Fair bets

Suppose that I show you two urns, each filled with 100 marbles. The first urn has 50 red marbles and 50 black. The second urn also has 100 marbles of red and black, but their proportions are unknown. If I offered you the chance to blindly pull a marble out of either urn for 50¢ and agreed to pay you $1 if the marble is red, which urn would you choose? Despite the fact that both bets have the same expected value, 50¢ — there’s just as much chance the second urn has 100 red marbles as zero, one, 99, or 50 — few people opt for the second urn in experiments. This is known as the Ellsberg paradox and is often used to illustrate the difference between risk and Uncertainty.1[1] That difference is critical in finance. It also explains why quantitative forecast models must be used with caution, why prediction markets are terrible at forecasting some events, and why — despite the insistence of some FOMC members — inflation swaps are not inflation expectations.

Uncertainty with a K: Knightian or Keynesian

The distinction between between risk and Uncertainty is typically associated with the American economist Frank Knight who proposed it in the late 1910s.2[2] Knight categorised risk as quantifiable or non-quantifiable, the latter of which he called “uncertainty,” hence why it is sometime called “Knightian uncertainty.” In the Ellsberg paradox, both bets risk the loss of 50¢ but the first urn offers a quantifiable probability of loss, 0.5, while the second urn has a nonquantifiable probabilities of gain or loss. The British economist John Maynard Keynes proposed the same concept (even earlier) in a framework that I prefer, splitting risk into three buckets: objective, subjective and uncertainty.3[3] The last is defined as Knight did, nonquantifiable risks, but Keynes divides quantitative risks in two: clearly defined probabilities like the chance of being dealt an ace in blackjack (objective); and subjective informed guesses like the chance of afternoon rain in London (subjective).

Risk versus Uncertainty

While it is common for laypeople to use the words risk and uncertainty interchangeably, even many economists and finance professionals learned in Knightian uncertainty, fail to grasp the practical difference. Hence the motivation for this note. At last week’s Hoover Institution conference, an esteemed, extremely intelligent and knowledgeable economist insisted to me that inflation swaps not only are inflation expectations, but are the most informative ones “because money is on the line.” I’ve had similar arguments with very successful hedge fund managers who are adamant that betting markets provide the best prediction for any question. They’re not wholly wrong, but they’re not right either. The distinction lies in the Ellsberg paradox.

Increasing Uncertainty

Suppose that instead of letting you choose which urn you pull a marble from, your only option is to purchase the chance to draw from both urns and be paid $1 for each red ball you retrieved. Rather than $1 (50¢ per urn), you might only want to pay 95¢ or even 90¢ to compensate for the Uncertainty of the second urn. If we bundled draws from 100 urns together and varied the number with unknown proportions of red marbles, the price that someone would be willing to pay would vary inversely it the number of uncertain urns: perhaps as high as $49.95 if only one of 100 urns had an unknown proportion, or as low as $35 if all 100 were of unknown mixture. That’s because risk aversion is increasing in Uncertainty: people don’t like risks they can’t put a number on.

Mixed chances

In the real world, risks often are a mix of objective, subjective and uncertain risks. Consider US nonfarm payrolls (NFP), the most anticipated, forecasted and market-moving data release on the planet. We have 88 years of monthly data (1,104 observations), oodles of historic correlates, and a rapidly expanding set of “big data” indicators that aid hundreds of professional economists in forecasting it. Thus, NFP — and the market movements associated with the release — are mostly objective risks. But what if there is severe flooding in the Midwest or a major strike that disrupts employment across several states? Based on the few historic examples and subtle difference across each, an objective estimate of their effects on NFPs is no longer possible. When Covid hit there were no relevant comparisons. Hence, even NFP, this most predictable of surveys, is a mix of quantifiable risk and Uncertainty, like the mix of urns described above.

