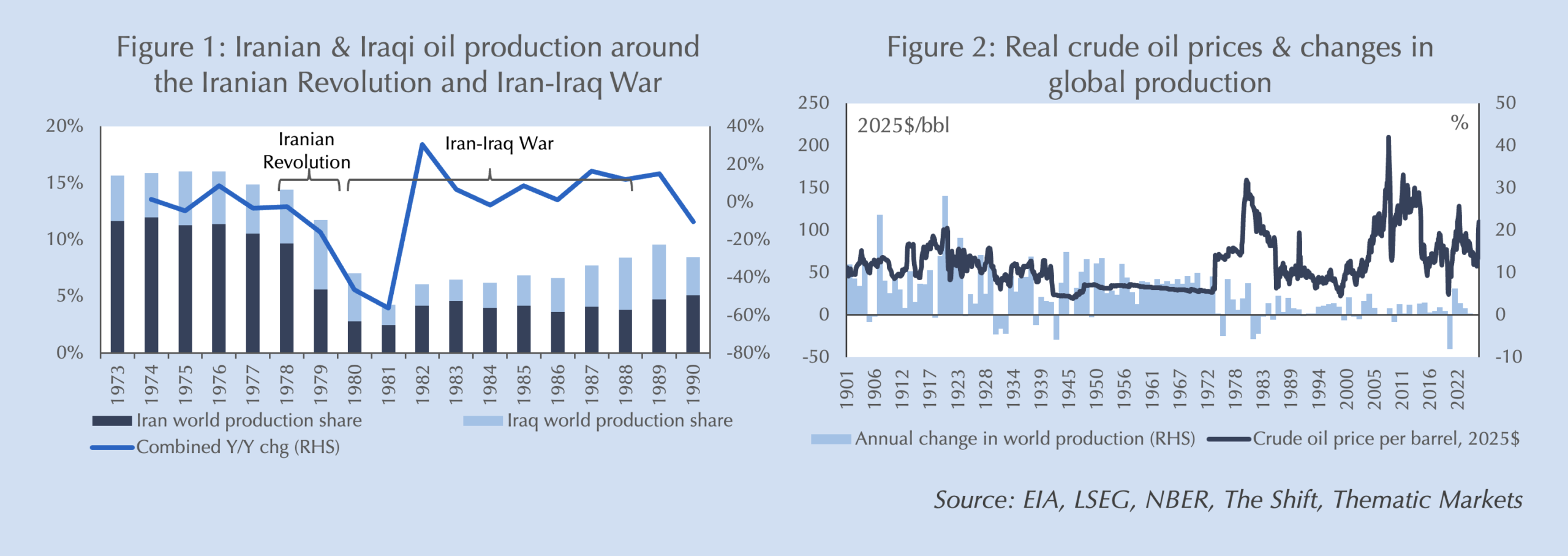

On the cusp of the Iranian Revolution, Iran produced 6 million barrels per day (mbd) of crude oil, almost 12% of global output; by 1981 after its 1978-’79 Revolution drove out many of its skilled technicians and Iraq invaded in 1980, attacking Iranian oil fields, production fell below 1.4mbd, or 2% of global production (Figure 1). Due to Iranian counterattacks, Iraqi production fell 2.5mbd from its 1979 high. The combined fall from 1978 to 1981 was 10% of global supply. The net global loss of supply was a smaller 6% due to rising US and North Sea production but it still tied 1942 for the largest annual supply disruption of the 20th century (Figure 2). There are two important lessons to draw from this episode. First, the gross supply disruption half century ago was roughly on par with the current blockage — once pipeline and “toll” leakage is accounted for — on a flow basis, about 12% of global supply. But to equal the total supply shock of that crisis, the current one would need to go on for another year or more. Second, as noted, the global economy is resiliently self-healing: new sources of supply offset roughly half of the huge fall in Iraqi and Iranian crude.

