The most important question in the US economy

Perhaps the most important debate on the US economy is whether or not it is undergoing a productivity boom. People on opposite sides of the debate often are perplexed at its existence: skeptics see artificial intelligence’s (AI’s) gains as a mirage, while optimist see undeniable improvement. Yet, I think both miss the bigger picture: the boom precedes large language models (LLMs) and is much broader. For nearly a decade, since well before ChatGPT’s introduction, I’ve been pointing to signs of accelerating productivity. My consistently above-consensus forecasts for economic growth, real interest rates, the dollar, and corporate earnings were due to the rapid advancements in automation, both cognitive and mechanical, embodied in my Localization thesis. Global bifurcation reinforces the resultant capex and productivity boom as it both further incentivizes automated Localization and blocks the most destructive effects of Chinese industrial policy.

Why productivity matters

The pace of productivity growth — the growth of output per worker — determines living standards, asset prices, interest rates, and exchange rates. Faster productivity growth allows firms to both pay workers higher real (inflation-adjusted) wages and generate more profits for shareholders, raising both consumption and share prices. Businesses borrow to expand and consumers borrow to build bigger houses, putting upward pressure on real interest rates. Higher wages and profits mean more tax revenue, easing fiscal constraints and lowering term premia on government bonds. Everyone else in the world wants to invest in the boom, pushing up the dollar. However, contrary to the views of some, including those expressed by new Fed Chairman Kevin Warsh, higher productivity does not necessarily lower inflation or allow for lower policy rates. In fact, it likely does the opposite.

Uncertainty strikes again

Productivity booms offer another great example of Uncertainty, which I discussed in my last article: they are completely unpredictable. But once they start, they tend to bunch together, leading to an extended period of innovation. An old friend, Alejandro Gaviria, documented this phenomenon in the behavior of world records in cycling and track and field.1[1] Alej found that once a world record falls, it tends to be broken several more times in quick succession before an unpredictably long period of stagnation emerges. He found that the “clustering” of new records typically began with a technological innovation — like the clipless pedal in cycling — that spurred both new training and a sequence of minor related innovations until imagination was exhausted. A new cluster would only emerge when a wholly new innovation emerged. Other economists have verified Alej’s insights for economic productivity.2[2] Both the clustering of innovations and the unpredictability of their occurrence cause problems for economists. Many are skeptical when a new productivity surge arrives, then wrongly assume the sequence of new innovations will continue forever.

Why is there even a debate?

As an economist-entrepreneur there is no debate in my mind on AI’s actual and potential productivity gains. Three years ago I might spend a week programming an analysis; now I “write” complex code with the help of an LLM in an hour. Basic research that took weeks before now can be done in days. The gain in my output per hour worked is not just measurable, it is nothing short of miraculous. But there are prominent, well respected economists like Northwestern University’s Robert Gordon who doubt that these gains are sufficient to overcome aging workforces, worsening educational outcomes, and inequality;3[3] and Nobel laureate Daron Acemoglu, who questions whether AI’s reach is broad enough, and whether it merely replaces rather than augments workers.4[4]

