To a hammer, everything looks like a nail

Reading commentary about Kevin Warsh’s nomination for Fed chairman reminds me of the old saying “to a hammer, everything looks like a nail.” Many of the people who – unlike yours truly – failed to predict his nomination are rhetorically pounding him like a nail into their preferred narratives. No, they weren’t wrong that President Trump wants a dove to helm the Fed, simply that Mr. Warsh has only recently revealed himself to be a dove.

It’s politics, i’n’t?

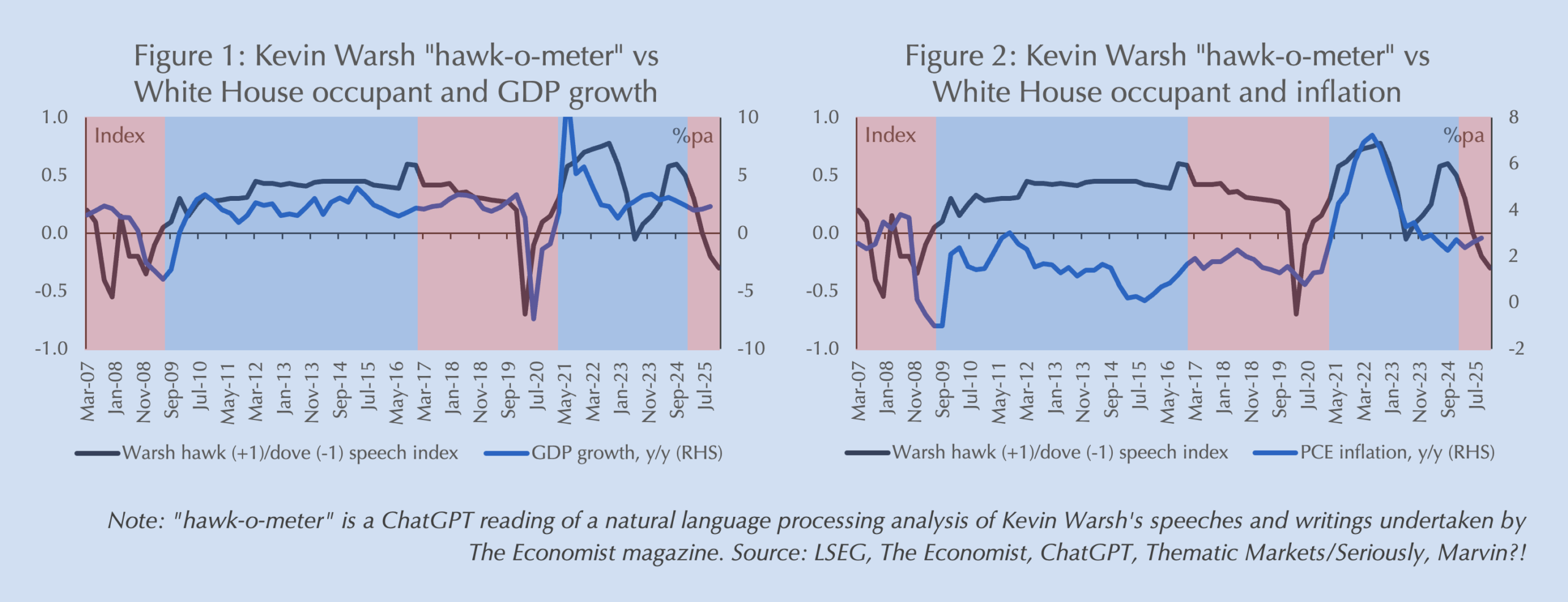

Both Paul Krugman,1[1] whose ability to twist economic theory into a pretzel to fit his politics could shame a German baker, and The Economist2[2] used large language models to construct “hawk-o-meters” from Mr. Warsh’s speeches and writings that neatly (appears) to fit changes in White House occupants. That is until you compare the indices to economic variables like GDP growth (Figure 1) or inflation (Figure 2) that seem to much better explain Mr. Warsh’s vacillations than moving vans coming and going from 1600 Pennsylvania Avenue.3[3]

“Look! In the sky! It’s a hawk! No, it’s a dove!”

