Today I am giving a presentation on “Risks, Challenges and Opportunities” at the Hoover Institution Monetary Policy Conference. This piece, focused on the risks to Fed independence with some insights into my forecasting method, is based on my remarks.

My primary message is that the risks to Fed independence are largely of its own making and that as an institution it is in desperate need of root-to-branch reform. My critique is blunt and unforgiving because I care about the Fed. I spent my formative years as young economist at the Fed, retain many close friends throughout the system, and am thankful for all that I learned there.

A running subtext of my talk — the importance of traditional economic analysis in a time of increasing uncertainty, i.e. non-quantifiable risk — is illustrated by an anecdote from my early days at Fed as a newly minted UCSD PhD. The eminent economic historian, Michael Bordo, was a visiting scholar at the Fed and came into my office for a chat. He took one look at my bookshelf and said, “That’s a lotta math and econometrics books. Don’t you think economic history and theory should be part of your analysis?” It’s taken me three decades, but hopefully, I can properly answer him today.

At Thematic Markets, I’m in the forecasting business. My clients — hedge funds, global banks, asset managers, and multinationals — pay me to identify the major trends affecting the global economy and markets before anyone else, something I’ve done more consistently than most over the last quarter century.

My technique flows from Professor Bordo’s advice and the economic theory I learned from my mentor, Valerie Ramey. I use their tools to identify the “Themes” underlying the global political economy and make my forecasts based on their expected evolution. But I always keep in mind one of the lessons that Nobel laureate econometrician Clive Granger taught me: “If your model doesn’t forecast, it’s wrong.”

Today, I see four major themes in the global economy and markets: Localization, Being is believing, Global entropy, and what I’ve called the Politics of Rage. Their collective effects have raised US potential growth, the marginal product of capital, inflation pressures, and are leading to increasing decentralization of finance and the diminution of globalized supply chains in manufacturing.

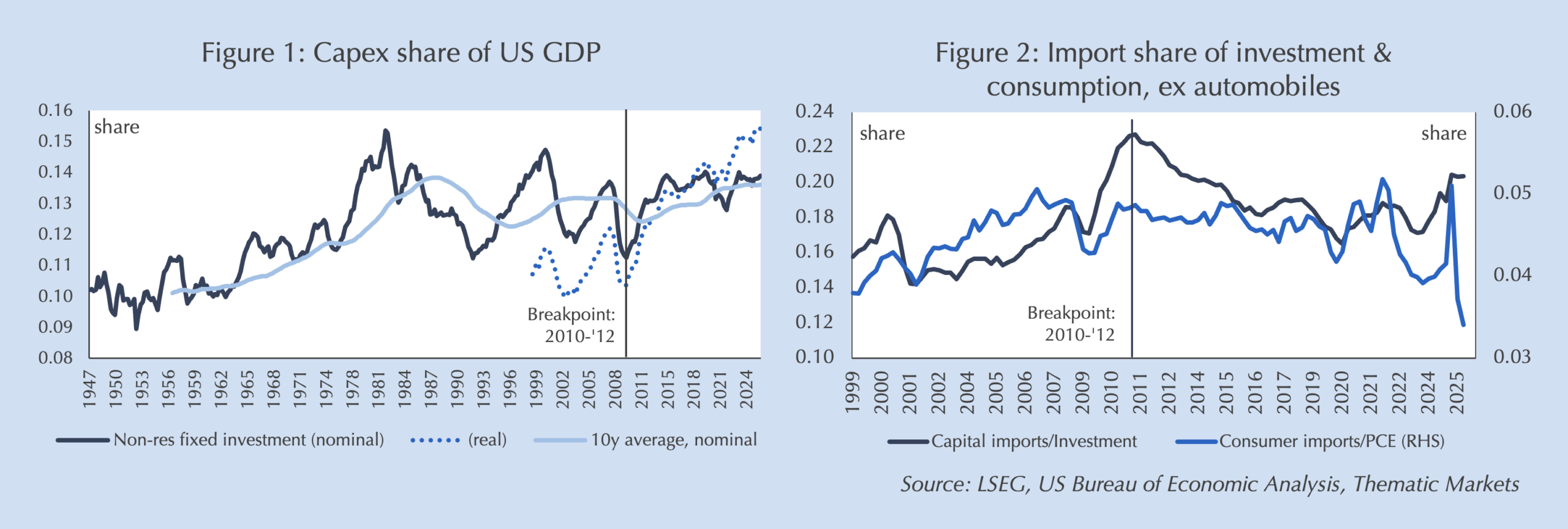

Let’s start with Localization. 2012 was an unheralded but important breakpoint in the global economy: Cross-border investment that had trended steadily from advanced economies to emerging economies for decades, reversed with the US being the primary beneficiary, coinciding with the largest investment boom in post-War US history when cumulated (Figure 1). At the same time, the import share of US GDP peaked after five decades of trending higher and has fallen steadily since. This is true of both imports as a share of capex and consumption (Figure 2), though less steady.

Anecdotal evidence gleaned from companies, private equity firms, and my analysis suggests the culprit is technology: when automation allows you to integrate production near your highest-value customers more cheaply than outsourced labor, globalization no longer makes sense.