I’ll believe it when I see it

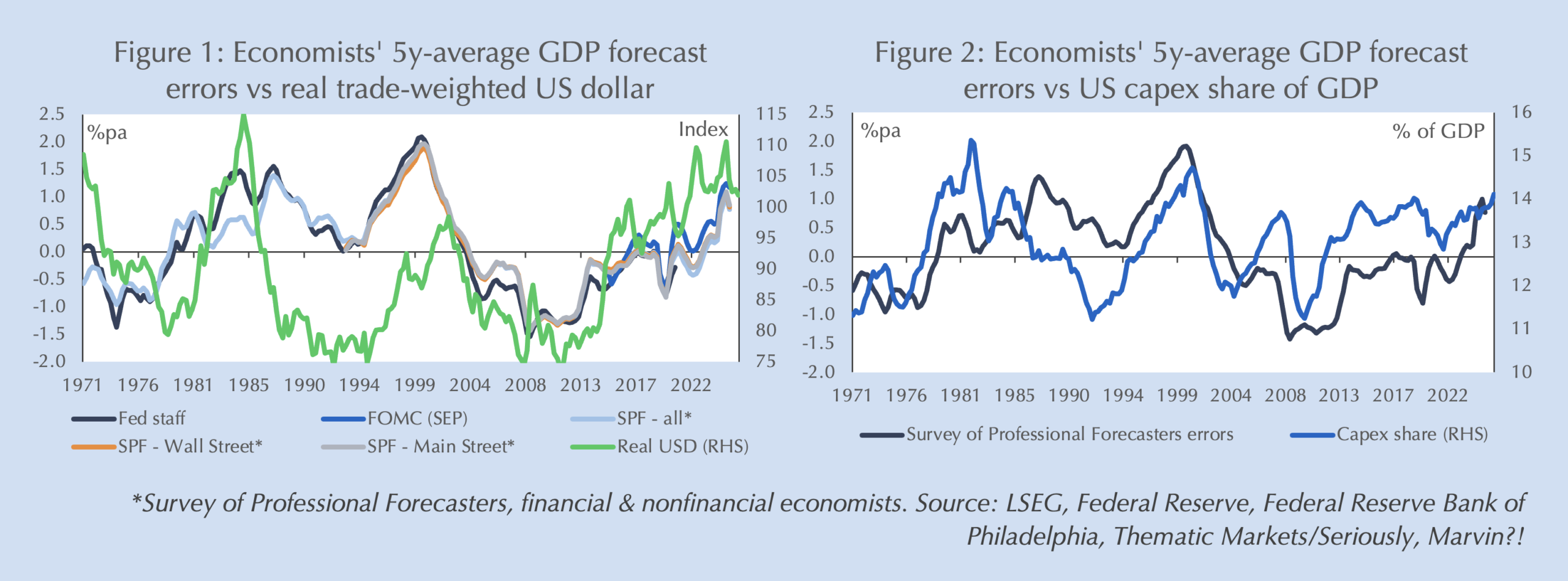

But the more common view of economists is that expressed by St. Louis Fed President Alberto Musalem: I’ll believe it when I see it in the data.5[5] The long, uncertain lags between productivity booms that Alej documented induce persistent skepticism that history suggests is only overcome once the boom is nearly passed. Figure 1 updates a chart that I created a few years ago that shows the surprisingly strong correspondence between economists’ forecast errors for GDP growth and the trade-weighted real exchange value of the dollar.

Innovation cycles in economists’ rearview mirror

Long-time readers of my research will immediately understand the source of the seemingly spurious relationship. As I showed in Solved: Drivers of the dollar cycle, the big, decade-plus swings in the dollar are driven by periodic innovation waves that power productivity booms. Economists, waiting for unequivocal evidence of accelerating productivity, underpredict growth as it happens, then overestimate it in subsequent years when they finally update their models to reflect higher productivity growth after it has passed. As Figure 1 illustrates, economists’ rearview-mirror forecasting is remarkably consistent through time and across institutions, from the Fed to Wall Street to corporate America: do you see five forecast lines, or just one? You’d almost think they were copying each other’s homework.