109 years ago

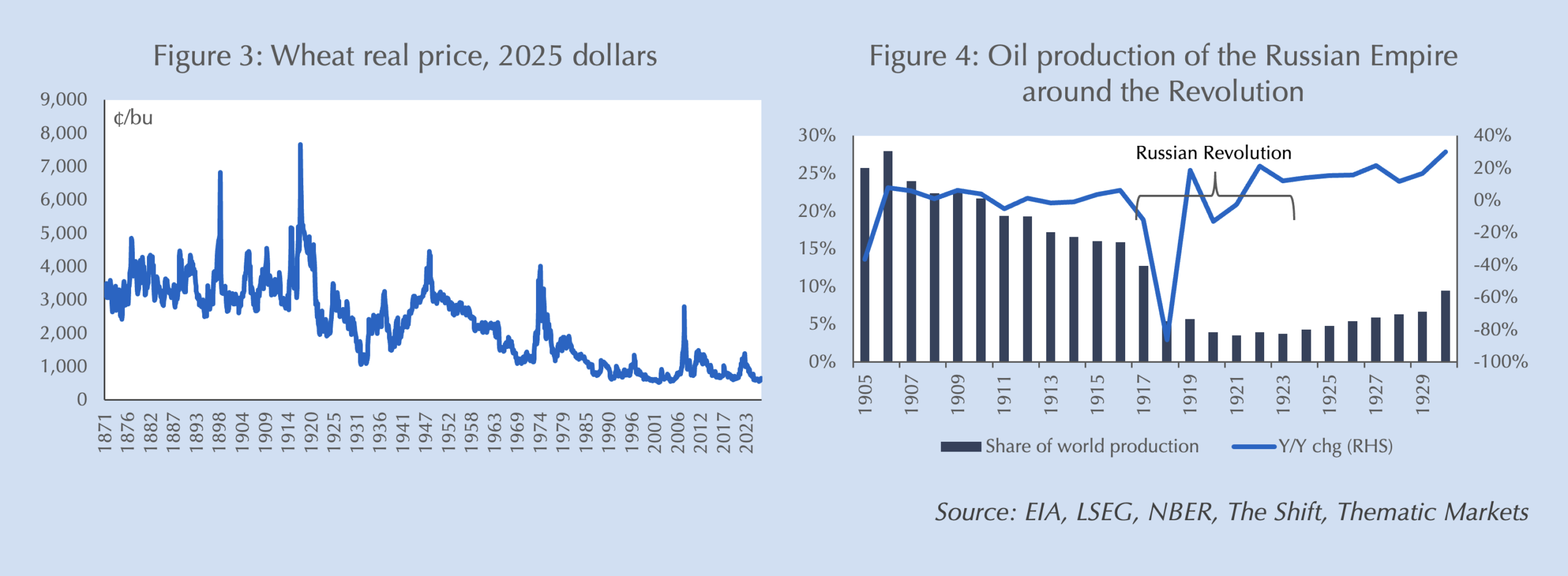

The Iran-Iraq disruption was largely about crude oil, but given the diversification of Gulf economies this is now a much bigger potential shock to oil, gas, fertilizer precursor petrochemicals, sulphur and helium. Yet there was a similar broad and deep shock to global supply over a century ago: the coincidence of the Russian Revolution with World War I. The War and British blockade of Germany had already severely disrupted global supplies of fertilizers as Germany was the world’s largest producer, it also disrupted food and steel production. But the Russian Revolution doubled all these problems, disrupting the world’s largest grain exporter and one of its largest oil producers. Real grain prices surged to their highest level in nearly two centuries of data (Figure 3). Crude oil prices surged to their highest level in half a century as Russian production collapsed from 16% of global supply to 5% in two years (Figure 4). The effects likely would have been far worse had not surging US supply and newly discovered oil in Mexico nearly fully offset the Russian production collapse. Again, the global economy proved resilient: new sources of crude oil came online, the Haber-Bosch process for producing synthetic nitrates was developed to offset blockaded German fertilizer supplies, and bumper American crops helped return food prices to normal, despite the breadth of the supply disruptions.

This time is different

There obviously are big differences in current circumstances from both examples, but there also are important similarities that are missed. For instance, many worry that large fiscal debts make the US and other Western economies uniquely vulnerable to a large energy price shock today. Yet, most European nations faced even larger debts after World War I. Indeed, despite lower debt levels during the Iran-Iraq War, US federal interest outlays were nearly twice their current level as a share of GDP due to the far higher real interest rates of the period. The real differences are in the broader exposure to a slowdown. World War I was followed by a depression, but that also accompanied not only the supply shocks noted, but the demobilization of millions of soldiers, a prolonged steel workers’ strike in the US, then the world’s largest steel maker, and the Spanish influenza. Similarly, the double-dip recessions of 1981 and ’82 were among the more severe post-War US recessions, but the US was then the largest energy importer in the world whereas today it is the world’s largest energy producer and a net exporter. It also is undergoing a massive capex boom driven by Localization, AI and defense, and it is worth noting that California did not participate in the US recessions of 1981 and ’82 due to a similar, localized capex boom during the Reagan defense buildup.

There will be blood

This is not to say that an extended disruption of Gulf exports wouldn’t be painful. It would. But it may not be as painful as anticipated or as widely spread. Every economy has developed more resiliency as a result of the major disruptions of recent years. The US still appears well insulated by a strong capex-driven expansion and the ability to close its energy markets as China has. Europe, Asia and Australia look far more exposed given their energy exposure, slower growth, and debts. The relative picture looks much as it did before the war started, only the global average has changed.