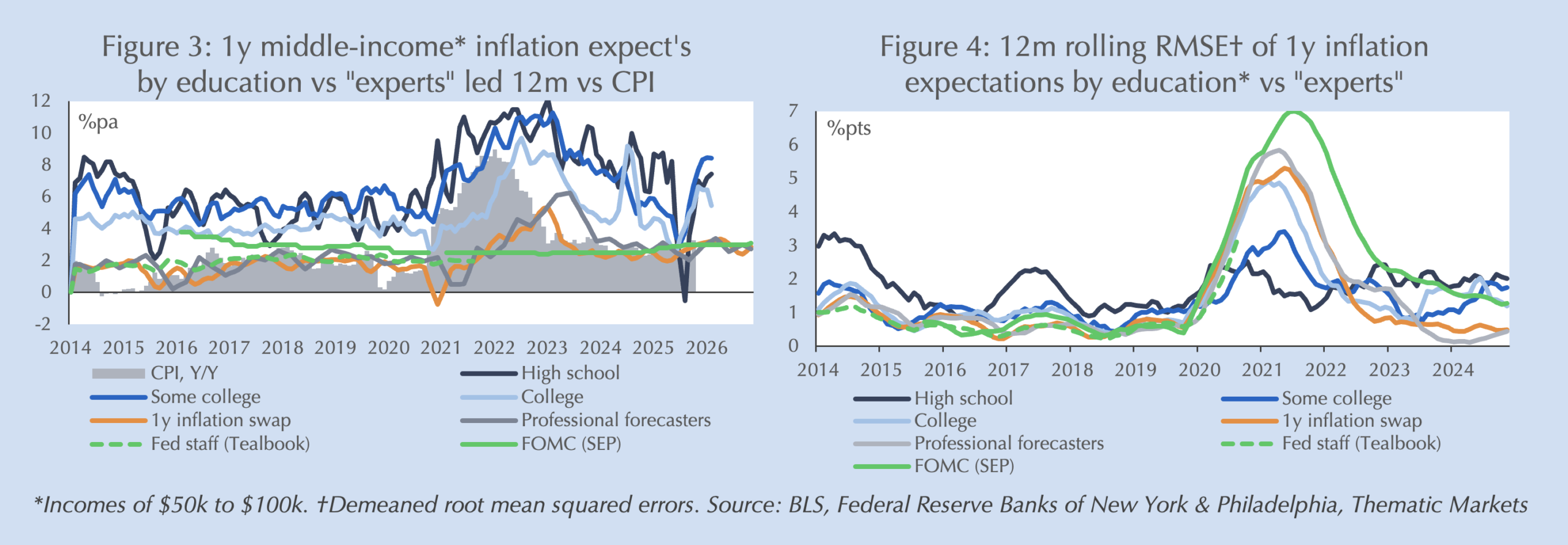

Being is believing is my layman speak for self-fulfilling expectations. Economic theory has long accepted the role of expectations in price formation: if consumers believe inflation is rising they more willingly accept rising prices, enabling faster inflation. But quantifying this, especially when inflation expectations are stable, has been a challenge. As a result, most econometric models neglect or de-emphasize them, and for many years that worked: econometricians’ fancy math bested the expectations of the noisy rabble’s expectations and everyone but bond traders (Figures 3 and 4).

Then Covid hit and inflation forecasting was turned on its head. The econometricians, even bond markets, got it all wrong, but consumers, in a perfect reverse order of education, nailed it. What happened? The Fed’s “Flexible Average Inflation Targeting” successfully unhinged inflation expectations and the people closest to prices didn’t just see it first, they created it with their expectations. Professional economists and bond traders only cottoned on after the fact and the Fed couldn’t even manage to acknowledge what their “lying eyes” were telling them.

There is an important secondary message here. I know a lot of bond traders and I’m not sure that any can tell you the price of a gallon of milk. To suggest that their pricing of future inflation is representative of consumer price expectations, given their failure to predict every instance of expectations de-anchoring from the 1970s through Covid, reflects a profound ignorance of finance, economic history and theory. The consumers that form prices in our economy struggle to balance their budgets. And by the way, they vote.