Innovation >>> capex >>> productivity data

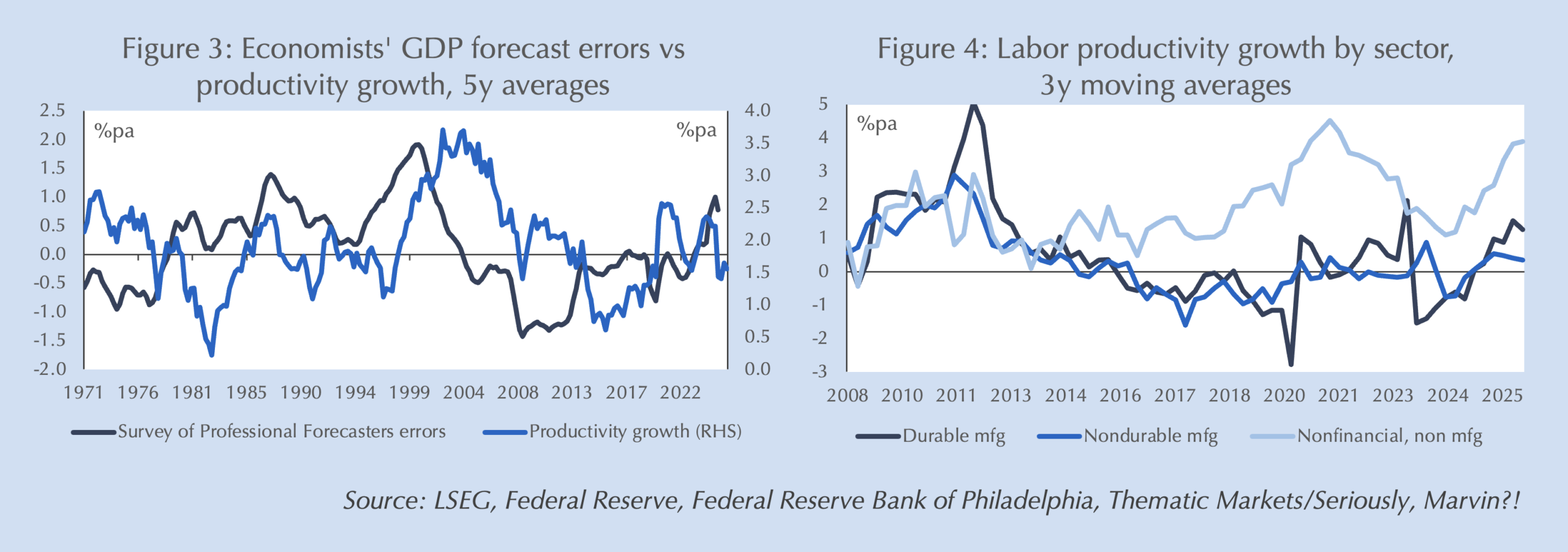

Figures 2 and 3 illustrate how the productivity data lag. Each re-plots the Survey of Professional Forecasters’ errors — no need to show other economists’ since they all make the same errors! — but versus different components of the innovation cycles that economists consistently miss: capex (nonresidential fixed investment) in Figure 2 and productivity growth in Figure 3. Capex, like the dollar is contemporaneous with economists’ forecast errors; i.e. markets’ and companies’ investment decisions reflect awareness of the productivity it will produce. But measured productivity in the data lags by years as shown in Figure 3. Stanford’s John Brynjolfsson explains why: firms make investment decisions based on perceived productivity enhancements, but the gains only show up once new factories are finished.6[6] It also takes time to work out the kinks in the system, to learn how to use the new technology most efficiently. And, as shown in Alej’s paper, it generally inspires new ideas that extend the technology boom. At some point, the gains taper off, but one look at Figure 1 shows this time is different: the dollar cycle is much more persistent than prior cycles. As I noted in Solved, this innovation cycle appears to have both much shorter, compounding product cycles and be more durable.

Markets’ blind forecasting

Markets, through their ability to aggregate information across individual company investment decisions, often foretell productivity booms well before economists. The dollar, as shown in Figure 1, is one expression of that (when the boom originates in the US). Equity markets are another. Falling equity risk premia (rising P/E ratios) may reflect a bubble, or they may attest to individual investors blindly “forecasting” a productivity boom that raises earnings. The difference is determined by earnings performance, which (so far) has well validated that it reflects productivity rather than a speculative bubble. Often lost in“Dot.com bubble” narratives is that it only became bubblicious in 1999-2000; during the infamous “irrational exuberance” phase of 1996-’99,7[7] sustained positive earnings surprises, like the strong dollar, accurately foretold the late-1990s/early-2000s productivity boom.