Appendix

| Dates | Event | Description | Commodities |

| 1867 | Grain shortage | Poor harvests in Europe combined with post-Civil War planting disruptions in the US | Wheat and other grains |

| 1898 | Grain shortage | Failed monsoon in India exacerbated by low inventories due to multiple years of poor Russian harvests and surging population growth in Europe | Wheat and other grains |

| 1914–18 | World War I | Major European and colonial war with U.S. involvement; naval blockade and submarine warfare fragmented commodity trade. | Wheat/grains; nitrates/fertilizer feedstocks; coal; metals; oil; shipping |

| 1917 onward | Russian Revolution / Civil War | Collapse of transport and civil war in a major grain exporter. | Wheat and other grains |

| 1919 | Great Steel Strike (U.S.) | Nationwide steel strike after WWI. | Steel |

| 1920–21 | Spanish Influenza | Global pandemic that disrupted labor supply and transport. | Broad labor/logistics shock rather than one dominant bulk commodity |

| 1930s (peak 1934–36) | U.S. Dust Bowl | Drought and soil erosion in the Great Plains sharply reduced crop yields. | Wheat; corn; other grains/livestock feed |

| 1939–45 (esp. 1942+) | World War II | Global war that broke production and trade networks. | Oil; wheat/grains; natural rubber; tin; strategic metals |

| 1951–54 | Abadan crisis | Iranian oil nationalization shut the Abadan complex and choked exports. | Crude oil; refined products/distillates |

| 1952 | U.S. steelworkers’ strike | Basic steel strike during the Korean War period. | Steel |

| 1956 | Suez crisis | British-French-Israeli attack on Egypt led to canal closure and severing of the Syrian pipeline. | Crude oil; refined products into Europe |

| 1959 | U.S. steelworkers’ strike | Longest major postwar steel strike in the U.S. | Steel |

| 1967-71 | Chile copper nationalization / copper turmoil | Nationalization in Chile plus strikes and political turmoil in other producers tightened copper supply. | Copper |

| 1967–75 | Suez Canal closure | Canal stayed closed after the Six-Day War. | Crude oil; products; broader seaborne trade |

| 1972–74 | “Great Grain Robbery” | Poor Soviet harvest led USSR to buy huge volumes of U.S. grain. | Wheat; feed grains/corn |

| 1973 | OPEC Oil Embargo | Arab producers embargoed some buyers and cut output after the Yom Kippur War. | Crude oil; refined products |

| 1978–79 | Iranian Revolution | Strikes and political collapse sharply reduced Iranian oil output. | Crude oil |

| 1980–81 | Iran–Iraq War | War damaged fields, terminals and shipping for two major producers. | Crude oil; products shipping |

| 1990 | Iraqi invasion of Kuwait | Iraq invaded Kuwait; nearly all Iraqi and Kuwaiti output went offline. | Crude oil; refined products |

| 2002–03 | Venezuelan oil strike | National strike and PDVSA stoppage crippled Venezuelan oil operations. | Crude oil; refined products |

| 2005 | Hurricanes Katrina & Rita | Major storms hit the U.S. Gulf of Mexico and Gulf Coast refining system. | Crude oil; natural gas; distillates and gasoline |

| 2007–08 | Food crisis | Poor harvests, low stocks, export bans, hoarding, biofuel diversion and high energy costs drove a global food shock. | Wheat; rice; corn; soy; fertilizers/energy indirectly |

| 2010–12 | Droughts / Russia heat wave & export ban / U.S. drought | Severe heat and drought cut harvests and prompted export restrictions; later U.S. drought hit feed grains and soy. | Wheat; corn; soy |

| 2010 | Rare earths | China curtailed rare-earth exports amid the Japan dispute and broader quota tightening. | Rare earths / critical minerals |

| 2011 | Tōhoku earthquake / Fukushima | Earthquake and tsunami disrupted industrial supply chains and, after the nuclear accident, raised Japanese LNG demand sharply. | LNG / natural gas (demand shock); some oil products; electronics/auto components |

| 2011 | Thailand floods | Flooding of Thai industrial parks disrupted electronics supply chains. | Hard-disk drives; electronics components |

| 2011 | Libyan civil war | Civil war removed high-quality light sweet Libyan crude from the market. | Crude oil |

| 2020 | Covid | Pandemic lockdowns and later rebound created major global supply disruptions. | Broad supply chains; steel and shipping; food processing; energy logistics |

| 2021 | Suez Canal blocked by Ever Given | Grounding of Ever Given blocked the canal for six days. | Containerized trade broadly; some oil/products via route |

| 2022– | Russian invasion of Ukraine | War, sanctions and Black Sea disruption hit energy, food and fertilizer markets. | Crude oil; natural gas/LNG; wheat; corn; sunflower oil; potash/fertilizer; ammonia feedstocks; some metals |

Comments are available to paid subscribers only.