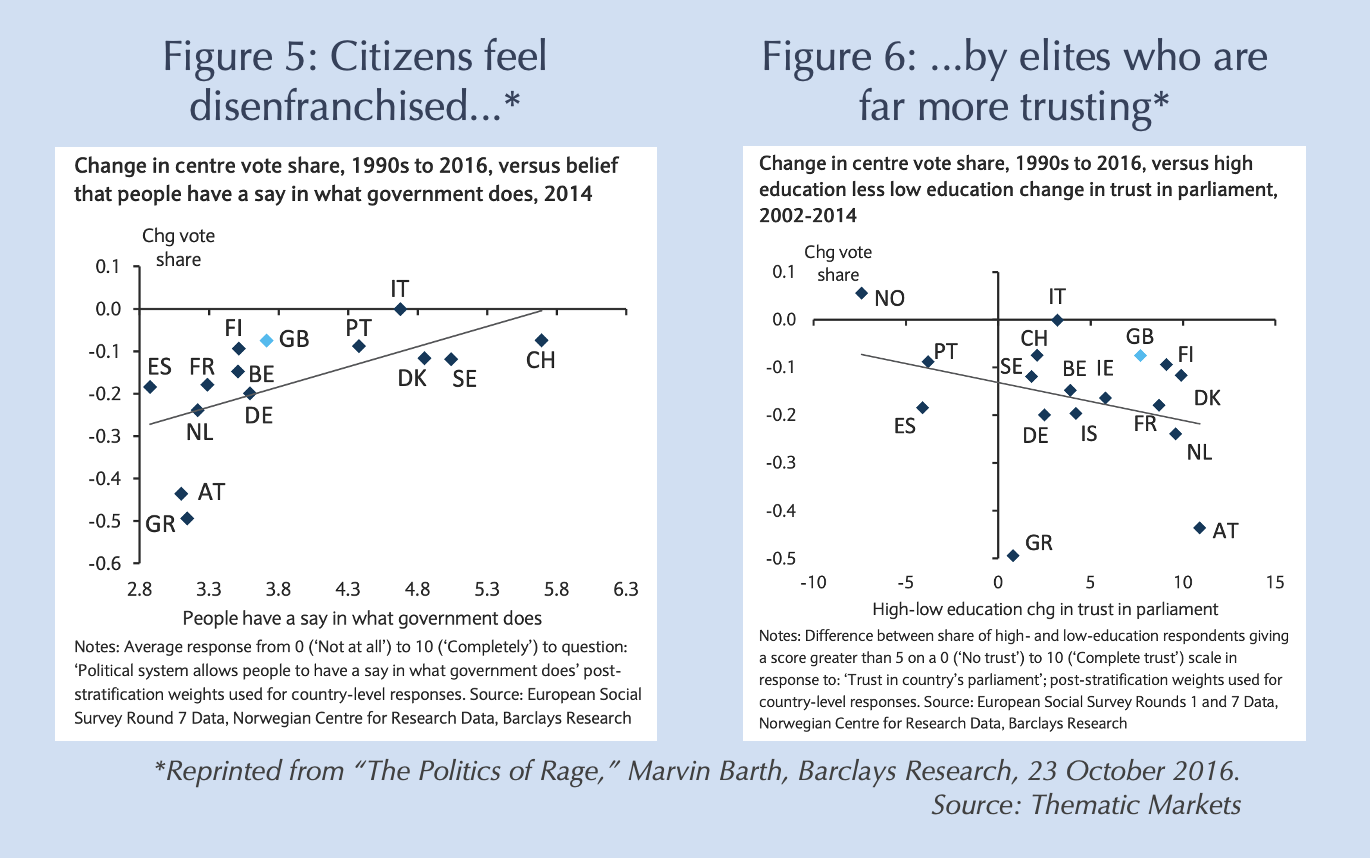

Failures of accountability like this have been one of the key drivers of populist anger. In The Politics of Rage, a report I wrote at decade ago, I found that the primary driver of populism is average citizens’ perception that they’ve been disenfranchised by elites’ pursuit of their own interests at the expense of the masses (Figures 5 and 6).

Contrary to popular opinion, this is about trust, not education. David Shor, chief data scientist for President Obama’s 2012 campaign, has shown that trust, far more than education, predicted votes for President Trump.1[1] Anthropologist Heidi Larson has amply demonstrated that perceived loss of control rather than eduction or lack of knowledge are the primary drivers of both vaccine hesitancy and conspiracy theories.2[2]

If you take one thing today, let it be this: You are not going to “educate” populism away or convince populists that you are acting in their best interests. They don’t trust you. And after a long sequence of “experts’” policy errors whose cost have largely fallen on the masses, who can blame them?

American populism has a long tradition and peculiar characteristics. In temperament, governing philosophy and policies, right down to legitimized graft, President Trump is merely the second coming of Andrew Jackson, the so-called “First Populist.” It only feels unfamiliar because we’re just ending a century-long period of Federalist ascendancy. There are two facets of Jacksonian populism that are particularly relevant to my topic here: hostility towards centralization of finance or government involvement in it, and a strong national defense, free of foreign entanglements and focused on “offshore balancing” in American interests.

The first is of obvious relevance to the Fed: don’t forget that Andrew Jackson successfully killed the Second Bank of the United States. The second is a predictable response to Global entropy, the collapse of the post-War global order that began almost three decades ago.