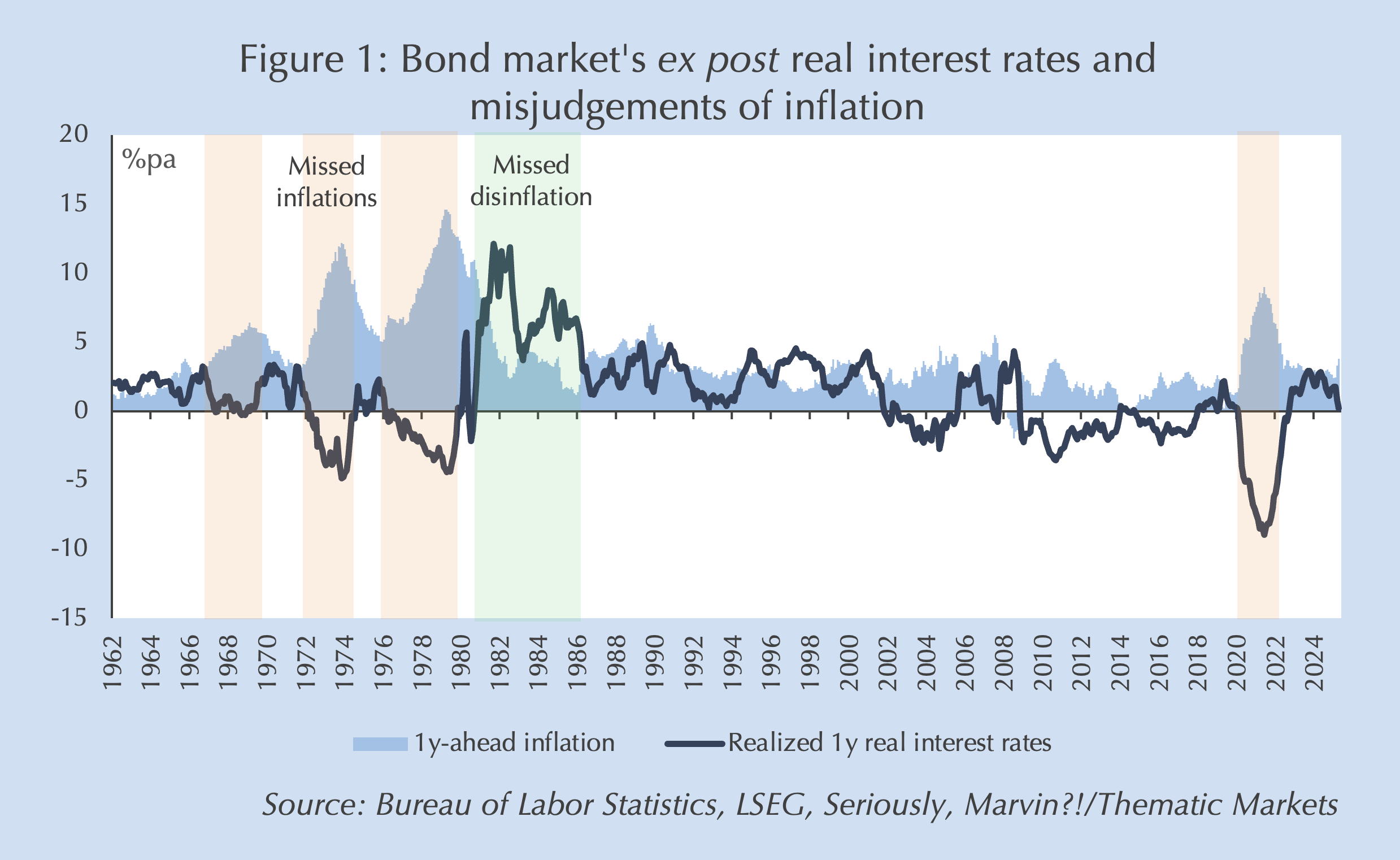

Bond traders know where their bread is buttered

The same applies to market-based measures of future inflation, like inflation swaps or “breakevens,” the yield difference between nominal Treasury securities and inflation protected TIPS. Unlike consumer inflation expectations that shape inflation because they are part of the price formation process, these market metrics are forecasts of inflation. Because “money is on the line,” they tend to be very good forecasts when inflation expectations are stable. During normal times, forecasting models based on lagged inflation, energy and food prices, rents, and labor market data allow quantification of the objective risks embedded in inflation. But when consumer inflation expectations shift — as they did in the 1970s (rising), 1980s (falling) and during Covid (rising) — bond markets have done a terrible job forecasting future inflation. Not sometimes, not most of the time, but every time as illustrated by ex post real interest rates (Figure 1). That’s because bond traders, just as participants in the Ellsberg paradox experiments, prefer to focus on objective risks they can reliably estimate and ignore the nonlinear, nonquantifiable risks that they can’t, like changes in consumers’ price expectations.

Betting on the truth

Betting markets face the same problem. Where plenty of data exist to form objective probabilities — whether the New York Knicks will beat the Cleveland Cavaliers this weekend, which company will have the largest market cap by month end, whether Democrats or Republicans will win the US House of Representatives in November’s midterm election — betting markets generally integrate all the available information and provide the best forecasts. But betting markets do poorly at forecasting unusual or novel situations, e.g. picking winners when a new political movement forms. Betting markets gave President Trump just a 13% chance of winning the 2016 election, 33% chance in 2020 (where he narrowly lost), and a 55% chance in 2024 when he won the popular vote and easily won the Electoral College.4[4] Betting markets also assigned only a 21% probability that Venezuelan dictator Nicholas Maduro would be removed from power by 31 January 2026 despite a massive build-up of US forces beforehand (and even with alleged insider trading pushing up the odds).5[5] Or, consider that there was a complete absence of betting opportunities on a worldwide lockdown in 2020 as such an event wasn’t even considered a possibility.