Both Mr. Krugman and The Economist are paid to feed their readers’ biases, not make accurate predictions. But the same can’t be said of many market participants who share their suspicions that Mr. Warsh’s rhetorical shift in favor of lower rates since President Trump was elected has something to do with politics. As I explain below, while I am convinced that Mr. Warsh is a hawk – which I believe, contrary to the consensus, is one of the reasons he was picked – I also do think that politics helps explain his change in tone. Yet much of the confusion over what Mr. Warsh stands for and what to expect from him stems from a far deeper, far more consequential cleft between him and what markets have become accustomed to from central banks.

Philosophy over ornithology

A recent post by former Fed and Biden Administration economist, Claudia Sahm,4[4] rightly notes that “hawk” and “dove” are “simplistic labels” that miss the defining feature of Mr. Warsh: his deep-seated philosophical rejection of the current central banking consensus (of which Ms. Sahm is a member). Ms. Sahm digs into the transcript of the November 2010 Federal Open Market Committee (FOMC) meeting to illustrate how out-of-line Mr. Warsh was from the emergent consensus that would dominate monetary policy for the next 16 years.5[5] At that consequential meeting, with the Fed funds rate already at its effective floor, for the first time, the Committee voted to expand the Fed’s balance sheet a as substitute for policy rate cuts – “Quantitative Easing” (QE) –rather than as the balance sheet had traditionally been used, including in 2008-‘09, to fulfill the Fed’s “lender-of-last-resort” duty. Then Governor Warsh strongly argued against the move, though in deference to then Chairman Ben Bernanke, voted with the Committee to approve it.

Stark contrasts

Ms. Sahm liberally quotes Mr. Warsh’s unvoted dissent to compare him with Committee members like Janet Yellen, whom she describes as “what central casting for a Fed Chair looks like.” Her comparison yields a stark contrast. Then Vice Chair Yellen is data driven, relies on models and, most importantly, is happy to push the boundaries of monetary policy without restraint to achieve the Fed’s full employment mandate. In contrast, Mr. Warsh worries that models may fail to capture nonlinearities in the economy, and is skeptical of the risk/reward of pursuing unproven policies that may both overstep the Fed’s mandate and invite adverse long-run political consequences.

Seeking regime change

That fundamental contrast in central bank philosophy continues to define Mr. Warsh and his views. He describes the current Fed as “radically different from the central bank [he] joined in 2006” and he blames the philosophical shift for “the greatest mistake in macroeconomic policy in 45 years, that divided the country, [and] caused a surge in inflation.”6[6] While he deferred to Chairman Bernanke out of respect in 2010 (resigning a few months later), he makes clear that he intends a “regime change” if confirmed as Chairman: “It’s not just about a person, it’s about an approach to economics.”7[7]

Back to the future

What would a new Warsh regime look like? A lot like the old regime…before quantitative easing. From his dissenting arguments in November 2020 through his most recent public speeches, Mr. Warsh has been remarkably consistent in his philosophical touch stones:8[8]

- Epistemic humility: Recognizing the limits of models, our understanding of the events that led to our present, and our ability to forecast the future.

- Respect the Fed’s legal mandate: stay within the boundaries defined my Congress, or risk political backlash.

- Operate within a pre-defined framework: Constant communication and forward guidance undermine credibility whenever you are wrong; defining a reaction function obviates the need.

- Accountability: Independence does not mean beyond reproach and failure to take responsibility for policy invites politicization.

Theory and practice

In practice, that means a much smaller balance sheet, less frequent communication that prioritizes framework over forecasts and commitments, more focused, measurable objectives that clearly align with its legislated mandate, and more “art” than “scientific” certainty. As an economist who grew up in the Greenspan Fed, I have a lot of sympathy for Mr. Warsh’s philosophical approach. As long-time readers will know, in the last two decades I think the Fed has relied too much on faulty models that have led to historically bad outcomes, have undermined its credibility, and arguably both politicized it and brought it into fiscal dominance already.