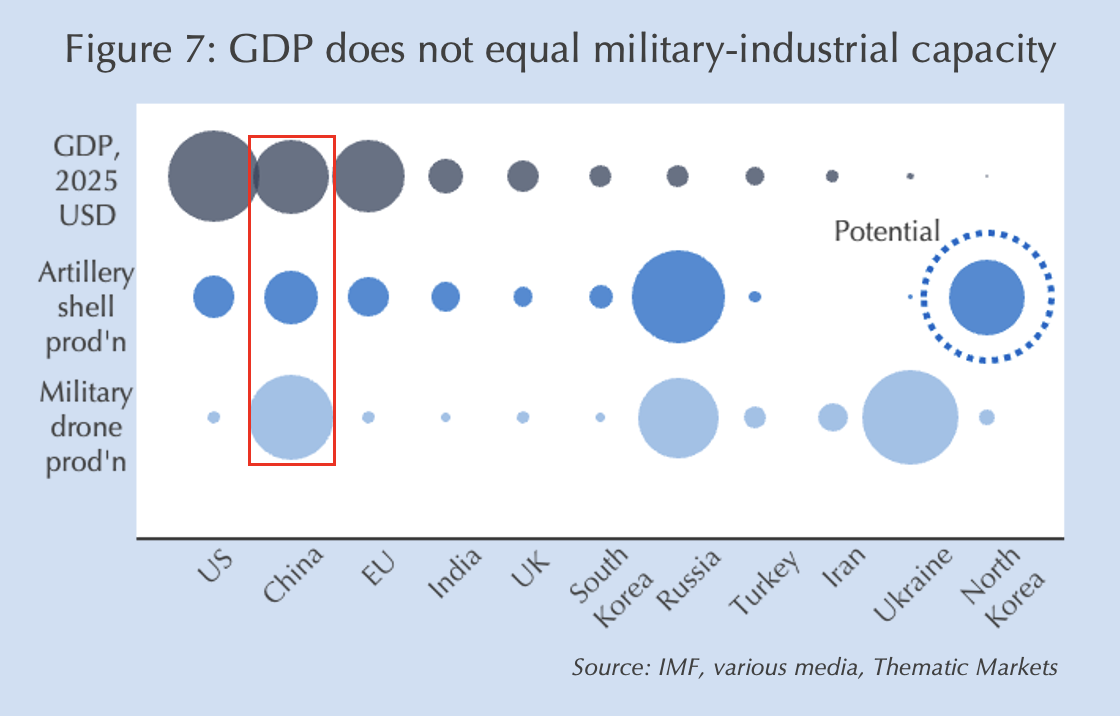

Through arrogance, idealism and short-sightedness, the West forgot that power — and the ability to police the world order — comes from capacity to manufacture guns, 155mm artillery shells, and now drones, not GDP (Figure 7).

But China didn’t. In fact, both Chinese policymakers’ “genius” in raising a billion people out of poverty and supposed “failures” of overcapacity reflected an intentional policy to shape the future battle space by tipping technological leadership and military-industrial capacity in China’s favor through massive industrial subsidies. The contours of this strategy were outlined in a 1997 book by two People’s Liberation Army senior colonels called “Unrestricted Warfare.”

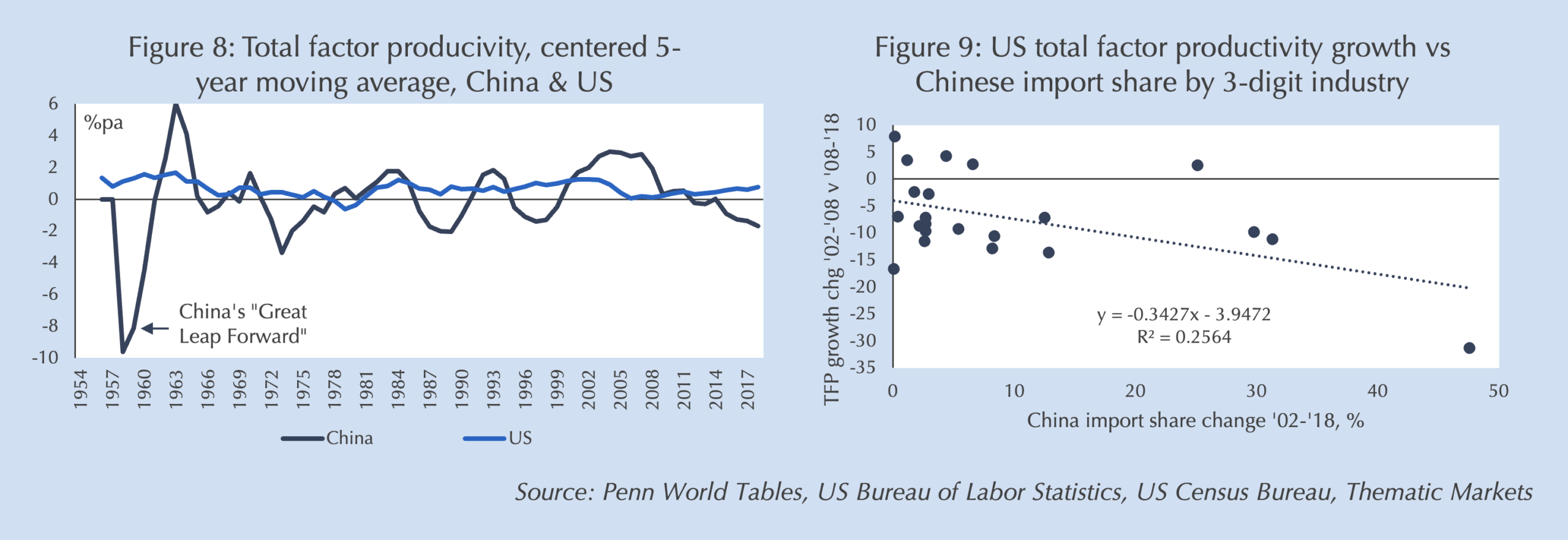

In my research, I’ve shown at a three-digit industry level that Chinese import penetration directly reduced total-factor productivity in US manufacturing by undermining “learning by doing” as American firms were forced into “run-off” mode (Figure 9). This isn’t because Chinese factories are more economically efficient: Chinese total factor productivity growth has been negative for more than a decade (Figure 8).