Objective signals

The underlying issue is that markets both prefer and are best at forecasting objective risks, hence tend to eschew and thus perform less well managing risks with deeply subjective or unknown. In a world of mixed risks — objective, subjective and uncertain — markets will focus on pricing the objective risks they understand, hence why inflation swaps do very well at pricing in every forecastable wiggle in inflation due to oil prices or avian-flu-affected egg prices, but perform miserably in capturing shifts in consumers’ expectations of (and thus willingness to accept) inflation. Or, why the stock market focuses on surprisingly good earnings growth numbers while seemingly “ignoring” a war that could generate the largest disruption of energy supplies in history: earnings are objective; war is Uncertainty.

Rising Uncertainty tilts the signal to “noise” ratio

But what happens as the world becomes more uncertain? I.e. what if Uncertainty’s share of total risk increases? In my example of 100 urns, this is akin to the share of unknown-proportion urns increasing, potentially randomly. If 99 out of 100 urns have (known) objective risks, the price of the bet likely will accurately reflect the objective probability of red marbles drawn. But if 99 urns have unknown proportion — or worse, an unknown share of the 100 urns have unknown marble proportions — markets will do a poorer job assessing the probability of red marbles drawn. This is the world we now live in and why Uncertainty is one of my ongoing Themes: rapid technological progress is upending global trade and production through Localization, Global entropy’s evolution to Global bifurcation is rewriting the “rules-based order,” while the Politics of Rage does the same for national politics, and, of course, Being is believing is shifting inflation’s trajectory unpredictably.

Risk premia up (with caveats)

As Uncertainty rises as a share of total risk, risk premia should expand, just as the price of the bet on 100 urn draws would be expected to fall as the share of urns with unknown proportions of marbles increases. Yet, expectation for rising risk premia has to be balanced against the potential for objective risks to offset them. For instance, the equity risk premium has fallen over the last few years, but that has been supported by an objective rise in positive earnings surprises. Absent such strong earnings growth, equity risk premia may well have risen. Similarly, narratives also can (temporarily) dominate Uncertainty. Objectively, US fiscal risks have grown steadily over the last two decades, yet term premia on US Treasuries fell on the false narrative of “secular stagnation” and the Illusory omnipotence of central banks. Only recently have US term premia begun to rise (their relative rise versus even riskier European sovereign bonds reflects yet another false narrative: de-dollarization).

Quant alpha down

Another implication of rising Uncertainty is declining “quant” alpha (excess returns to quantitative finance strategies). That trend is already well underway due to the increasing availability of digitized data and falling cost of quantitative analysis (“Hey, Claude, can you please program up that multivariate Kalman filter for me?”). When anyone can build an analytical model of nearly any quantifiable risk, it can’t be a source of alpha. But as Uncertainty rises as a share of total risk — and potential for excess return — the available alpha for quantitative methods must fall. Indeed, this was Frank Knight’s point in Risk, Uncertainty and Profit, his book describing Uncertainty as nonquantifiable risk.6[6] True excess returns should only be available for risks that dissuade most other investors due to the inability to quantify them. (See my related points for political and business leadership.)

Subjective versus uncertain risks

One of the reasons I prefer Keynes’ tripartite formulation of risk to Knight’s is the grey zone of “subjective” risks. It’s a grey zone because how do we differentiate risks that are truly nonquantifiable — i.e. you can’t even make a reasoned guess at the probability — from those that merely don’t lend themselves to statistical analysis? Is the probability that consumer inflation expectations shift really nonquantifiable? I correctly forecast their 2021 jump,7[7] partial stabilization in 2023, and recent rebound. What about populism? I correctly forecast Brexit, Donald Trump’s 2016 election, narrower-than-expected loss in 2020 and popular-vote win and coattails in 2024.8[8] What about the rise in US productivity we’re now seeing? Again, I’ve been highlighting it for years before it became clearer in the data.9[9] In each of these cases, I would argue that the risks were subjective rather than truly nonquantifiable Uncertainty. A combination of theory-led economic analysis and careful examination of the available data allowed me to make (correct) subjective judgements on their probability.

Managing uncertainty

But there are risks that are simply unquantifiable. For instance, what is the likelihood that a resumption of hostilities in the Persian Gulf takes out much of the region’s oil production capacity for an extended period? Or that a peaceful solution opens the Gulf before the end of June? We can make guesses at both probabilities, but if we’re honest with ourselves the range of reasonable guesses is too wide to be useful in linear (non-derivative) investment decisions. Yet, even true Uncertainty is manageable with appropriate methods and tools. As I’ve shown in previous research, structured scenario analysis can be used to construct derivative portfolios that will hedge most unexpected risks.10[10] There is a similar process for long-only, non-derivative portfolios, but the required return sacrifice is greater.

The first step is admitting there’s a problem

The critical point is that successfully navigating a world of mixed risks requires you to know which are objective, which can be subjectively analyzed, and which are nonforecastable. Knowing — and admitting — the difference is the first step.

Comments are available to paid subscribers only.