It’s politics i’n’t?

But how do we explain Mr. Warsh’s rhetorical embrace of lower interest rates since President Trump’s election? Of course, politics likely plays a role, and as long as it isn’t the dominant factor driving the change, political savvy probably is a good thing. Mr. Warsh has never backed away from his defense of price stability and indeed has called it the Fed’s “armor” to defend its independence.9[9] But a successful Fed chairman must play politics to keep the Fed independent. Alan Greenspan, one of the Fed’s most politically astute chairmen, regularly tilted his answers to questions in his semi-annual Congressional testimony towards the party in power: favoring tax cuts in Republican majorities and new spending when the Democrats were in power. This was how he kept the Fed out of the firing line and maintain its latitude to conduct independent monetary policy. Even the legendary Paul Volcker ducked political fire for hiking Fed funds to 20% by claiming the Fed was targeting the money supply rather than interest rates. Firm oaks fall in political winds; bendable reeds stand tall when the winds pass.

The case for lower rates

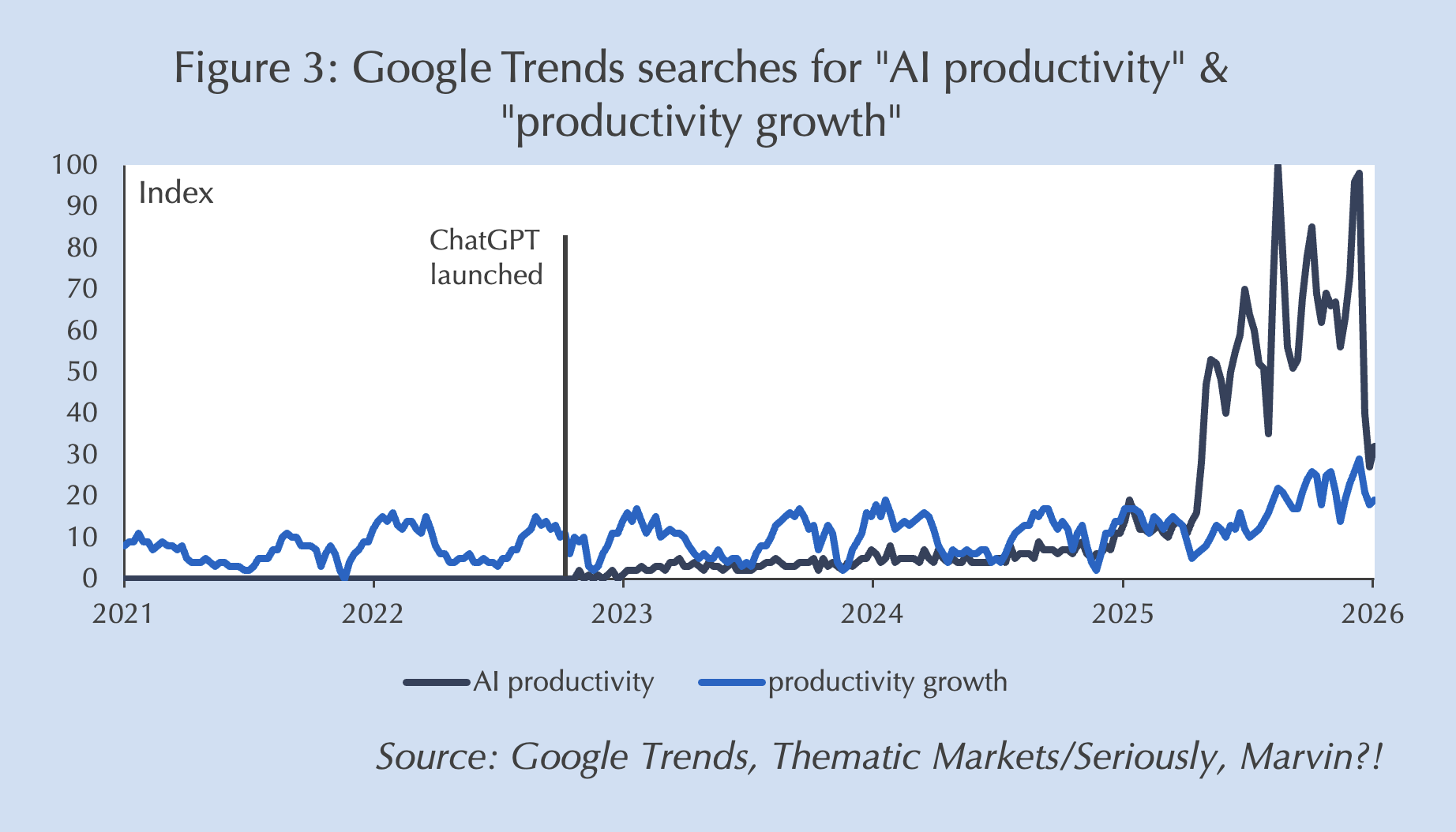

While the necessary evils of politics may have nudged Mr. Warsh towards lower rates, he has articulated a clear, defensible economic framework that would permit lower (policy) interest rates amid price stability. First, he expects the balance-sheet contraction he has promised to provide sufficient tightening of financial conditions to deliver price stability even with lower policy rates. Second, he anticipates a tailwind of falling inflation to come from rising productivity delivered by artificial intelligence. Even the timing of his conversion may be defensible. A pre-requisite for the balance-sheet effects he posits would be the appointment of a chairman like himself; and as shown by Google search activity (Figure 3), he doesn’t seem to have been alone in suddenly noticing the potential for AI-led productivity growth midway through 2025.

For the record, I expect him to be wrong about inflation on both counts, hence my expectations for a policy-rate-led bear flattening of the US yield curve in the second half. I have long maintained that both QE and QT (Quantitative Tightening, the reversal of QE) have far less effect on bond yields than the Fed and most in markets assume. Further, in my framework Being is believing effects are more important to the path of inflation than real relative price effects. But that doesn’t mean Mr. Warsh’s views are either unjustified or inconsistent with his philosophy of monetary policy as defined above.