Belatedly, the US has awakened to the threat. This is what was behind the Biden Administration’s industrial subsidies and the Trump Administration’s tariff wall.

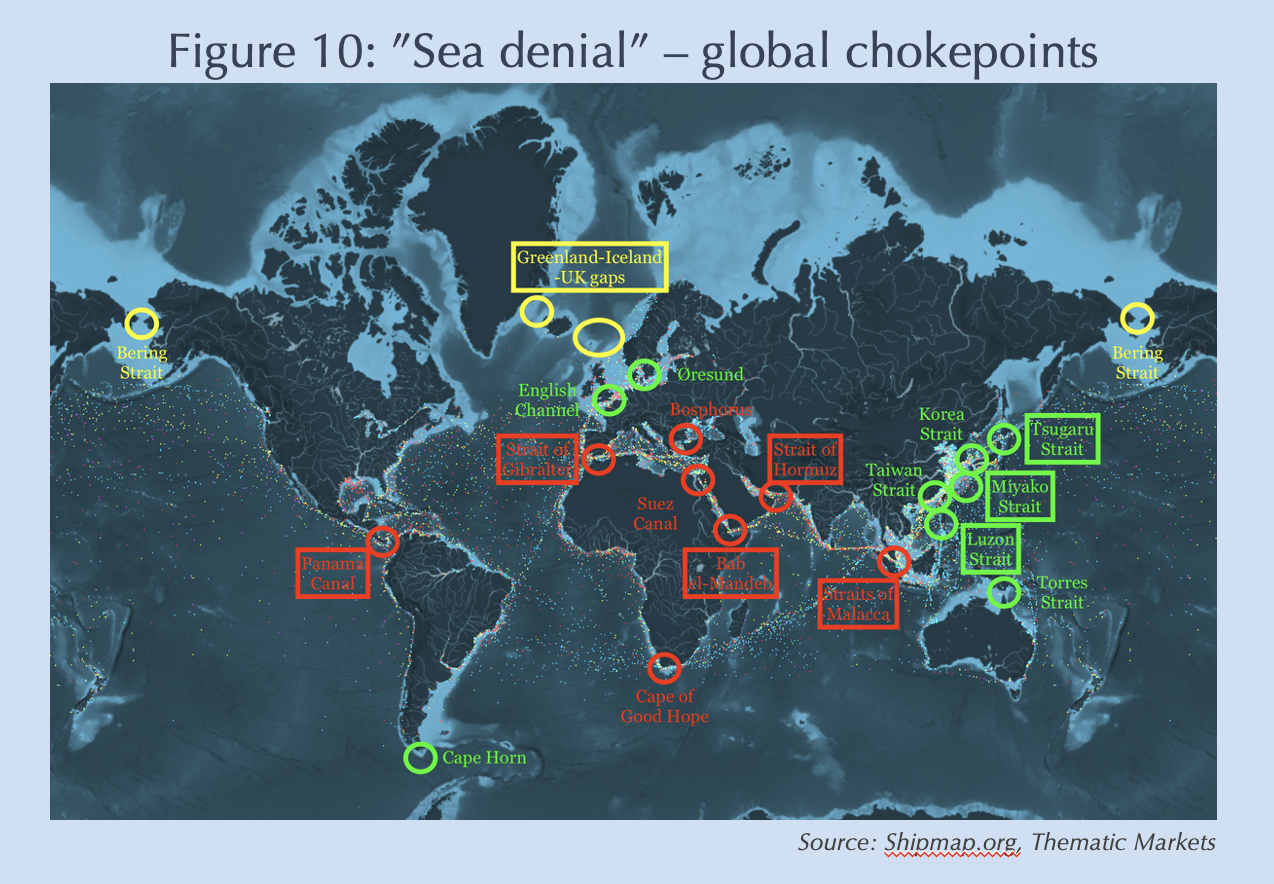

But tariffs are only part of the Trump Administration’s response. Realizing that rebuilding industrial capacity will take a decade or more and that the PLA Navy will outclass the US Navy by tonnage, technological sophistication and weaponry within a few years, the US military has shifted to a hybrid warfare strategy of “sea denial”: i.e. China may deny the US control of the seas, but by seizing the world’s major chokepoints, the US can deny China control, too.3[3] Every “boxed” chokepoint shown on Figure 10 is one that the US has moved to control in the last year. Rising resource nationalism and transport costs are the result.

What does this all mean?

First, Localization is driving potential growth, the marginal product of capital, and neutral real interest rates higher, while compressing imports. This is clear in both the economic data and in financial market prices over the last decade.

Being is believing is driving inflation persistence, despite the Fed’s denials.

Global entropy is simultaneously reinforcing Localization, shifting out the aggregate demand curve by increasing redundancy and defense expenditures, and shifting the aggregate supply curve inwards by raising costs.