Markets narratives and the bigger picture

Yet markets also are misled by their own narratives. The productivity gains of the Dot.com era were broad based as networking technologies improved logistics, inventory management and production control across industries (Figure 3). Yet, equity markets at the time invested disproportionately — and most painfully when the 1999-2000 bubble burst — in any company adding “.com” to its name. Similarly, markets today focus on the Magnificent 7, hyperscalers and AI-specialized firms, missing the broader productivity boom that started more than a decade ago and extends across sectors (Figure 4).

Why I remain bullish on US productivity growth

I have no idea whether leading AI names have already become bubblicious, will ever meet their hyperbolic long-term earnings expectations, or even survive. But I have no doubt that we are still in the “early innings” of a broader productivity boom that market narratives, again, appear to underestimate. There are three reasons for this:

- Contrary to conventional wisdom, Global bifurcation and US tariff policy are accelerating US capex and productivity (as I correctly forecast following “Liberation Day”). In prior research I had shown that China’s manufacturing gains since 2010 were due to subsidized capital deepening, not efficiency gains. The associated overcapacity undermined productivity growth elsewhere by wiping out competition and associated “learning-by-doing” productivity. That made it obvious that shielding the immense, hyper-competitive US marketplace from Chinese industrial policy would raise US investment and productivity growth.

- Recall from Alej’s research that innovation waves cluster as each innovation spurs others. While automated Localization predates generative AI, its rapid development is likely to both broaden and accelerate the process of discovery that extends the clustering process. That is particularly true as US entrepreneurs attempt to re-enter markets they have long since been driven out of.

- As noted above, economic data, markets and anecdotes suggest this innovation wave is much stronger than prior ones. The US capex boom is already the largest on record, cumulatively measured, and continues to drive growth; US earnings surprises have continued far later into this recovery than in prior cycles while the US equity risk premium is only in the 30th percentile of the last 155 years, suggesting pricing is not yet as stretched as many believe; and the dollar remains near multi-decade highs.

Inflation and Fed policy

That said, my view of the consequences of a sustained productivity boom is very different from that described by incoming Fed Chairman Kevin Warsh. Chairman Warsh points to the 1990s as an era of productivity-driven low inflation and suggests that policy rates can be lower as a result. However, that reading ignores the economic implications of a rise in productivity growth, the unique circumstances of the 1990s, and the importance of Being is believing on the path of inflation. Higher productivity growth raises the marginal product of capital, increasing demand for investment and pushing the neutral interest rate higher, not lower. US real interest rates averaged nearly 4% in the 1990s, almost double the current 10-year TIPS yield. Both cost pressures and long-term interest rates fell in the 1990s due to the opening of vast new sources of labor in China and the former East Bloc, rampant mercantilism across Asia that created both a “global savings glut” and massive expansion of manufacturing capacity, and falling geopolitical competition that cheapened trade. All those factors are operating in reverse under Global bifurcation.

Unstable inflation expectations

But the biggest difference between now and the 1990s is in inflation expectations, aka Being is believing. By the late 1990s the Fed benefitted from low and stable inflation expectations as Paul Volcker crushed the 1970s’ inflation and Alan Greenspan reinforced it with his aggressive response to accelerating growth in 1994. Chairman Warsh, unfortunately inherits the fruits of nearly two decades of irresponsible monetary policy — that he vociferously criticized — that have left him with unanchored inflation expectations and core inflation that is nearly double the Fed’s target and accelerating. With current real policy rates well below neutral, capex demand reaccelerating and rising gasoline prices, inflation is likely to accelerate further without a considerable rise in the Fed funds rate. We will soon see if Chairman Warsh’s claims to “epistemic humility” were mere rhetoric, or if his long-time criticism of insular Fed thinking was genuine.

Comments are available to paid subscribers only.