Free the Fed now!

What about Mr. Warsh’s reported calls for a “Fed-Treasury Accord?” This results from misunderstandings of Mr. Warsh’s views on QE and of what the Fed-Treasury Accord of 1951 was. Many people confuse the Accord with the Fed’s loss of independence under pressure from the Treasury to cap its borrowing costs. It was the exact opposite: after being forced to cap interest rates through World War II and its aftermath, the Accord freed the Fed to pursue independent policy. In that context, if your starting point is that the Bernanke-Yellen-Powell Fed enslaved itself in fiscal dominance through QE, which is how Mr. Warsh (and many in the Trump Administration) view it, then unwinding QE requires a Fed-Treasury Accord to return the Fed to independence. This is actually quite sensible for market stability: if the Fed intends to shed a significant portion of its $4¼ trillion in Treasury holdings as the Treasury is selling $1½ trillion of new issuance per year, some coordination likely is necessary to prevent unintended volatility or distortions in sectors of the curve.

The final weighing

As noted above, I have much sympathy for Kevin Warsh’s broad philosophy of monetary policy, even as I doubt his justifications for lower rates amid a powerful, Localization-led capex boom. I also have questions about his understanding of economics. He is trained as a lawyer – a worrying sign after Jerome Powell – and gaps in his understanding of monetary theory are clear in some of his public discourse. But what I do not doubt is that he is at heart a hawk who will hike rates without hesitation if the Fed’s mandate for price stability is threatened. Playing politics to get the seat is different from tarnishing your reputation through poor execution of your duties. Mr. Warsh is a well respected, independently wealthy man who already has resigned from the Federal Reserve Board once over his philosophical differences. When inflation comes, as I expect it will, he will hike rates as aggressively as needed to bring it to heel. Even Claudia Sahm, despite her clear misgivings about him, credits him with the ability to admit error and change his view as the conditions demand.

Comments are available to paid subscribers only.