Finally, the Politics of Rage is, well, raging. As seen in the GENIUS and Clarity Acts, it is advancing decentralized finance which I expect my co-panelists may tackle in detail. It also is pushing for greater accountability from bureaucracies.

Let me briefly illustrate with two current examples how this Thematic, or “narrative,” method of forecasting better meets Clive Granger’s test than time series models.

Had you relied on standard trade models and generic studies of tariffs — which notably are of small, developing economies, not a large, mostly closed economy on the technology frontier — you would have predicted, as most economists did, that the broad, large increase in US tariffs last year would both reduce US capex and impair productivity growth. I forecast the opposite, that tariff walls would accelerate Localization-driven capex and shield US manufacturing from productivity-killing Chinese subsidies.

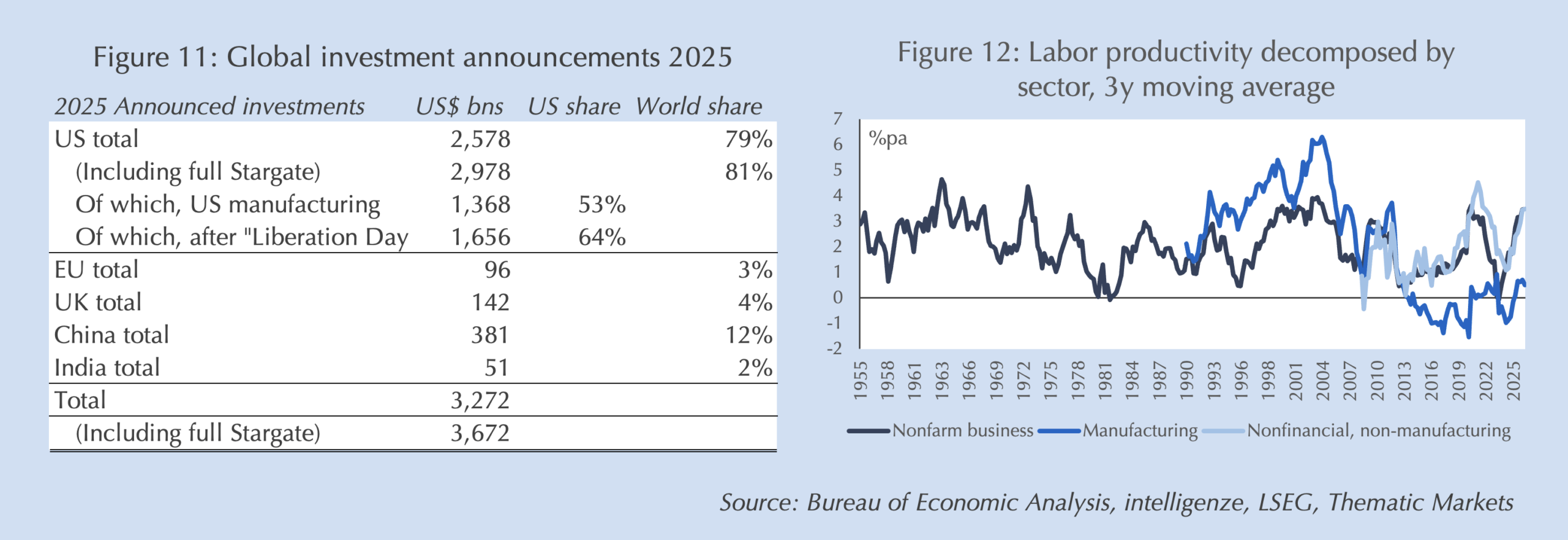

The investment numbers are undeniable: The US attracted nearly 80% of announced global capex last year, two thirds of which occurred after “Liberation Day” and more than half of which was manufacturing in contrast to the consensus narrative that this is all just AI data centers (Figure 11). Hard data on US capex and durable orders validate the announcements.

It’s too early for me to claim victory on productivity, but it is notable that US manufacturing productivity growth flipped from negative to positive on the first round of Chinese tariffs and accelerated last year (Figure 12).

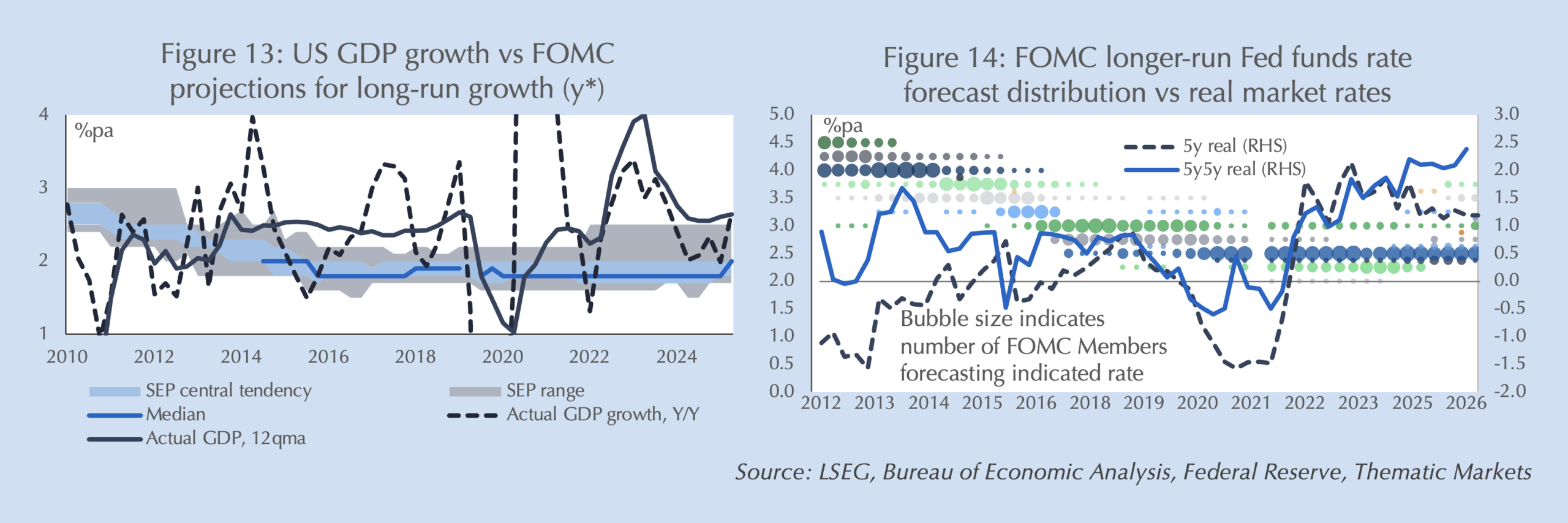

But enough about me. Let’s consider how the Fed looked at the same economy. It’s not pretty. Despite having 500 economists working for them — I don’t even have a research assistant — actual GDP growth has outpaced the most optimistic FOMC member’s estimate of trend growth for over a decade (Figure 13). That is despite realized real interest rates that have made a mockery of their estimates of neutral policy rates (Figure 14).

To paraphrase “The Princess Bride,” I don’t think “restrictive” means what they think it means.

This FOMC likes to blame their failures on Covid as though no other Committee faced cost shocks or uncertainty. Tell that to William Harding who had to face World War I, the Russian Revolution’s unprecedented disruptions of both grain and oil, the largest US steelworkers’ strike, and the Spanish Flu, all while handcuffed by the gold standard. Or even the much maligned Arthur Burns, who had to manage the float of the dollar, Nixon’s price controls, the Arab oil embargo, and the Great Grain Robbery, without the benefit of either inflation expectations data or well accepted understanding that the Phillips Curve shifts.

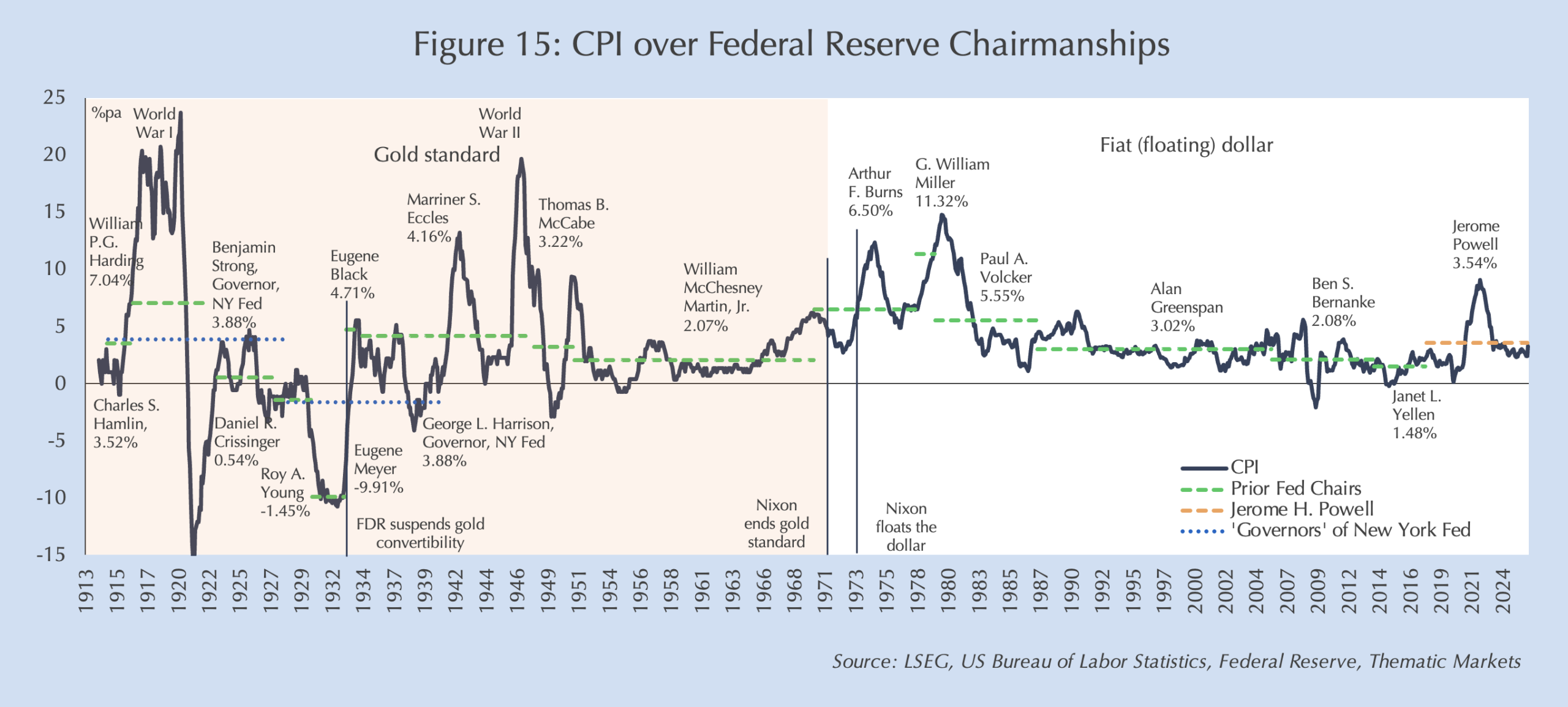

By the objective measure of average inflation, the Powell Fed is the seventh worst ever and the fourth worst of the fiat era (Figure 15). But that’s unfair to Paul Volcker who was handed 12% inflation as a welcoming gift. In contrast, Jerome Powell inherited sub-2% inflation and is bequeathing Kevin Warsh 4.4% core PCE inflation that is accelerating.

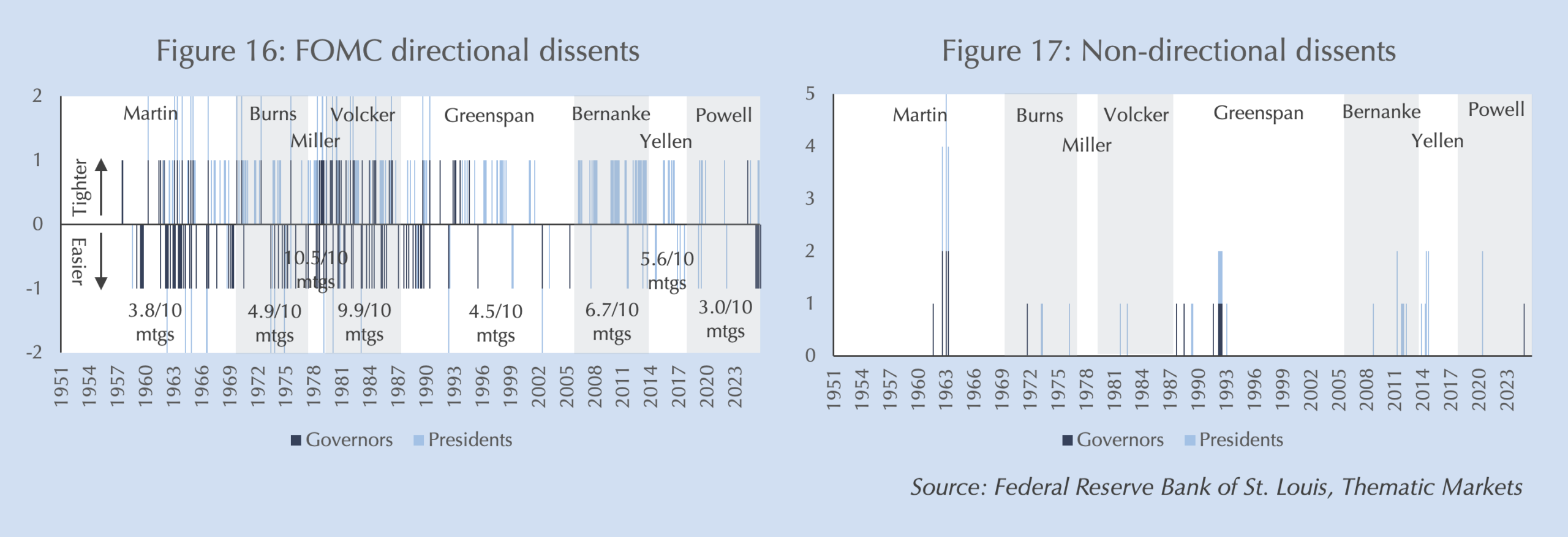

Importantly, this poor record was a team effort. I’m pleased to see that a few FOMC members have finally found their independence, but the record is clear: the Powell Fed had the lowest rate of dissents since the Fed-Treasury Accord secured that independence (Figures 16 and 17).

In closing, I’d like to relay one more lesson from ancient Greece. Athens’ greatest hero, Themistocles, saved Greece from the conquest by the world’s first true empire, the Persians. Despite that miraculous success, Themistocles was ostracised — that is publicly exiled by popular vote — for fraud and treason. Historians agree that the charges were questionable and factionalism played a role. But most also agree that Themistocles’ arrogance and lack of humility before his fellow citizens sealed his fate.

The current political assault on the Fed reflects similar factionalism. But it also results from objective policy failures that the Fed continues to deny. In a democracy, right or wrong, everyone must be accountable to the people. The Fed would do well to remember that if democracy can turn on a hero like Themistocles, it is far more likely to turn on an institution with an objective record of failure.

Comments are available to paid subscribers only.